Answer to Question 1C

Answer to Question 21.

Architecture Firms Commercial Clients

Total Total Total

(all customers) Architecture AA BB Commercial CC DD EE

(1) = (2) + (5) (2) = (3) + (4) (3) (4) (5) = (6)+(7)+(

(6) (7) (

Gross Revenues 500,610 211,400 117,000 94,400 289,210 178,690 73,920 36,600

(less) Discounts 13,530 11,700 11,700 0 1,830 0 0 1,830

Net Revenues 487,080 199,700 105,300 94,400 287,380 178,690 73,920 34,770

Customer-level costs 327,770 132,100 73,500 58,600 195,670 109,290 57,860 28,520

Customer-level operating income 159,310 67,600 31,800 35,800 91,710 69,400 16,060 6,250

Distribution-channel (Overhead) costsa 110,630 42,550 68,080

Distribution-channel-level oper. income 48,680 25,050 23,630

Corporate-sustaining costsa 59,570

Operating income (10,890)

a Architecture: 25 170,200 = 42,550; Commercial: 40 170,200 = 68,080; Corporate-sustaining: 35 170,200 = 59,570;

2.

Cumulative

Customer-Level

Operating Income

Customer-Level Customer-Level Cumulative as a of Total

Operating Customer Operating Income Customer-Level Customer-Level

Customer Income Revenue as a of Revenue Operating Income Operating Income

Code (1) (2) (3) = (1) (2)

(4) (5) = (4) 159,310

CC 69,400 178,690 38.84 69,400 43.6

BB 35,800 94,400 37.92 105,200 66.0

AA 31,800 105,300 30.20 137,000 86.0

DD 16,060 73,920 21.73 153,060 96.1

EE 6,250 34,770 17.98 159,310 100.0

159,310 487,080

3. Interiors by Denise reported a net operating loss for the quarter. All of Denise's customers are profitable, but the presence of substantial corporate-sustaining costs led to the overall negative level of income. Offering a discount to Attractive Abodes in order to gain their business was a good move because even with the discount the customer contributed significant customer-level operating income, without affecting overall profit margins. Similarly, despite the discount offered to Elegant Extras for advance cash payment, Elegant Extras still provided a positive contribution to overall income. However, Elegant Extras was the least profitable customer on the basis of profit margins. It is possible that Denise gave the discount at a time when she needed liquidity, thereby trading off some income for immediate cash. Going forward, it is important to ensure that customers do not come to expect the same deal for every transaction.

Yet, despite all customers being profitable, Interiors by Denise showed a loss. This performance is not sustainable over the long run. Therefore Denise must work to reduce costs at all levels and/or to increase prices for her services. Increasing prices may cause Denise to be uncompetitive (she had to offer discounts to lure away Attractive Abodes), so before she does so, Denise must look to increase the efficiency of her operations and to reduce costs.

Answer to Question 31. Direct materials and direct manufacturing labor are analyzed in turn:

Actual Costs

Incurred

(Actual Input Qty.

Actual Price)

Actual Input Qty.

Budgeted Price Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

Budgeted Price)

Direct

Materials

(100,000 4.65a)

465,000 Purchases Usage

(100,000 4.50) (98,055 4.50)

450,000 441,248

(9,850 10 4.50)

443,250

15,000 U 2,002 F

Price variance Efficiency variance

Direct

Manufacturing

Labor

(4,900 31.5b)

154,350

(4,900 30)

147,000

(9,850 0.5 30) or

(4,925 30)

147,750

7,350 U 750 F

Price variance Efficiency variance

a 465,000 100,000 = 4.65

b 154,350 4,900 = 31.5

2. Direct Materials Control 450,000

Direct Materials Price Variance 15,000

Accounts Payable or Cash Control 465,000

Work-in-Process Control 443,250

Direct Materials Control 441,248

Direct Materials Efficiency Variance 2,002

Work-in-Process Control 147,750

Direct Manuf. Labor Price Variance 7,350

Wages Payable Control 154,350

Direct Manuf. Labor Efficiency Variance 750

3. Some students' comments will be immersed in conjecture about higher prices for materials, better quality materials, higher-grade labor, better efficiency in use of materials, and so forth. A possibility is that approximately the same labor force, paid somewhat more, is taking slightly less time with better materials and causing less waste and spoilage.

A key point in this problem is that all of these efficiency variances are likely to be insignificant. They are so small as to be nearly meaningless. Fluctuations about standards are bound to occur in a random fashion. Practically, from a control viewpoint, a standard is a band or range of acceptable performance rather than a single-figure measure.

4. The purchasing point is where responsibility for price variances is found most often. The production point is where responsibility for efficiency variances is found most often. The Schuyler Corporation may calculate variances at different points in time to tie in with these different responsibility areas.

