This topic contains a solution. Click here to go to the answer

|

|

|

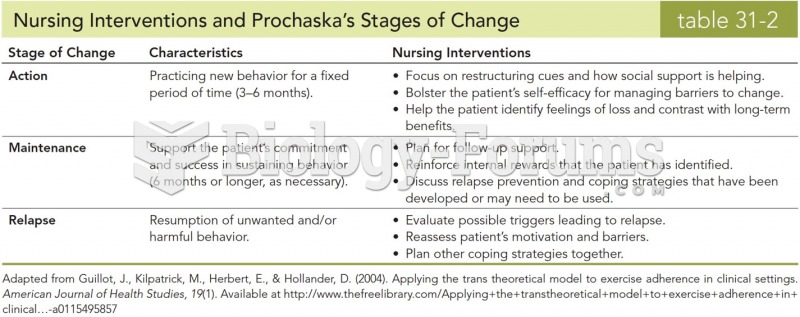

Nursing Interventions and Prochaska's Stages of Change

Nursing Interventions and Prochaska's Stages of Change

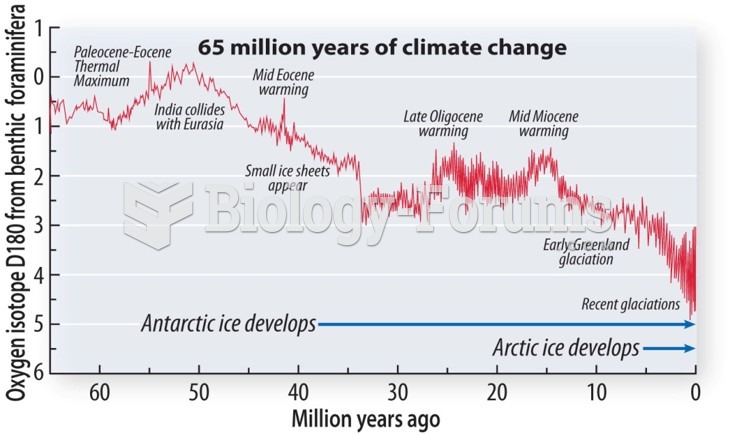

Ancient Climate Change: Following the Cretaceous

Ancient Climate Change: Following the Cretaceous

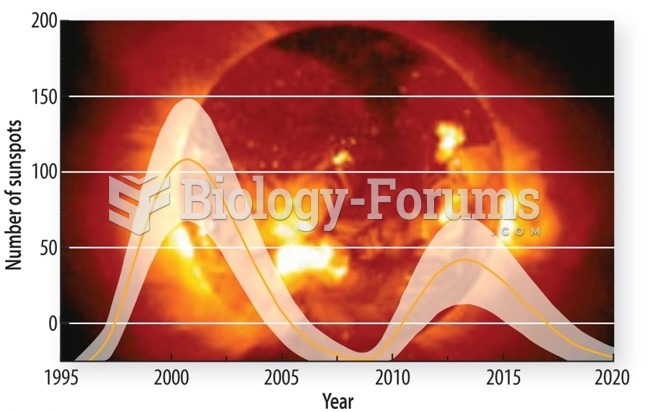

The Sun and climate change

The Sun and climate change

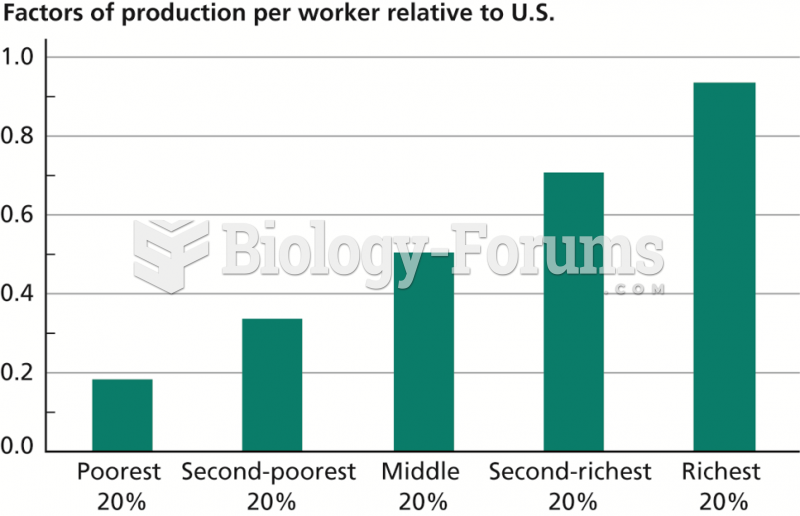

Role of Factors of Production in Determining Output per Worker, 2009

Role of Factors of Production in Determining Output per Worker, 2009

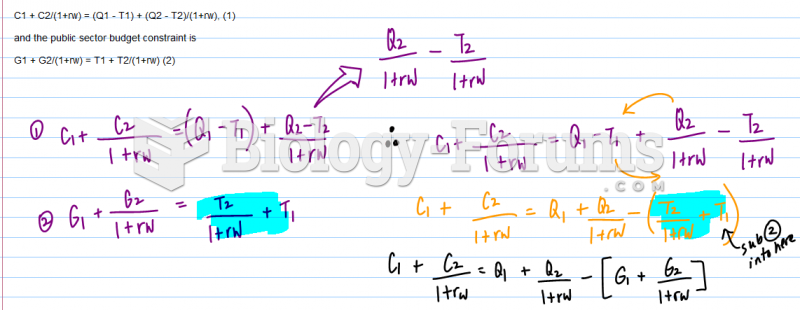

Consider a two-period economy with no investment opportunities: first and second period output ...

Consider a two-period economy with no investment opportunities: first and second period output ...

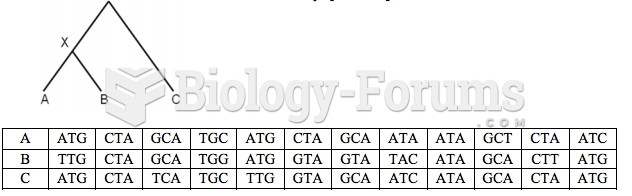

Outgroup role in relative rate test

Outgroup role in relative rate test