This topic contains a solution. Click here to go to the answer

|

|

|

True Forget-Me-Not

True Forget-Me-Not

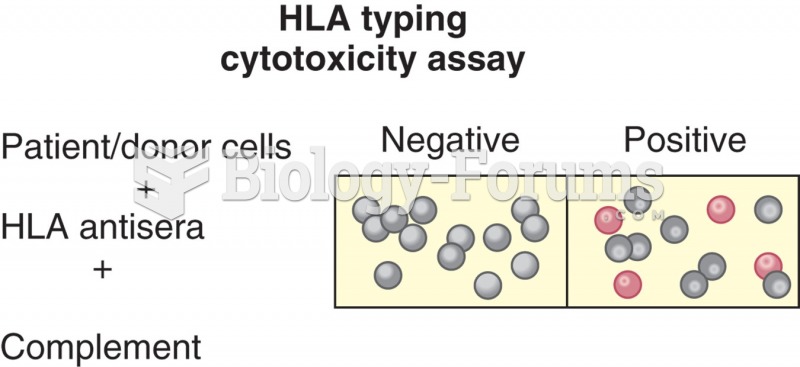

Principle of a microcytotoxicity assay.

Principle of a microcytotoxicity assay.

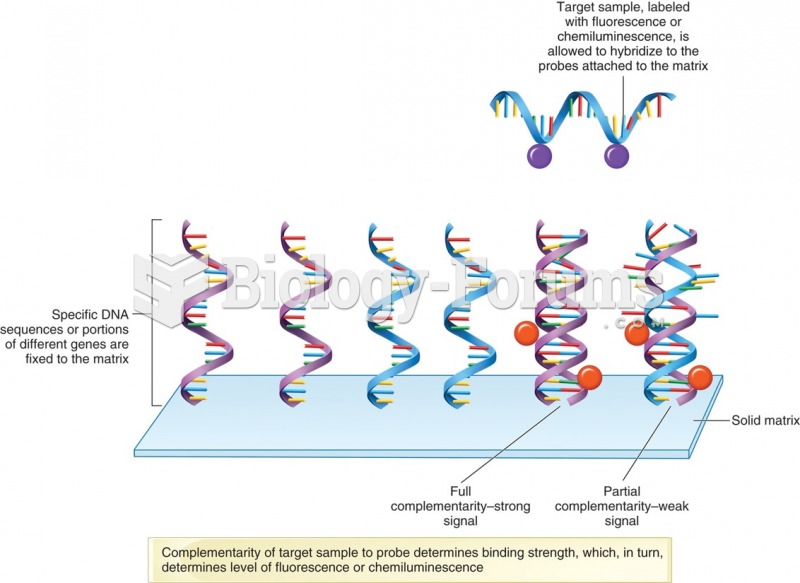

Basic principle of target-probe hybridization in microarray chips.

Basic principle of target-probe hybridization in microarray chips.

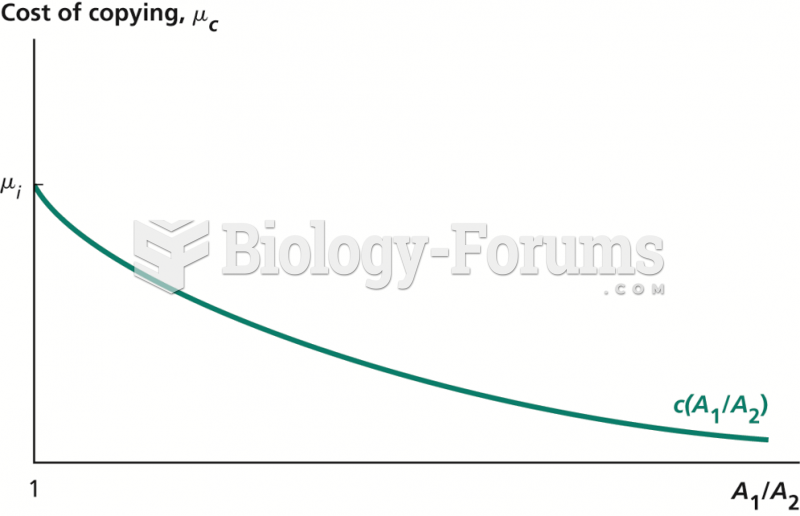

Cost of Copying for the Follower Country

Cost of Copying for the Follower Country

Physics - Pressure, Density, Pascal's Principle

Physics - Pressure, Density, Pascal's Principle

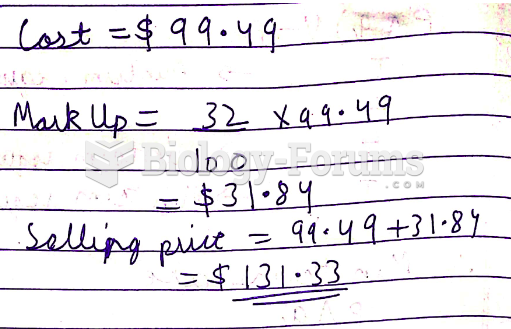

Cost = $99.49; Rate of markup based on cost = 32%. Find the markup and selling price.

Cost = $99.49; Rate of markup based on cost = 32%. Find the markup and selling price.