This topic contains a solution. Click here to go to the answer

|

|

|

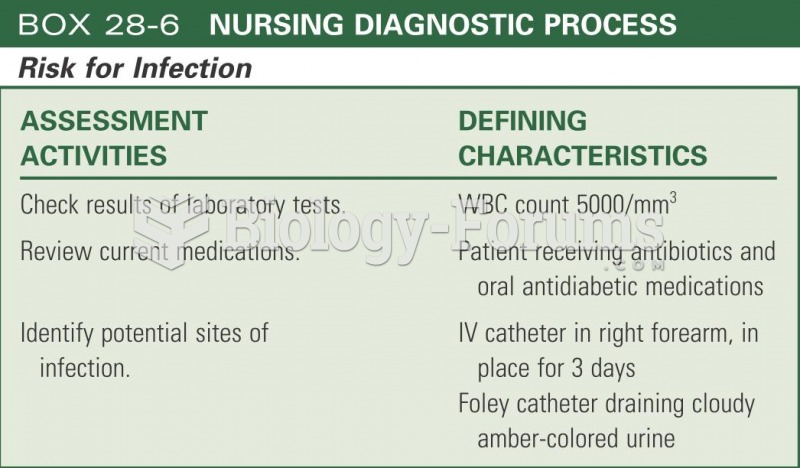

Nursing diagnositic process - risk for infection

Nursing diagnositic process - risk for infection

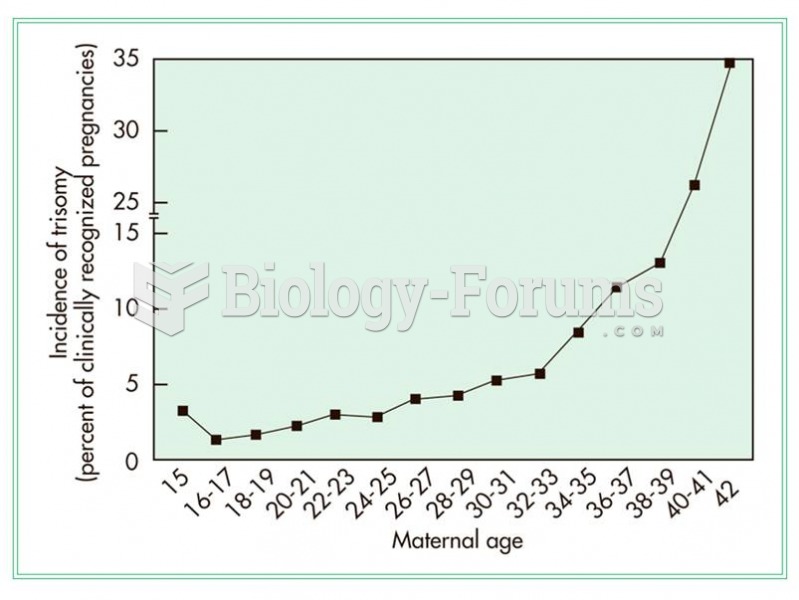

Increased risk of trisomy with maternal age.

Increased risk of trisomy with maternal age.

