This topic contains a solution. Click here to go to the answer

|

|

|

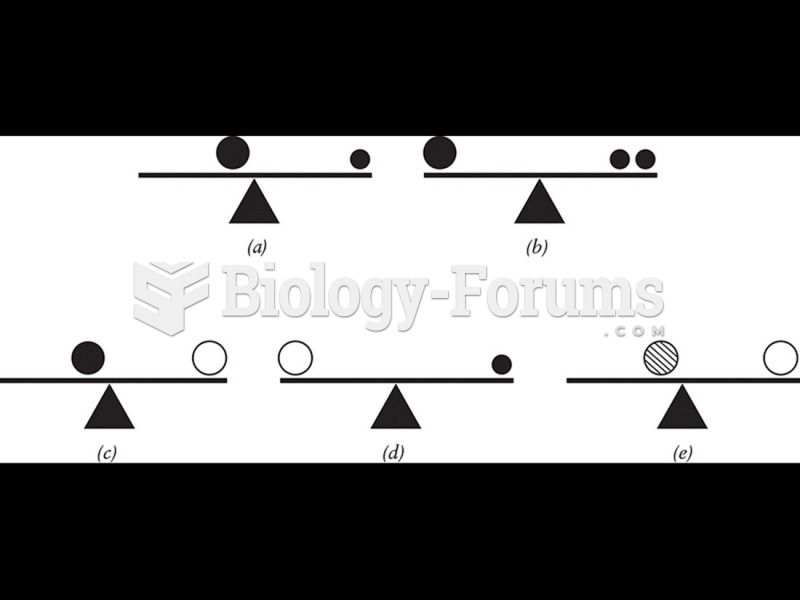

Some different varieties of asymmetrical balance.

Some different varieties of asymmetrical balance.

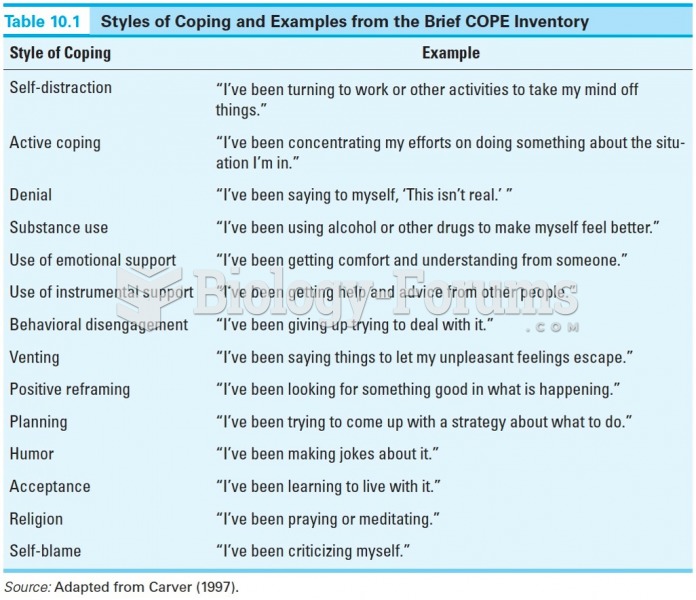

Styles of Coping and Examples from the Brief COPE Inventory

Styles of Coping and Examples from the Brief COPE Inventory

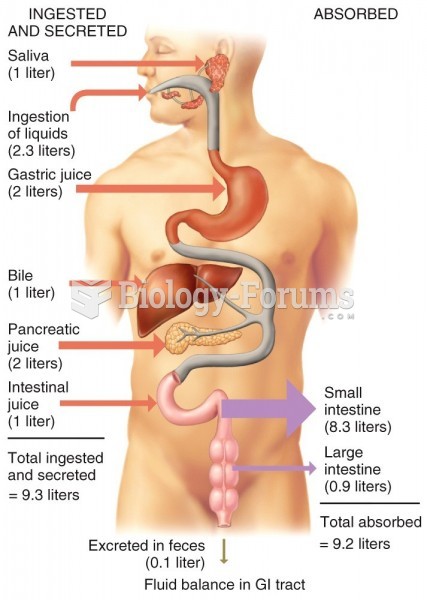

Fluid Balance during Exercise

Fluid Balance during Exercise

Fluid Balance

Fluid Balance

Acid–Base Balance

Acid–Base Balance

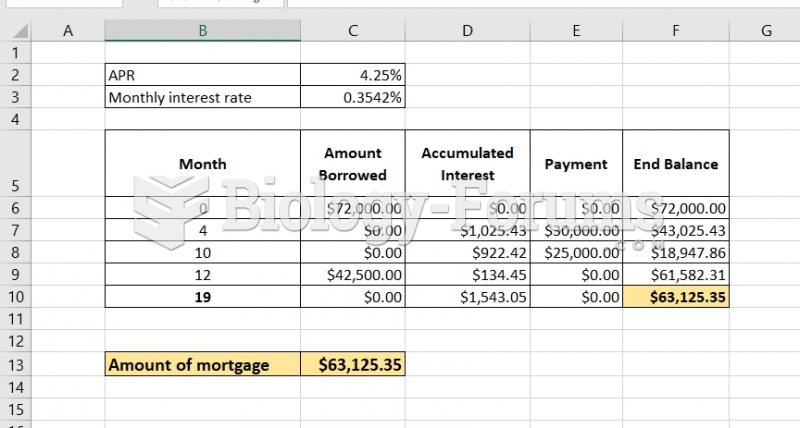

Raman has a line of credit loan with the ICICI bank. The initial loan balance was $72000.00. ...

Raman has a line of credit loan with the ICICI bank. The initial loan balance was $72000.00. ...