Answer to Question 1

C

Answer to Question 2

1a. Medical supplies rate = =

= 2,200 per patient-year

Rent and clinic maintenance rate = =

= 6.60 per square foot

Admin. cost rate for patient-charts food and laundry = =

= 4,400 per patient-year

Laboratory services rate = =

= 44 per test

These cost drivers are chosen as the ones that best match the descriptions of why the costs arise. Other answers are acceptable, provided that clear explanations are given.

1b. Activity-based costs for each program and cost per patient-year of the alcohol and drug program follow:

Drug After-Care Total

Direct labor

Physicians at 150,000 4; 0 600,000 600,000

Psychologists at 75,000 4; 8 300,000 600,000 900,000

Nurses at 30,000 6; 10 180,000 300,000 480,000

Direct labor costs 1,080,000 900,000 1,980,000

Medical supplies1 2,200 50; 60 110,000 132,000 242,000

Rent and clinic maintenance2

6.60 9,000; 12,000 59,400 79,200 138,600

Administrative costs to manage

patient charts, food, and laundry3

4,400 50; 60 220,000 264,000 484,000

Laboratory services4

44 1,400; 700 61,600 30,800 92,400

Total costs 1,531,000 1,406,000 2,937,000

Cost per patient-year

1Allocated using patient-years

2Allocated using square feet of space

3Allocated using patient-years

4Allocated using number of laboratory tests

1c. The ABC system more accurately allocates costs because it identifies better cost drivers. The ABC system chooses cost drivers for overhead costs that have a cause-and-effect relationship between the cost drivers and the costs. Of course, Yu should continue to evaluate if better cost drivers can be found than the ones they have identified so far.

By implementing the ABC system, Yu can gain a more detailed understanding of costs and cost drivers. This is valuable information from a cost management perspective. The system can yield insight into the efficiencies with which various activities are performed. Yu can then examine if redundant activities can be eliminated. Yu can study trends and work toward improving the efficiency of the activities.

In addition, the ABC system will help Yu determine which programs are the most costly to operate. This will be useful in making long-run decisions as to which programs to offer or emphasize. The ABC system will also assist Yu in setting prices for the programs that more accurately reflect the costs of each program.

2. The concern with using costs per patient-year as the rule to allocate resources among its programs is that it emphasizes input to the exclusion of outputs or effectiveness of the programs. After-all, Yu's goal is to cure patients while controlling costs, not minimize costs per-patient year. The problem, of course, is measuring outputs.

Unlike many manufacturing companies, where the outputs are obvious because they are tangible and measurable, the outputs of service organizations are more difficult to measure. Examples are cured patients as distinguished from processed or discharged patients, educated as distinguished from partially educated students, and so on.

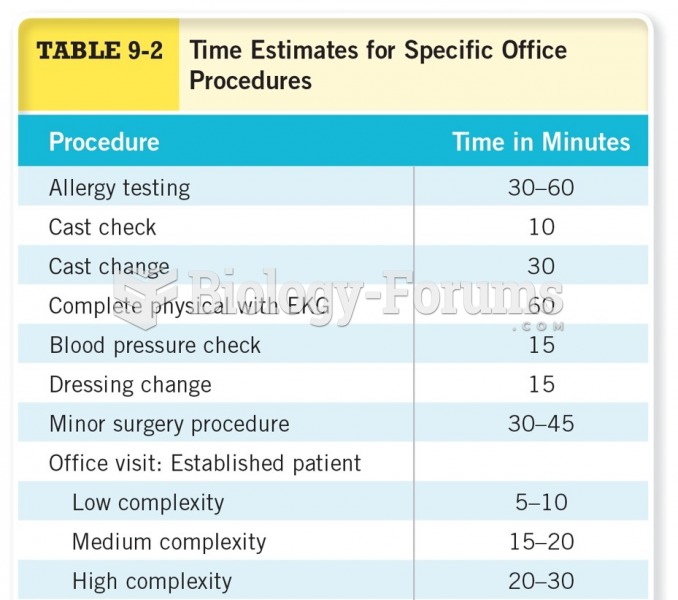

Time Estimates for Specific Office Procedures

Time Estimates for Specific Office Procedures

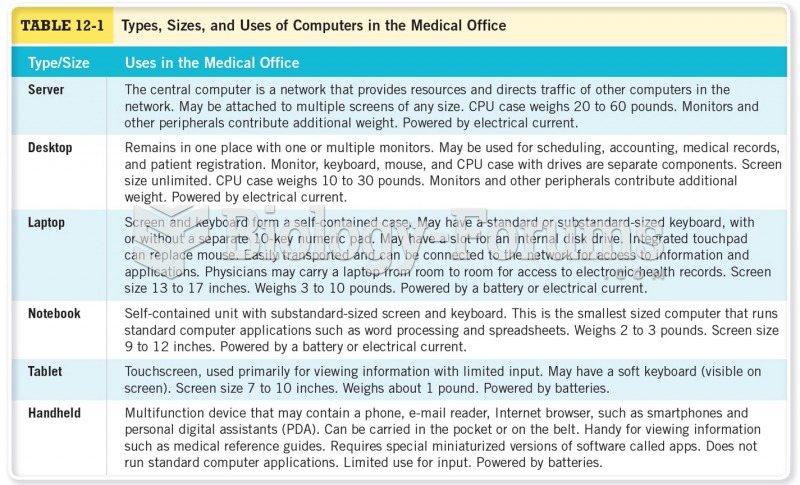

Types, Sizes, and Uses of Computers in the Medical Office

Types, Sizes, and Uses of Computers in the Medical Office

Example of equipment used for a urine drug screen that a medical office may require before ...

Example of equipment used for a urine drug screen that a medical office may require before ...

Every medical office should keep emergency supplies in a waterproof container.

Every medical office should keep emergency supplies in a waterproof container.

Computerized spirometry is used in medical office settings as well as in hospitals and other medical ...

Computerized spirometry is used in medical office settings as well as in hospitals and other medical ...

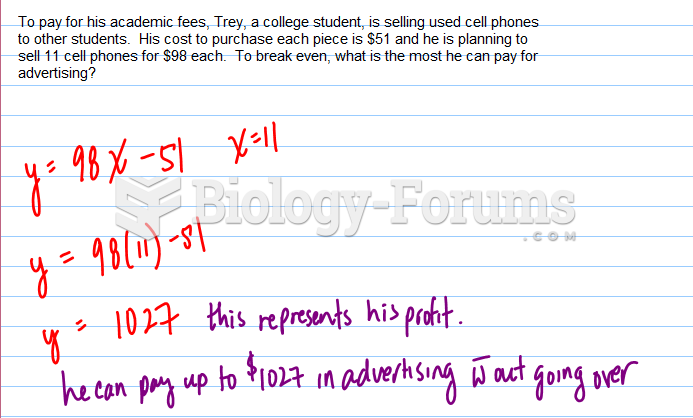

Advertising Break-even Question

Advertising Break-even Question