This topic contains a solution. Click here to go to the answer

|

|

|

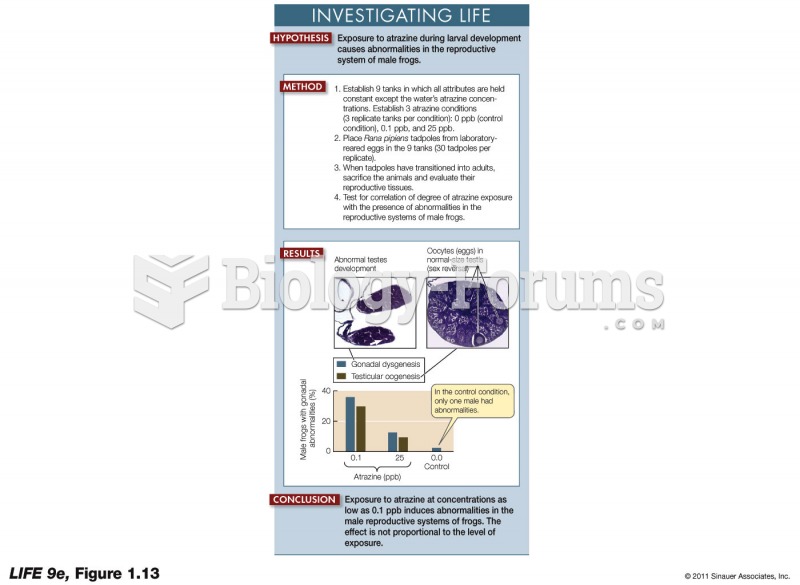

Controlled Experiments Manipulate a Variable

Controlled Experiments Manipulate a Variable

The Real Reason Why They Repeat the Same 20 Songs on the Radio & TV Nationwide

The Real Reason Why They Repeat the Same 20 Songs on the Radio & TV Nationwide

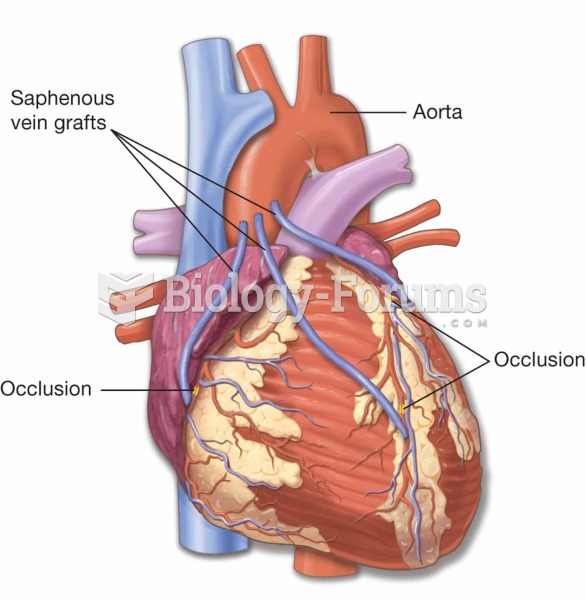

A coronary artery bypass graft (CABG) is a procedure to bypass a blocked coronary artery. The proced

A coronary artery bypass graft (CABG) is a procedure to bypass a blocked coronary artery. The proced

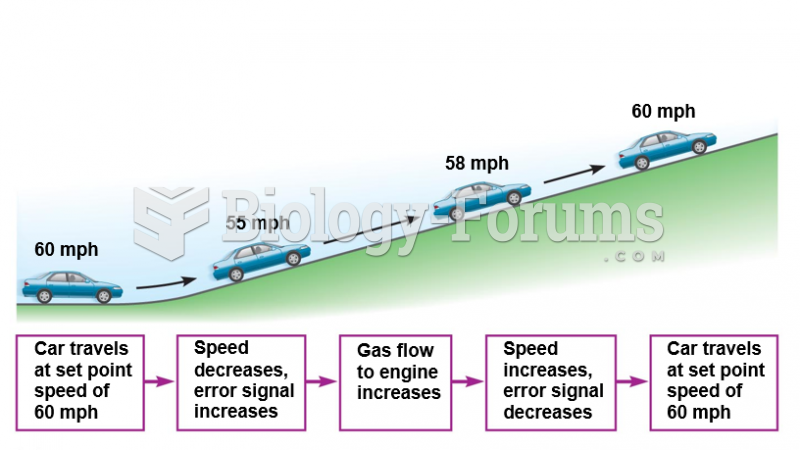

Negative feedback control of a regulated variable.

Negative feedback control of a regulated variable.

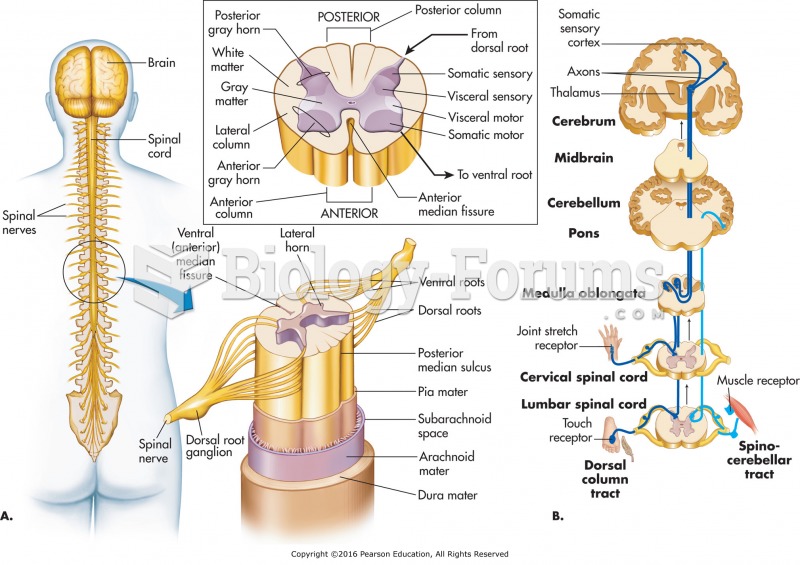

(A) Internal anatomy of the spinal cord. (B) Ascending spinal tracts.

(A) Internal anatomy of the spinal cord. (B) Ascending spinal tracts.

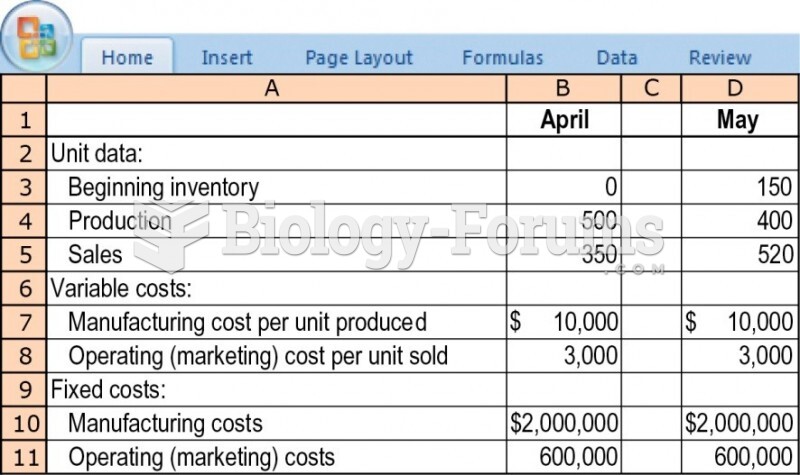

Variable and absorption costing, explaining operating-income differences.

Variable and absorption costing, explaining operating-income differences.