Answer to Question 1

The price elasticity of demand measures the percentage change in quantity demanded of a good due to a percentage change in its price. The market price elasticity cannot be less than 0.2 . If price falls by one percent, Green will buy 0.2 percent more sweaters and the increase in everybody else's consumption will be greater than 0.2 percent (since their price elasticities are all greater than 0.2). Since total demand will rise by more than 0.2 percent, the market price elasticity must be greater than 0.2 . A similar argument would show that the market price elasticity must be less than 1.2 .

Answer to Question 2

The momentary supply, short-run supply, and long-run supply all illustrate the response of suppliers to changes in the price, but they differ according to how much time has elapsed after the price change.

The momentary supply is frequently the least elastic and shows how suppliers cannot easily respond to a price change immediately after the price change occurs. Changing the quantity produced means changing the inputs into the production process, which takes time to complete. Sometimes the momentary supply is perfectly inelastic.

The short-run supply shows suppliers' response after enough time has elapsed for some, but not all, of the possible technological adjustments have occurred. Short-run supply generally is intermediate in elasticity between the momentary supply and the long-run supply.

The long-run supply shows how suppliers react after enough time has passed that all possible adjustments to factors of production have been made to accommodate the price change. It usually is the most elastic of the three supplies.

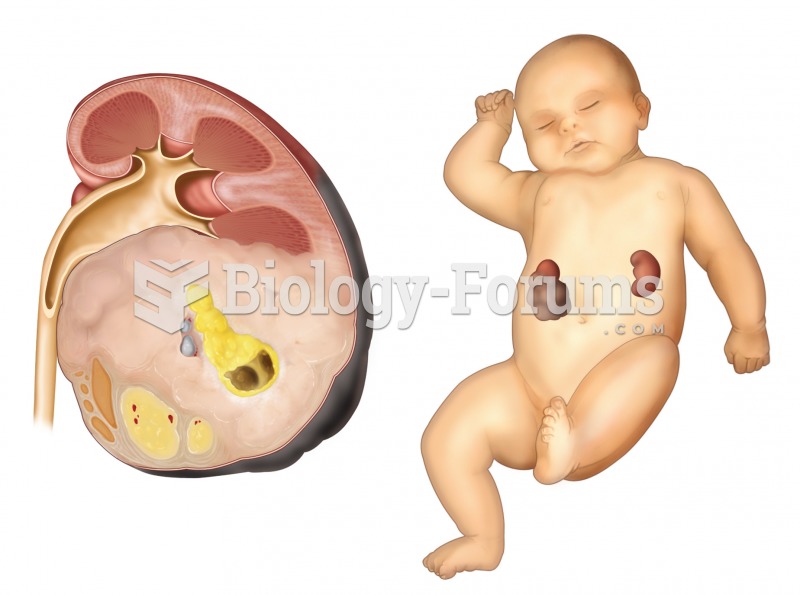

Nephroblastoma. A sectioned kidney reveals the presence of a very large tumor, which arose from feta

Nephroblastoma. A sectioned kidney reveals the presence of a very large tumor, which arose from feta

Food Sources When it comes to meeting your vitamin K needs, think green

Food Sources When it comes to meeting your vitamin K needs, think green

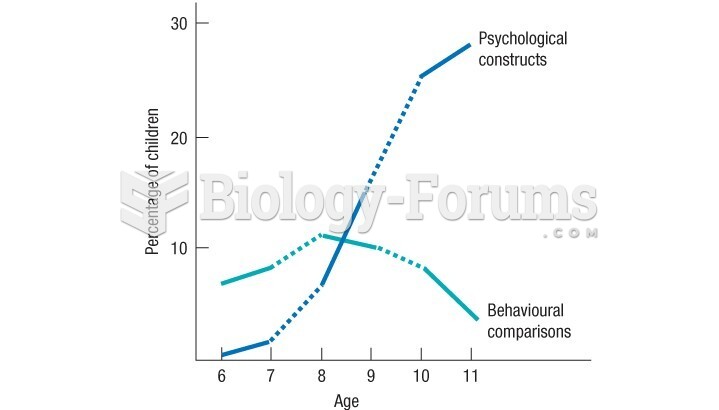

Barenboim's study show the change in children's descriptions of their peers

Barenboim's study show the change in children's descriptions of their peers

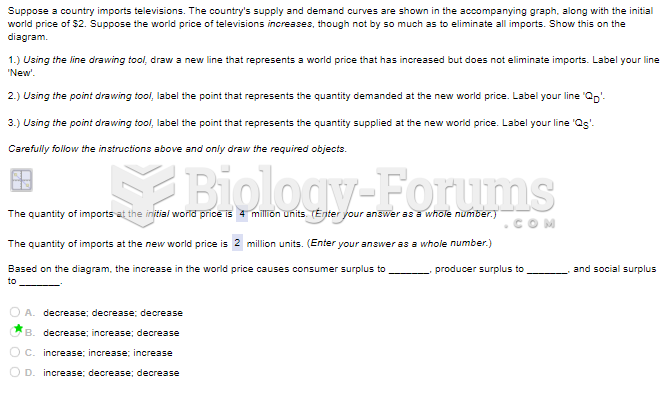

Suppose a country imports televisions. The country's supply and demand curves are shown in ...

Suppose a country imports televisions. The country's supply and demand curves are shown in ...

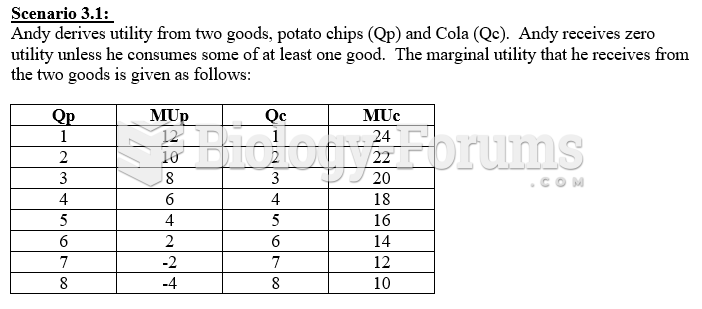

Refer to Scenario 3.1. If the price of potato chips is $0.50 and the price of Cola is $4.00, ...

Refer to Scenario 3.1. If the price of potato chips is $0.50 and the price of Cola is $4.00, ...

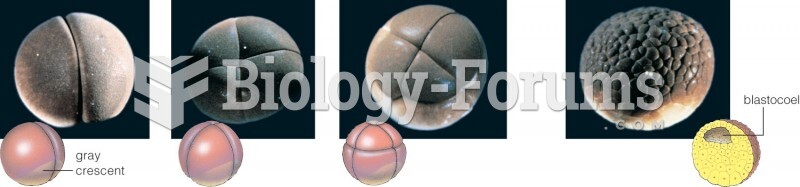

Here we show the first three divisions of cleavage, a process that carves up a zygote’s cytoplasm. ...

Here we show the first three divisions of cleavage, a process that carves up a zygote’s cytoplasm. ...