This topic contains a solution. Click here to go to the answer

|

|

|

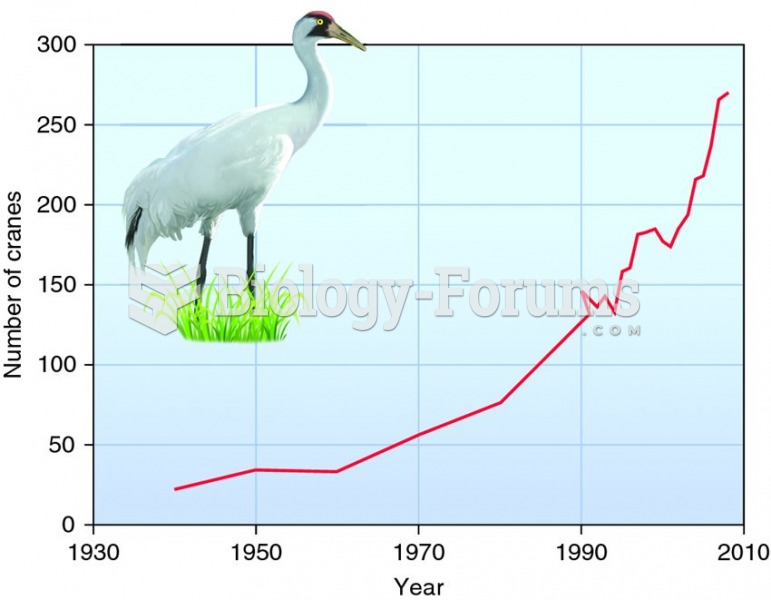

Exponential growth in the Canadian migratory population of the whooping crane after 70 years of cons

Exponential growth in the Canadian migratory population of the whooping crane after 70 years of cons

