What a firm must pay for its inputs is referred to as its:

A) production value.

B) cost of production.

C) opportunity cost.

D) loss in production.

Question 2

The profit earned by a monopolistic competitor after the entry of new firms is ________.

A) higher than the profit earned by the firm before the entry of new firms

B) lower than the profit earned by the firm before the entry of new firms

C) equal to the profit earned by a monopolist in the long run

D) higher than the profit earned by a perfect competitor in the long run

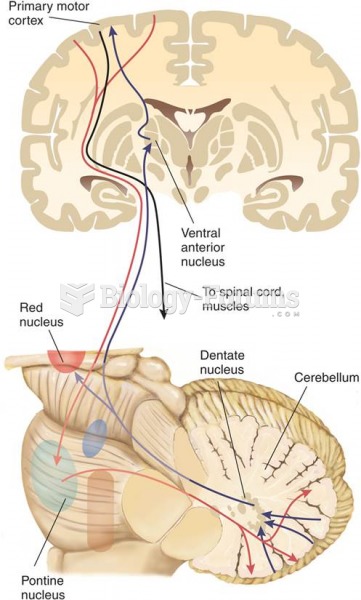

Inputs and Outputs of the Lateral Zone of the Cerebellar Cortex

Inputs and Outputs of the Lateral Zone of the Cerebellar Cortex

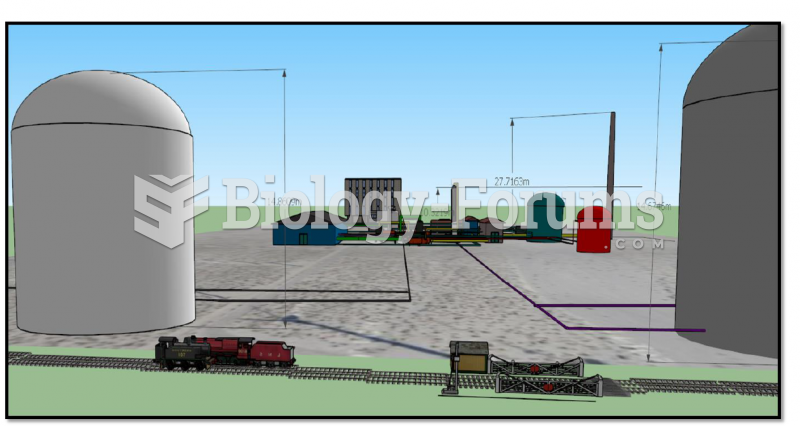

3D Plant Layout - Side View for Dual-Stage Pressure Production of Nitric Acid

3D Plant Layout - Side View for Dual-Stage Pressure Production of Nitric Acid

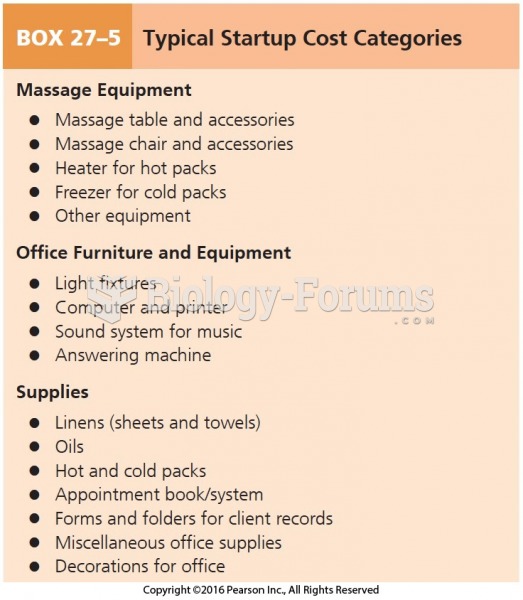

Typical Startup Cost Categories Cont.

Typical Startup Cost Categories Cont.

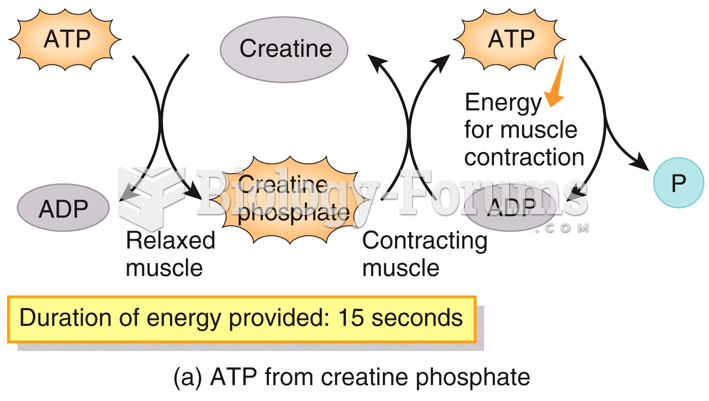

ATP Production in Cardiac Muscle

ATP Production in Cardiac Muscle

Production of prototrophs as a result of genetic recombination

Production of prototrophs as a result of genetic recombination

A cowbird with its foster parent. A female cowbird minimizes her cost of parental care by laying her

A cowbird with its foster parent. A female cowbird minimizes her cost of parental care by laying her