Answer to Question 1

C

Answer to Question 2

1. Budgeted fixed manufacturing overhead costs rates:

Denominator

Level Capacity

Concept Budgeted Fixed

Manufacturing

Overhead per

Period

Budgeted

Capacity

Level Budgeted Fixed

Manufacturing

Overhead Cost

Rate

Theoretical 6,480,000 5,400 1,200.00

Practical 6,480,000 3,840 1,687.50

Normal 6,480,000 3,240 2,000.00

Master-budget 6,480,000 3,600 1,800.00

The rates are different because of varying denominator-level concepts. Theoretical and practical capacity levels are driven by supply-side concepts, i.e., how much can I produce? Normal and master-budget capacity levels are driven by demand-side concepts, i.e., how much can I sell? (or how much should I produce?)

2. The variances that arise from use of the theoretical or practical level concepts will signal that there is a divergence between the supply of capacity and the demand for capacity. This is useful input to managers. As a general rule, however, it is important not to place undue reliance on the production volume variance as a measure of the economic costs of unused capacity.

3. Under a cost-based pricing system, the choice of a master-budget level denominator will lead to high prices when demand is low (more fixed costs allocated to the individual product level), further eroding demand; conversely, it will lead to low prices when demand is high, forgoing profits. This has been referred to as the downward demand spiralthe continuing reduction in demand that occurs when the prices of competitors are not met and demand drops, resulting in even higher unit costs and even more reluctance to meet the prices of competitors. The positive aspects of the master-budget denominator level are that it is based on demand for the product and indicates the price at which all costs per unit would be recovered to enable the company to make a profit. Master-budget denominator level is also a good benchmark against which to evaluate performance.

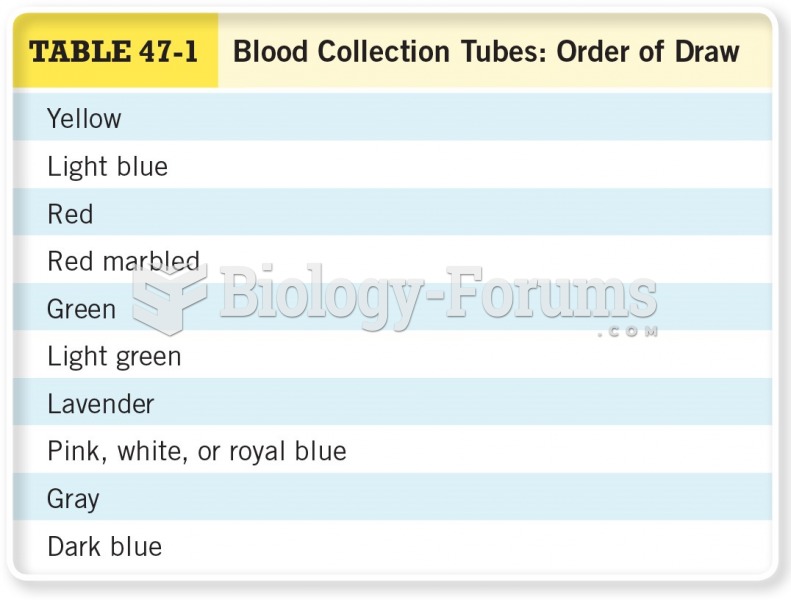

Blood Collection Tubes: Order of Draw

Blood Collection Tubes: Order of Draw

How to convert verbal statements into algebraic equations (Part 3)

How to convert verbal statements into algebraic equations (Part 3)

How to convert verbal statements into algebraic equations (Part 2)

How to convert verbal statements into algebraic equations (Part 2)

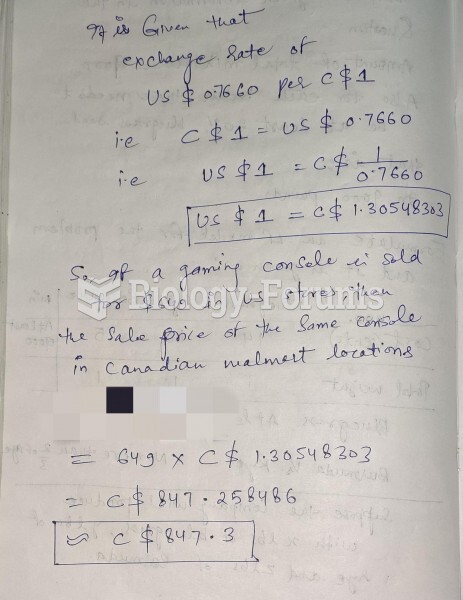

In order to encourage Canadians to avoid cross border shopping, Walmart Canada is striving to ...

In order to encourage Canadians to avoid cross border shopping, Walmart Canada is striving to ...

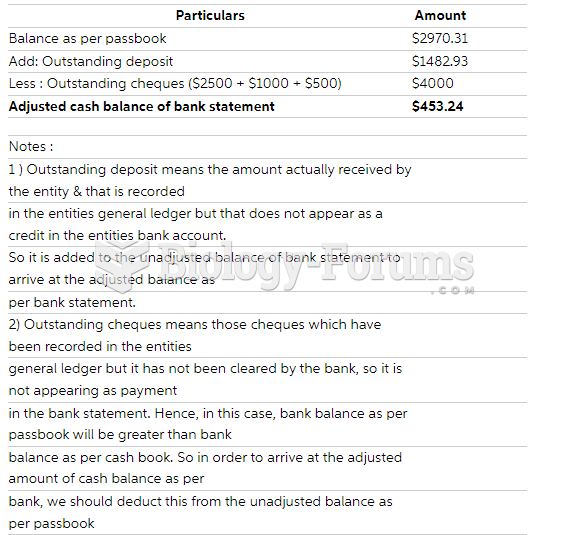

A bank statement shows a balance of $2,970.31 The check register of the account owner shows an ...

A bank statement shows a balance of $2,970.31 The check register of the account owner shows an ...

Test of Yanofsky’s Proposed trp Operon Gene Order

Test of Yanofsky’s Proposed trp Operon Gene Order