Firms in a perfectly competitive market usually enter or leave an industry in the short-run and not in the long-run.

Indicate whether the statement is true or false

Question 2

When revenue is less than total cost but more than variable cost it implies that:

a. the firm is enjoying positive economic profits.

b. the firm is earning normal profits.

c. the firm can cover its variable cost and a part of its fixed costs.

d. the firm is unable to cover its costs and should shut down.

e. the firm is able to cover both its fixed and variable costs.

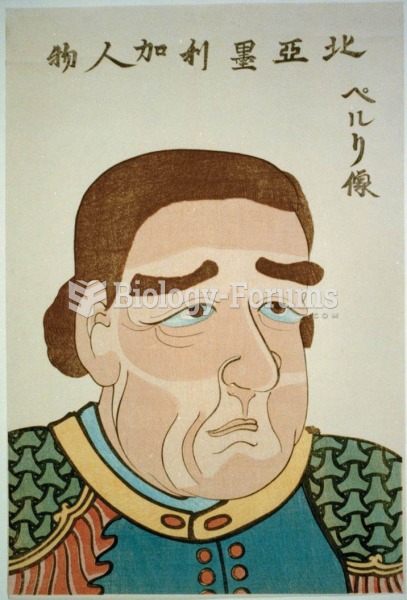

A photograph of Commodore Matthew Perry in 1855 juxtaposed with a Japanese portrait of him. When Per

A photograph of Commodore Matthew Perry in 1855 juxtaposed with a Japanese portrait of him. When Per

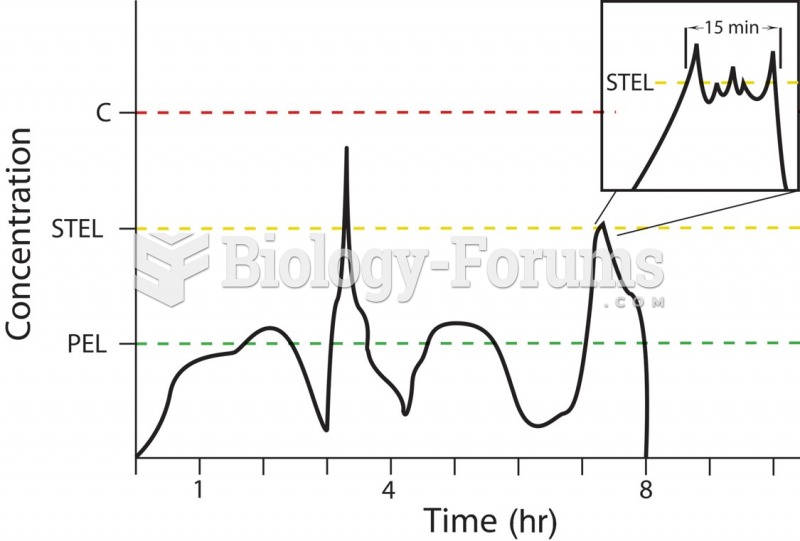

The relationship between the permissible exposure limit (PEL), the short-term exposure limit (STEL), ...

The relationship between the permissible exposure limit (PEL), the short-term exposure limit (STEL), ...

Reconstruction Drawing of Trajan's Market

Reconstruction Drawing of Trajan's Market

Project Management: Achieving Competitive Advantage

Project Management: Achieving Competitive Advantage

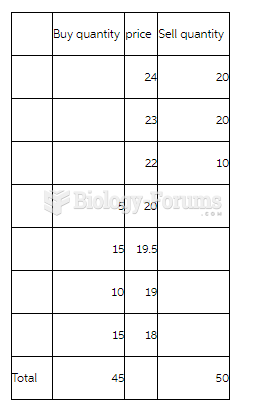

Markets and Institutions Market Story Problem

Markets and Institutions Market Story Problem

Short form of amino acids

Short form of amino acids