|

|

|

Blue whale skeleton, outside the Long Marine Laboratory at the University of California, Santa Cruz

Blue whale skeleton, outside the Long Marine Laboratory at the University of California, Santa Cruz

Rebound Tenderness, Apply Firm Pressure to the Abdomen

Rebound Tenderness, Apply Firm Pressure to the Abdomen

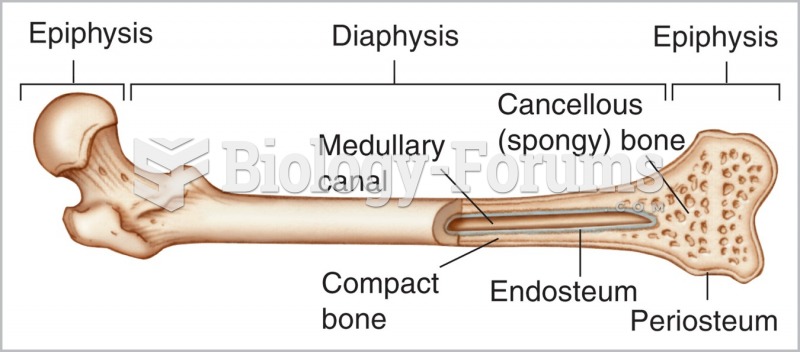

The features found in a long bone.

The features found in a long bone.

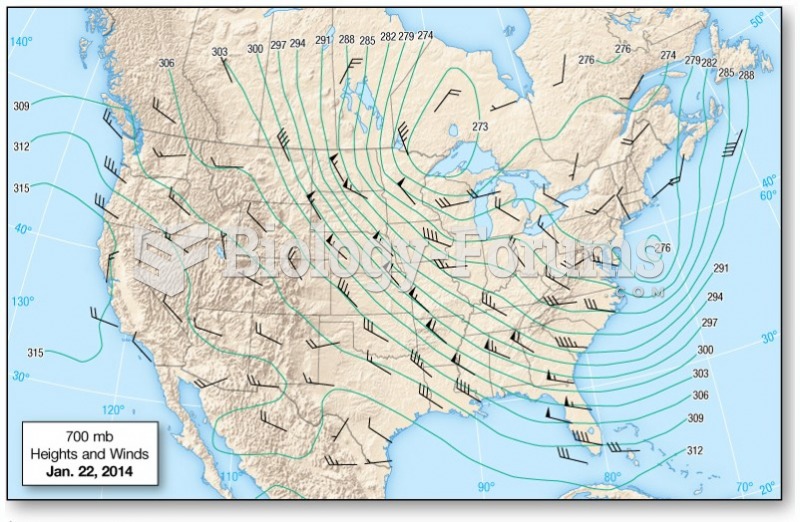

Upper-Level Maps

Upper-Level Maps

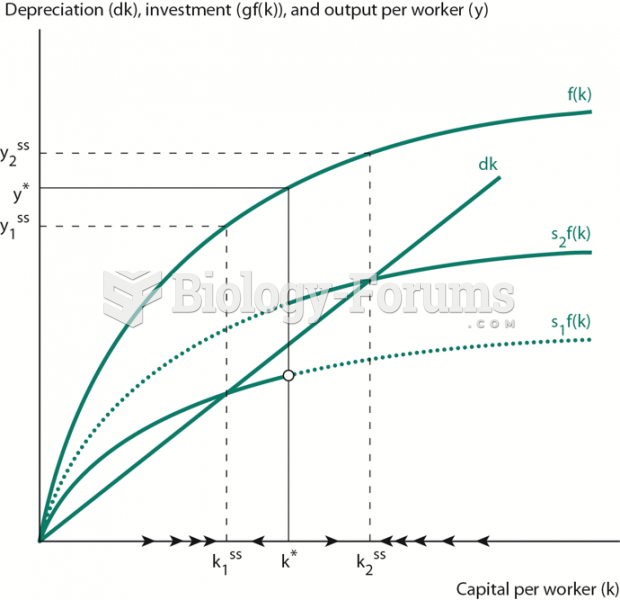

Solow Model with Saving Dependent on Income Level

Solow Model with Saving Dependent on Income Level

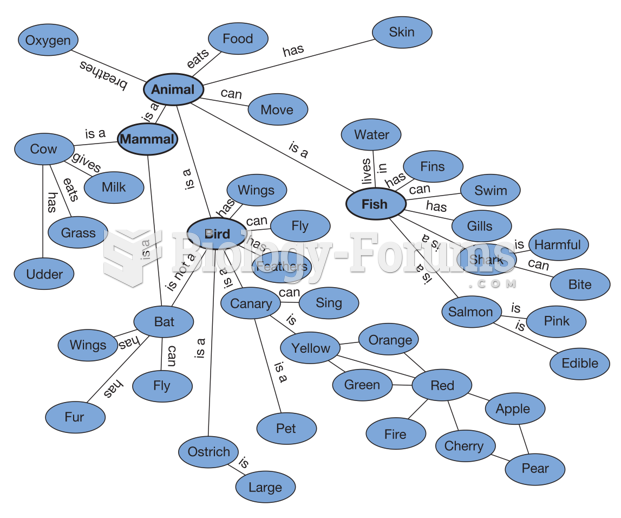

Part of a Semantic Network in Long-Term Memory

Part of a Semantic Network in Long-Term Memory