Answer to Question 1

D

Answer to Question 2

When firms have non-identical cost structures, the pattern of entry into the industry is different than when they have identical cost structures. In the former case, it is the set of firms with the lowest average total cost curve that enters the market first and earns highest economic profits. The next set of firms that enters has a higher average total cost than the initial lot of market entrants. Eventually, a firm with an even higher average total cost curve enters the market and this firm earns zero economic profits. This firm is called the marginal entrant, as it is indifferent between entering the market and staying out of the market. The price in the market is equal to the marginal entrant's long-run average total cost because for any price below this price there is absolutely no incentive for the firm to enter. Because the price equals the long-run average total cost curve of the marginal entrant and not the minimum average total cost curve of the industry, the market supply curve is upward-sloping rather than horizontal. On the other hand, in case of a market where all firms have an identical cost structure, the long-run price equals the minimum average total cost of the industry, which is the same for all firms. Hence, the market supply curve in this case is horizontal and there are no economic profits in the long run. Because in the case of non-identical cost structures, firms face an upward-sloping market supply curve even in the long run, low-cost firms can make positive economic profits.

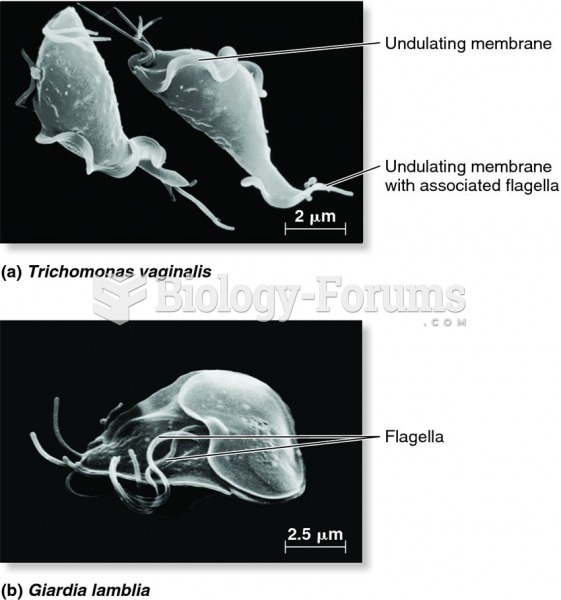

Parasitic members of the supergroup Excavata.

Parasitic members of the supergroup Excavata.

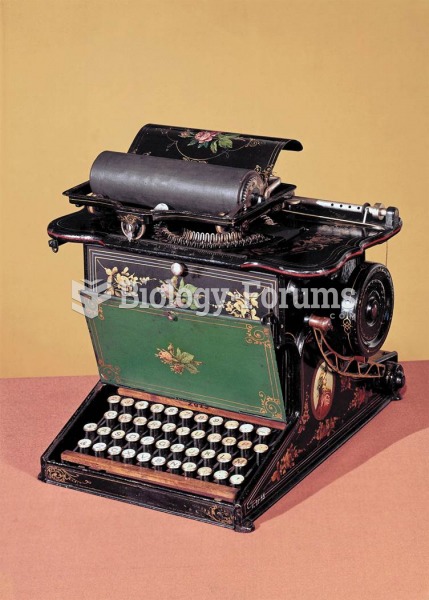

The first commercially successful typewriter, manufactured in quantity beginning in 1874, surely fue

The first commercially successful typewriter, manufactured in quantity beginning in 1874, surely fue

PPE used to prevent exposure to bloodborne pathogens.

PPE used to prevent exposure to bloodborne pathogens.

Cost Accounting 14

Cost Accounting 14

Therapy to Prevent PTSD after Disaster

Therapy to Prevent PTSD after Disaster

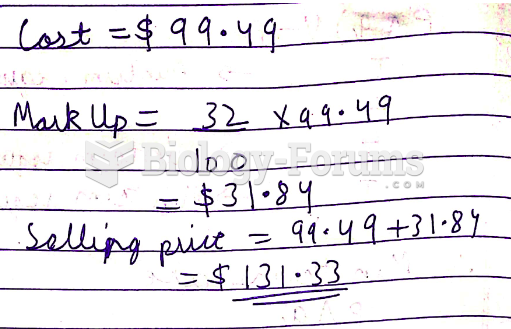

Cost = $99.49; Rate of markup based on cost = 32%. Find the markup and selling price.

Cost = $99.49; Rate of markup based on cost = 32%. Find the markup and selling price.