This topic contains a solution. Click here to go to the answer

|

|

|

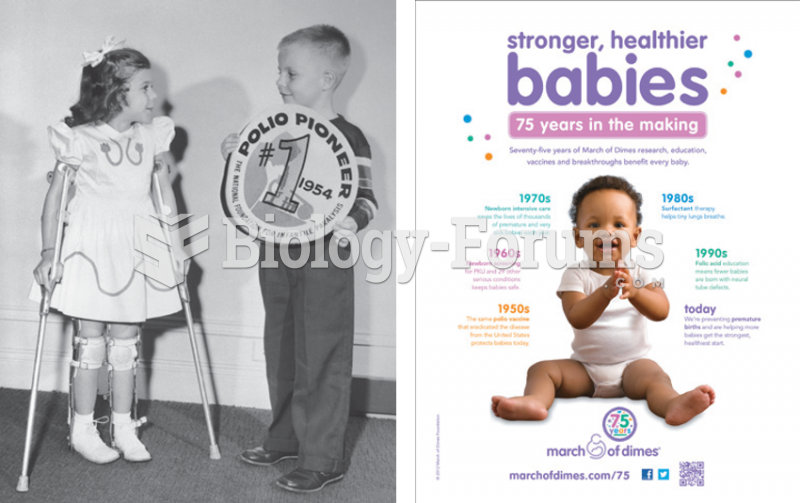

The March of Dimes

The March of Dimes

Legal Environment of Business: Online Commerce, Ethics, and Global Issues (Cheeseman)

Legal Environment of Business: Online Commerce, Ethics, and Global Issues (Cheeseman)

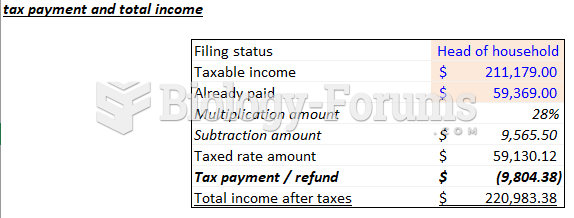

Business Math Question Solution

Business Math Question Solution

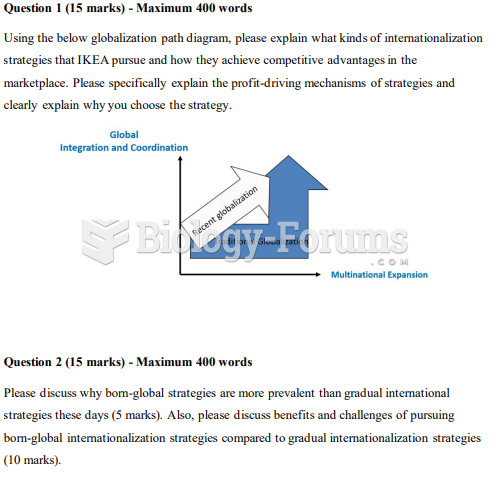

International Business Management

International Business Management

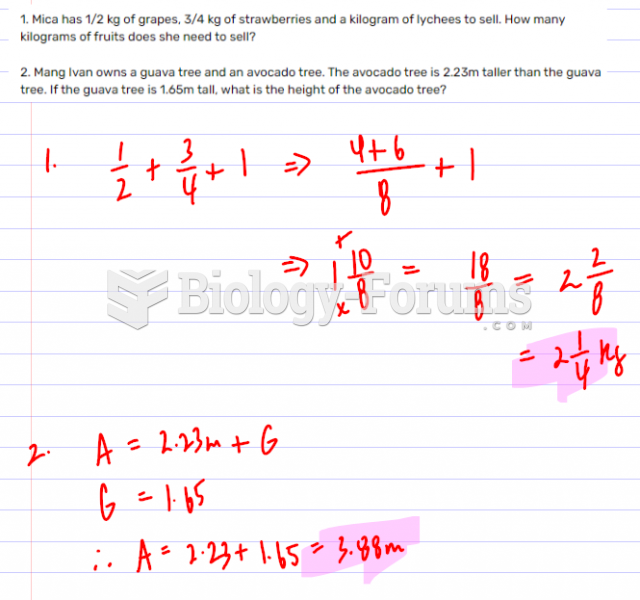

Business Math

Business Math

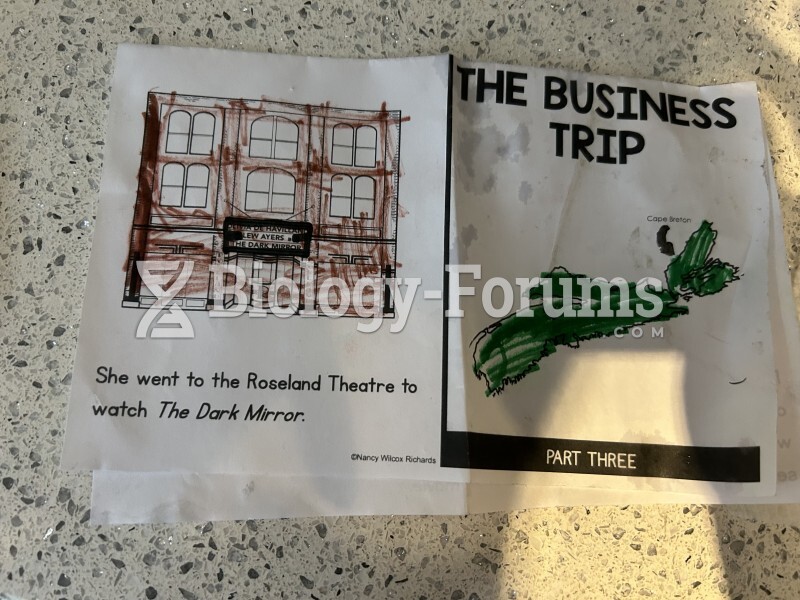

The business trip grade 1

The business trip grade 1