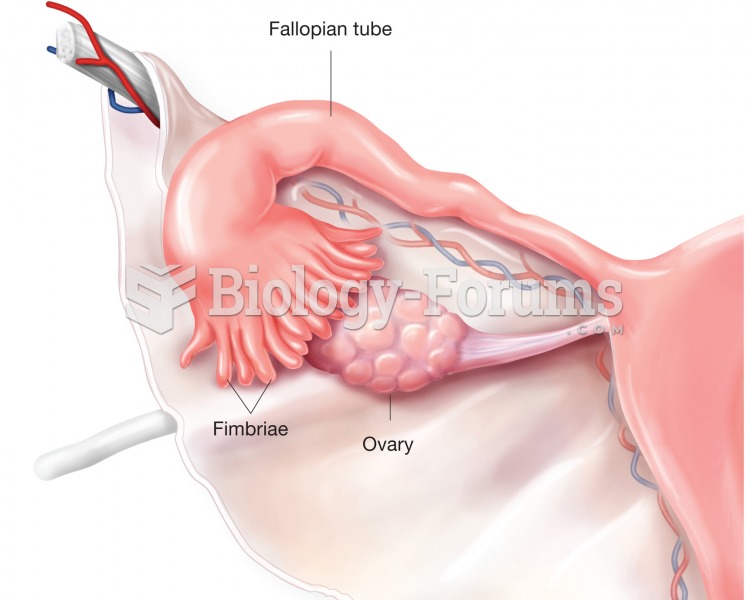

The ovaries. In addition to producing ova, the ovaries secrete the female sex hormones, estrogen and

The ovaries. In addition to producing ova, the ovaries secrete the female sex hormones, estrogen and

The couple discusses grief over the loss of a child.

The couple discusses grief over the loss of a child.

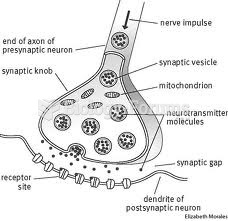

PhysioEx 9.0 Review Sheet Exercise 3

PhysioEx 9.0 Review Sheet Exercise 3

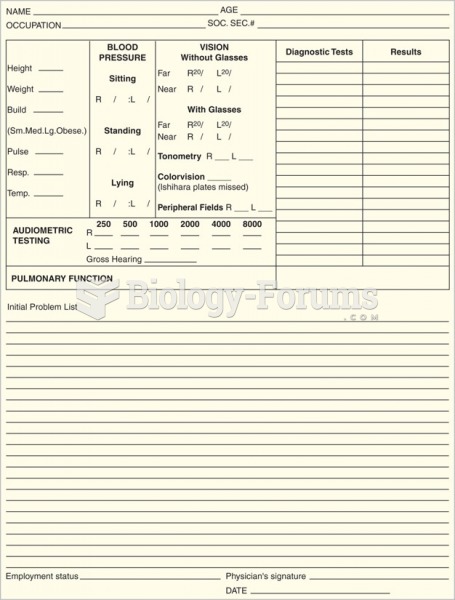

An example of a medical history sheet to list patient problems.

An example of a medical history sheet to list patient problems.

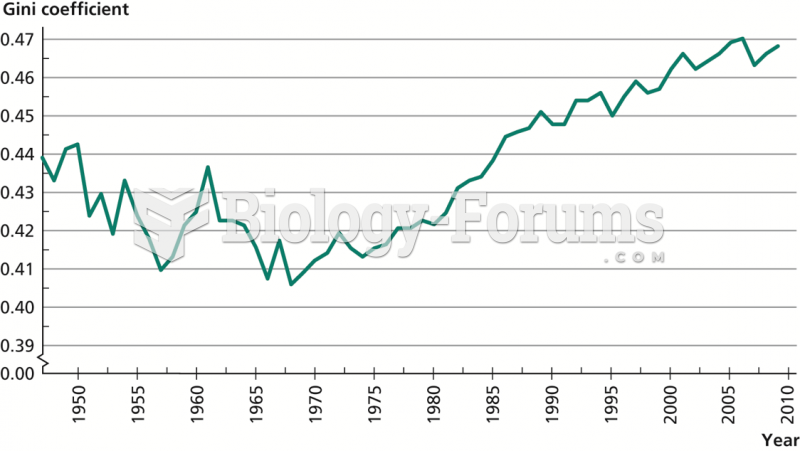

Income Inequality in the United States: 1947–2009

Income Inequality in the United States: 1947–2009

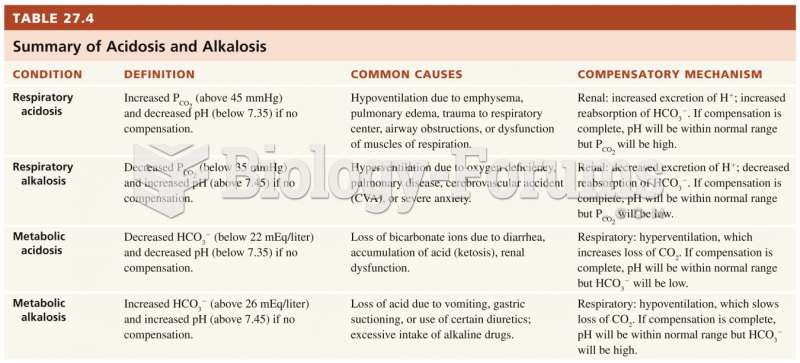

Acid–Base Balance

Acid–Base Balance