This topic contains a solution. Click here to go to the answer

|

|

|

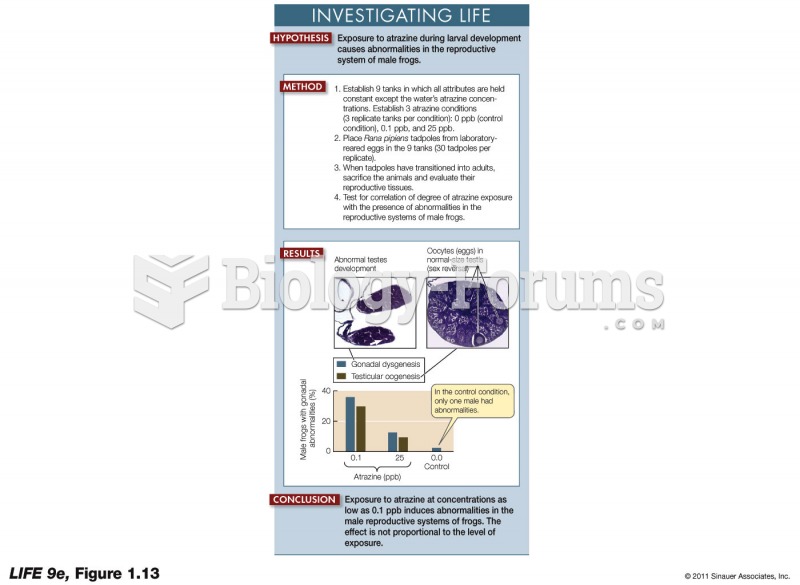

Controlled Experiments Manipulate a Variable

Controlled Experiments Manipulate a Variable

How to solve a linear system when the variable is in the denominator position (Question 2 of 2)

How to solve a linear system when the variable is in the denominator position (Question 2 of 2)

Triceps and Side Stretch With Arm Overhead.

Triceps and Side Stretch With Arm Overhead.

If the random variable x is exponentially distributed with parameter λ = 4, then P(x ≤ ...

If the random variable x is exponentially distributed with parameter λ = 4, then P(x ≤ ...

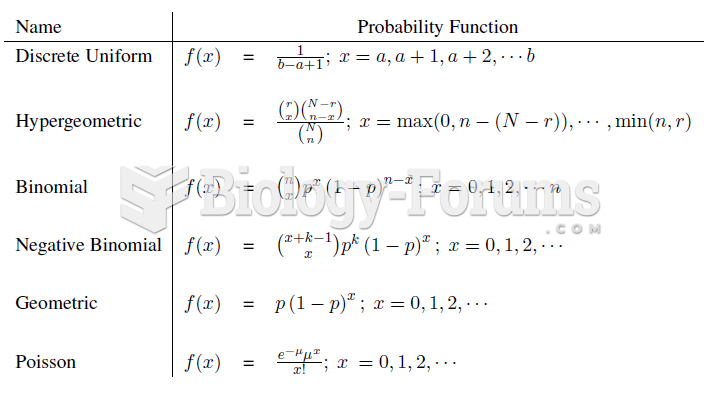

Summary of Single Variable Discrete Models

Summary of Single Variable Discrete Models

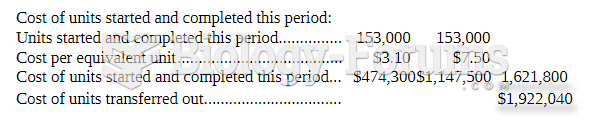

The following information relates to the Cutting Department of Kittina Corporation for the ...

The following information relates to the Cutting Department of Kittina Corporation for the ...