Tiger Pride produces two product lines: T-shirts and Sweatshirts. Product profitability is analyzed as follows:

| Production and sales volume | 192,000 units | 24,000 units |

| Selling price | $17.00 | $29.00 |

| Direct material | $1.70 | $ 5.00 |

| Manufacturing overhead | $3.50 | $ 3.00 |

| Selling and administrative | $4.10 | $ 7.00 |

| Operating profit | $3.40 | $ 6.80 |

Tiger Pride's managers have decided to revise their current assignment of overhead costs to reflect the following ABC cost information:

| Activity | Activity cost | Activity-cost driver |

| Supervision | $123,480 | Direct labor hours (DLH) |

| Inspection | $104,800 | Inspections |

| T-SHIRTS | SWEATSHIRTS |

| 0.25 DLH/unit | 1.50 DLH/unit |

| 48,000 DLHs | 36,000 DLHs |

| 50,000 inspections | 15,500 inspections |

Under the revised ABC system, supervision costs allocated to Sweatshirts will be ________. (Do not round interim calculations. Round the final answer to the nearest whole dollar.)

◦ $52,920

◦ $104,800

◦ $123,480

◦ None of these answers are correct.

Sumatran Tiger

Sumatran Tiger

Skeleton of tiger quoll

Skeleton of tiger quoll

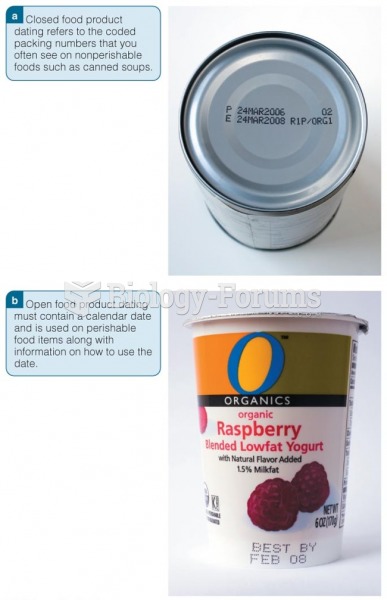

Closed and Open Food Product Dating

Closed and Open Food Product Dating

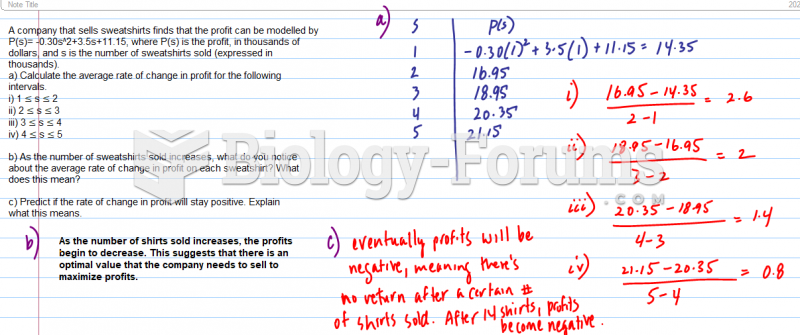

A company that sells sweatshirts finds that the profit can be modelled by P(s)= ...

A company that sells sweatshirts finds that the profit can be modelled by P(s)= ...