This topic contains a solution. Click here to go to the answer

|

|

|

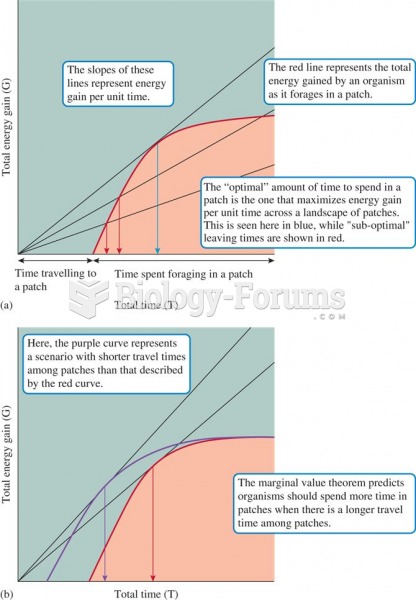

A graphical representation of the marginal value theorem.

A graphical representation of the marginal value theorem.

How to evaluate a function containing the constant k

How to evaluate a function containing the constant k

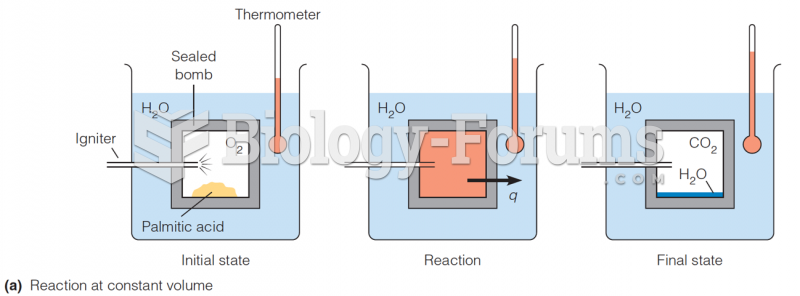

Reaction at constant-volume

Reaction at constant-volume

Answer the following short answer, please show your steps and include the formulas used

Answer the following short answer, please show your steps and include the formulas used

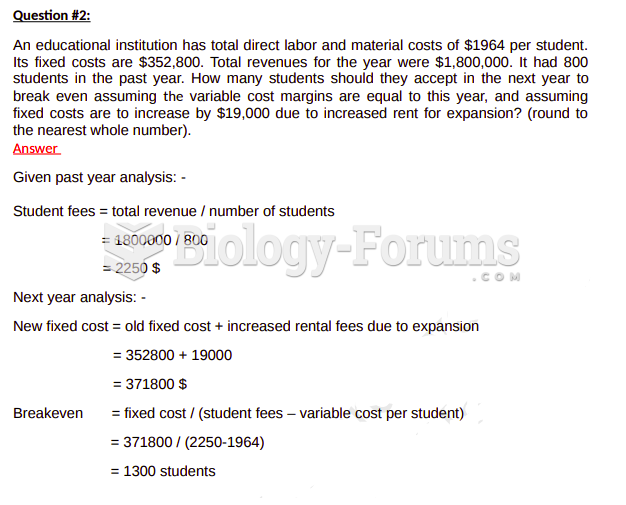

An educational institution has total direct labor and material costs of $1964 per student. Its ...

An educational institution has total direct labor and material costs of $1964 per student. Its ...

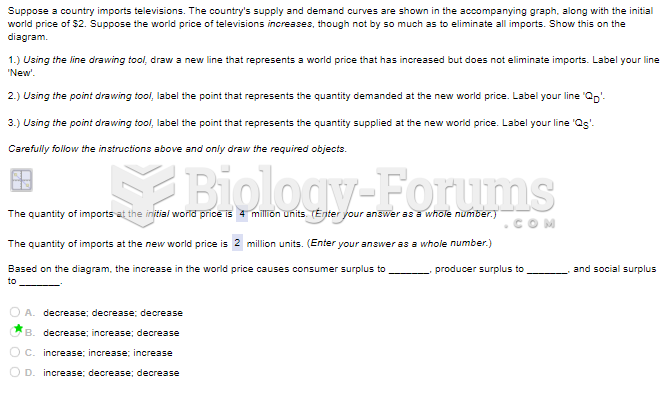

Suppose a country imports televisions. The country's supply and demand curves are shown in ...

Suppose a country imports televisions. The country's supply and demand curves are shown in ...