Zack Peyton borrowed 398,000 from Fifth First Bank to purchase a new home. Zack gave First Bank a mortgage on his home. The mortgage was recorded on January 3, 2014. Zack had made a down payment of 42,000. When Zack moved in, he purchased an in-ground swimming pool from Paddock Pools for 35,000. Zack paid Paddock 4,000 and Paddock financed the remaining amount for him, recording a mortgage for 29,000 on February 26, 2014. Zack needed window coverings, landscape, and some new furniture. Wells Fargo gave Zack a 150,000 home equity line of credit, secured by a mortgage on Zack's home for 150,000. Wells Fargo recorded the home equity credit line mortgage on February 1, 2014. Zack, because of a bonus at work, did not draw on the line of credit until June 10, 2015, using 25,000. The economy went south somewhere around September 2015. The value of Zack's home dropped by almost 50. Zack lost his job. He could no longer make his payments. Fifth First Bank served Zack with a notice of foreclosure on November 1, 2015. Suppose that the fact pattern is changed slightly and prior to the economy going south, Zack sold his home to Melanie Knight for 450,000. Melanie paid Zack 52,000 and assumed the Fifth First Bank mortgage. The property was transferred subject to the Paddock mortgage but Melanie did not agree to assume the payments on the pool. Zack failed to make the payments on the Paddock Pool. Paddock has begun foreclosure proceedings on the home.

A)Paddock has no foreclosure rights because it is second in line in priority.

B)Paddock has no foreclosure rights because it is third in line in priority.

C)Paddock has no foreclosure rights because Melanie did not agree to assume the loan.

D)Paddock has the right to foreclose on its mortgage.

Question 2

With reference to 29, what type of interest does X hold?

A) Fee simple determinable

B) Fee simple subject to a condition subsequent

C) Fee tail

D) None of the above

Charles Darwin may be dead and gone but a recent write-in campaign has pitted him against Republican

Charles Darwin may be dead and gone but a recent write-in campaign has pitted him against Republican

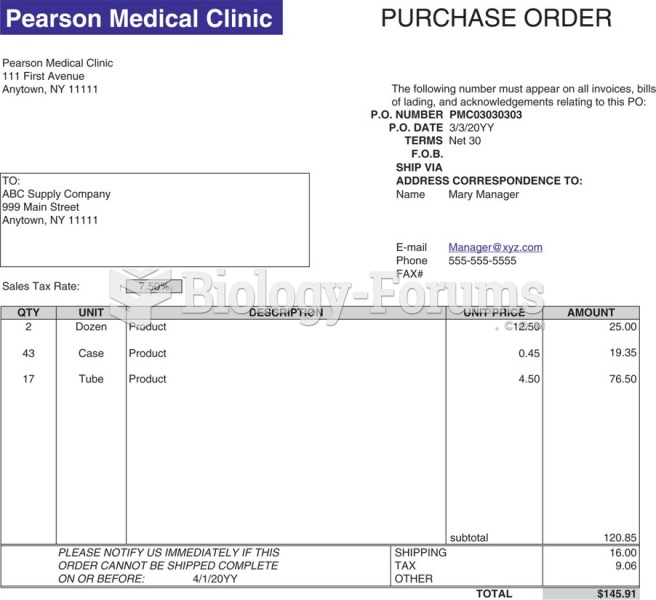

Sample purchase order form.

Sample purchase order form.

On the left is one of Jennifer Lopez’s homes, this one in Miami Beach. She also has a home in ...

On the left is one of Jennifer Lopez’s homes, this one in Miami Beach. She also has a home in ...

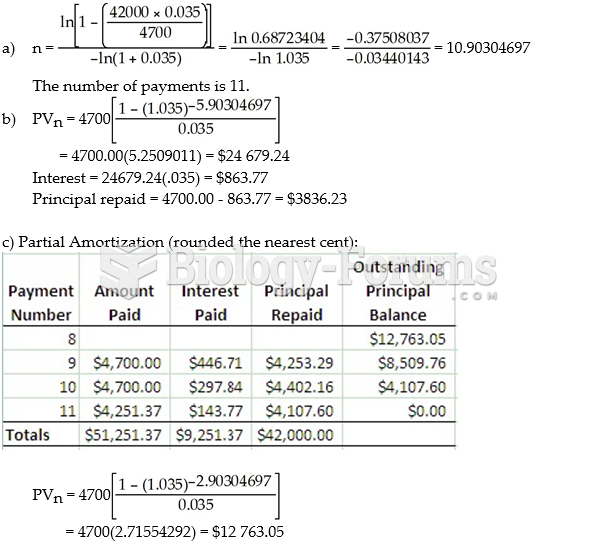

Rola Inc. borrowed $42 000.00 at 7% compounded semi-annually. The loan is repaid by payments of ...

Rola Inc. borrowed $42 000.00 at 7% compounded semi-annually. The loan is repaid by payments of ...

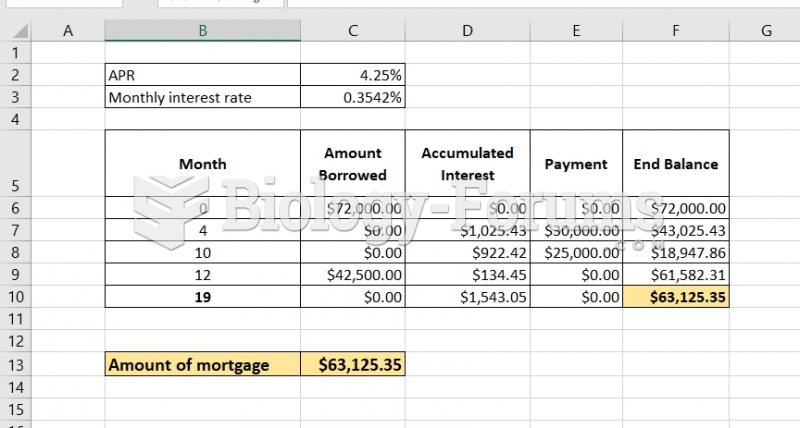

Raman has a line of credit loan with the ICICI bank. The initial loan balance was $72000.00. ...

Raman has a line of credit loan with the ICICI bank. The initial loan balance was $72000.00. ...

Piggy bank

Piggy bank