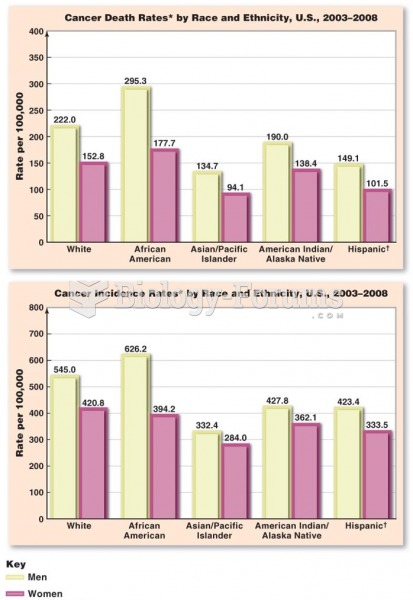

U.S. Cancer Risk—Racial Diversity

U.S. Cancer Risk—Racial Diversity

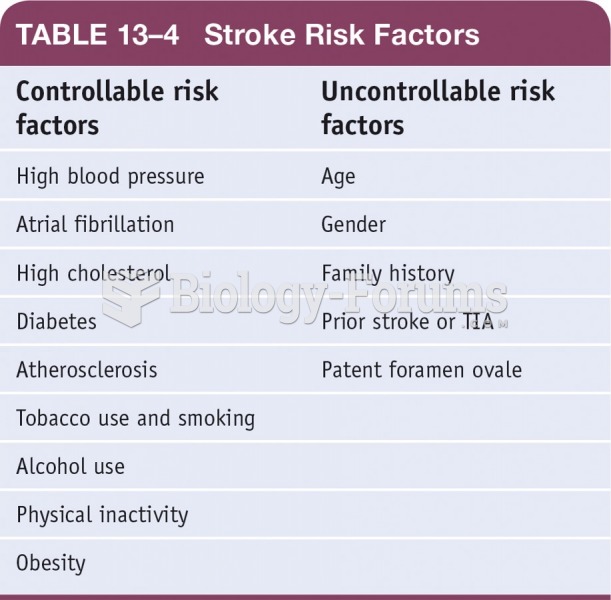

Stroke Risk Factors

Stroke Risk Factors

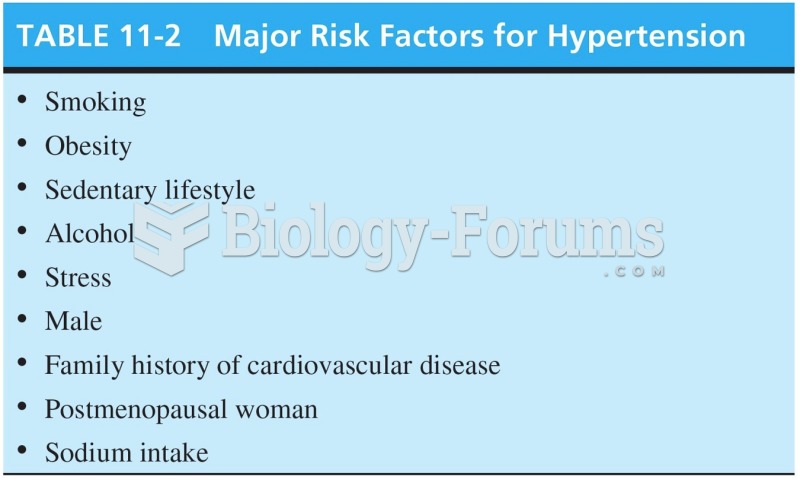

Major Risk Factors for Hypertension

Major Risk Factors for Hypertension

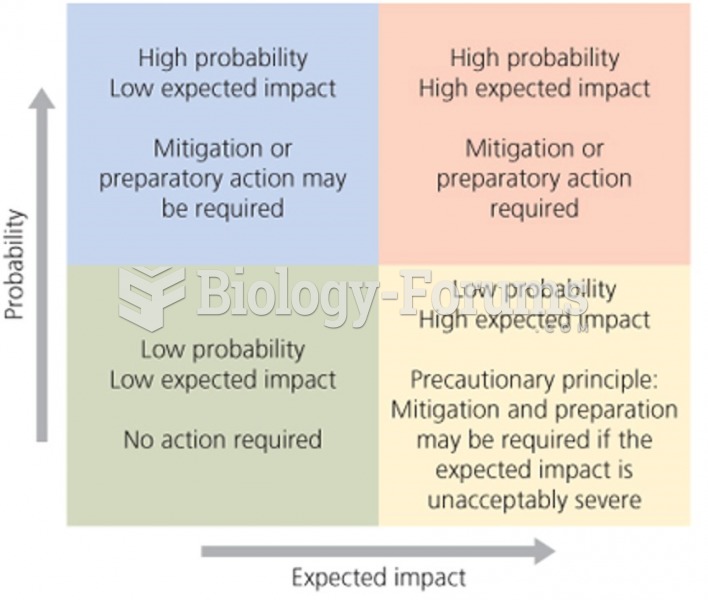

Risk assessment analyzes

Risk assessment analyzes