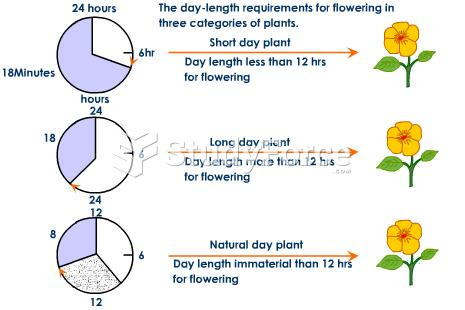

Growth of Plants

Growth of Plants

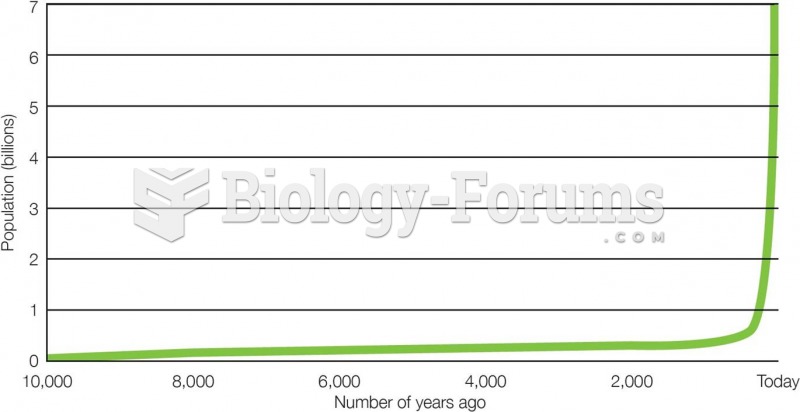

World Population Growth, Past 10,000 years

World Population Growth, Past 10,000 years

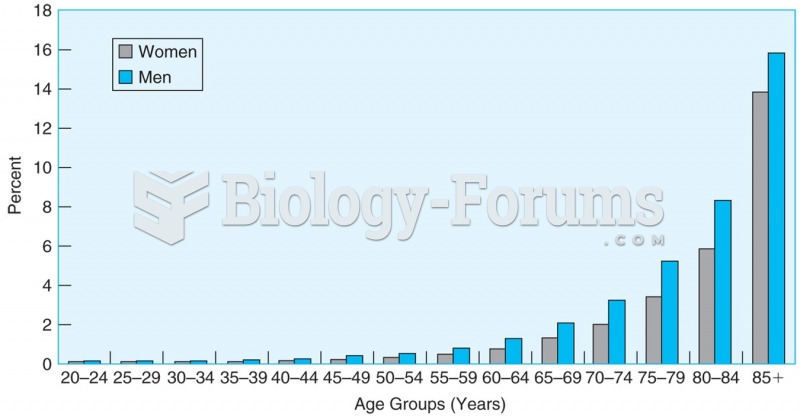

The mortality rate in the United States increases with age and is lower for women than men at every ...

The mortality rate in the United States increases with age and is lower for women than men at every ...

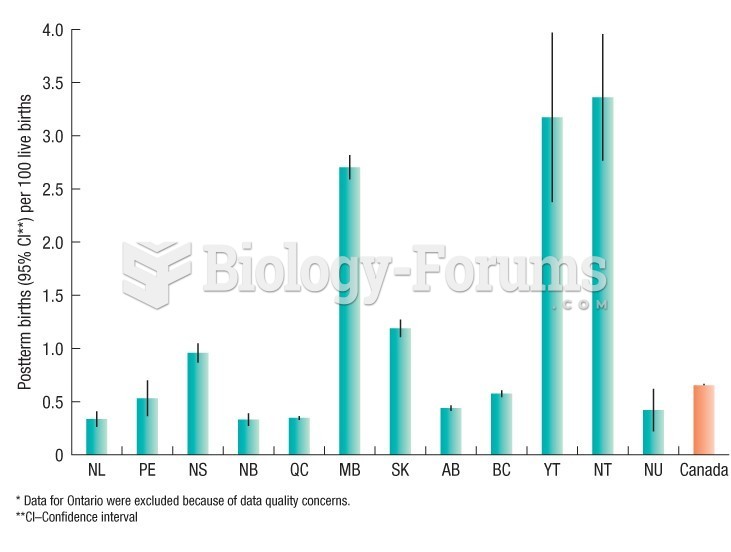

Post-term birth rates, by province/territory, Canada

Post-term birth rates, by province/territory, Canada

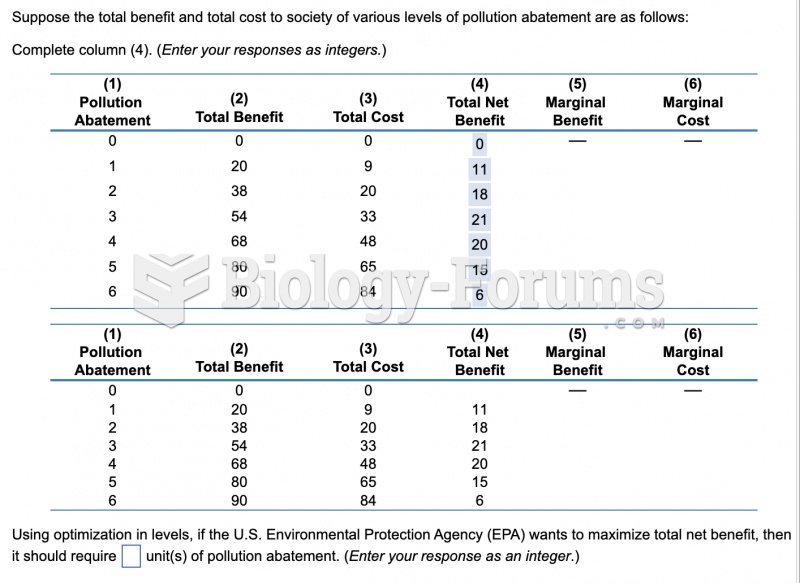

economic question

economic question