Answer to Question 1

B

Answer to Question 2

1. The opportunity cost to Wild Orchid of producing the 3,500 units of Stronglast is the contribution margin lost on the 3,500 units of Everlast that would have to be forgone, as computed below:

Selling price

Variable costs per unit:

Direct materials

Direct manufacturing labor

Variable manufacturing overhead

Variable marketing costs

Contribution margin per unit

Contribution margin for 3,500 units (28 3,500 units) 52

10

2

8

4 24

28

98,000

The opportunity cost is 98,000. Opportunity cost is the maximum contribution to operating income that is forgone (rejected) by not using a limited resource in its next-best alternative use.

2. Contribution margin from manufacturing 3,500 units of Stronglast and purchasing 3,500 units of Everlast from Chesapeake is 105,000, as follows:

Manufacture

Stronglast Purchase

Everlast

Total

Selling price

Variable costs per unit:

Purchase costs

Direct materials

Direct manufacturing labor

Variable manufacturing costs

Variable marketing overhead

Variable costs per unit

Contribution margin per unit

Contribution margin from selling 3,500 units of Stronglast and 3,500 units of Everlast

(18 3,500 units; 12 3,500 units) 40

10

2

8

2

22

18

63,000 52

36

4

40

12

42,000

105,000

As calculated in requirement 1, Wild Orchid's contribution margin from continuing to manufacture 3,500 units of Everlast is 98,000. Accepting the Apex Company and Chesapeake offer will benefit Wild Orchid by 7,000 (105,000 98,000). Hence, Wild Orchid should accept the Apex Company and Chesapeake Corporation's offers.

3. The minimum price would be any price greater than 22, the sum of the incremental costs of manufacturing and marketing Stronglast as computed in requirement 2. This follows because, if Wild Orchid has surplus capacity, the opportunity cost = 0. For the short-run decision of whether to accept Apex's offer, fixed costs of Wild Orchid are irrelevant. Only the incremental costs need to be covered for it to be worthwhile for Wild Orchid to accept the Apex offer.

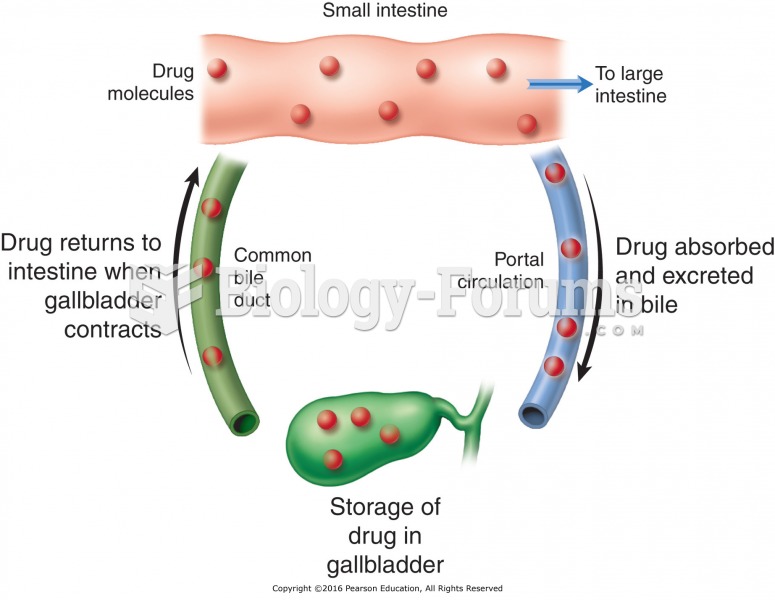

Enterohepatic recirculation of a drug can increase its half-life in the body and prolong its ...

Enterohepatic recirculation of a drug can increase its half-life in the body and prolong its ...

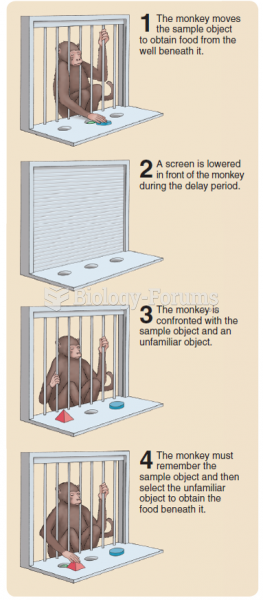

Performance of a delayed nonmatching-to-sample trial.

Performance of a delayed nonmatching-to-sample trial.

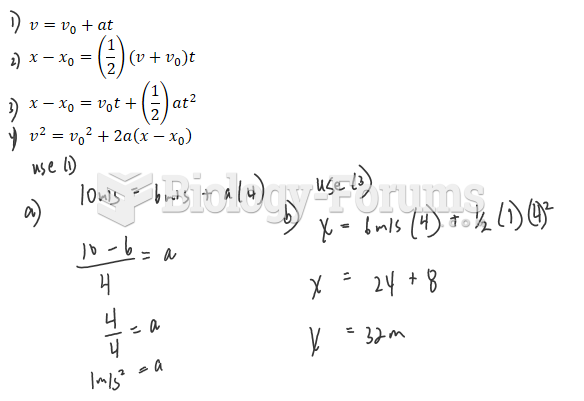

How to solve optimization problems in calculus (Question 8)

How to solve optimization problems in calculus (Question 8)

Acid–Base Balance

Acid–Base Balance

Physics - Motion (Please help me solve these problems, I really need help)

Physics - Motion (Please help me solve these problems, I really need help)

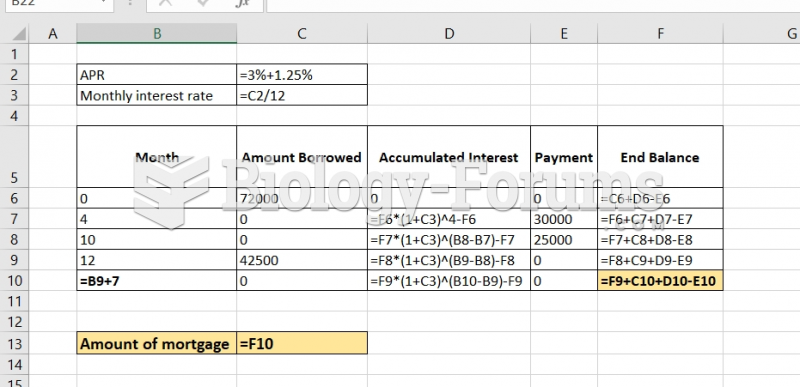

Raman has a line of credit loan with the ICICI bank. The initial loan balance was $72000.00. ...

Raman has a line of credit loan with the ICICI bank. The initial loan balance was $72000.00. ...