Answer to Question 1

Answer: There are two methods to consider. First, you can make 24 equal payments of = 1,250. This will pay off the entire loan before interest is charged. Second, you can make the regular 7 APR payments for two years and then pay off the balance with what is called a balloon payment. The PVIFA factor for 6 12 = 72 periods and a periodic interest rate of = 0.58333 is:

PVIFA = 58.65444. The monthly annuity payment is: PMT = = = 511.47. The total monthly payments for two years would be 24 511.47 = 12,275.28. Therefore, your balloon payment at the end of two years would be 30,000.00 - 12,275.28 = 17,724.72.

Answer to Question 2

Answer: There are two methods to consider. First, you can make 24 equal payments of = 833.33. This will pay off all of the loan before interest is charged. Second, you can make the regular 8 APR payments for two years and then pay off the balance with what is called a balloon payment. The PVIFA factor for 5 12 = 60 periods and a periodic interest rate of = 0.66667 is 49.31843. The monthly annuity payment is: PMT = = = 405.53. The total monthly payments for two years would be 24 405.53 = 9,732.67. Therefore, your balloon payment at the end of two years would be 20,000.00 - 9,732.67 = 10,267.33. Do the two methods imply that money is free? The answer is yes only if you are willing to make the loan period last just two years and can either (i) increase your monthly payments to 833.33 or (ii) pay off the balloon balance of 10,267.33 at the end of the second year following 24 equal payments of 405.53. For many people, these two options may not be feasible. For example, many people may find 833.33 a month for a car loan too much for their budget even if for only two years, and it may be even more difficult to come up with a balloon payment of 10,267.33 after the two-year period.

The 2012 U.S. presidential campaign rang with “get tough” cries to end Iran’s nuclear capacity and c

The 2012 U.S. presidential campaign rang with “get tough” cries to end Iran’s nuclear capacity and c

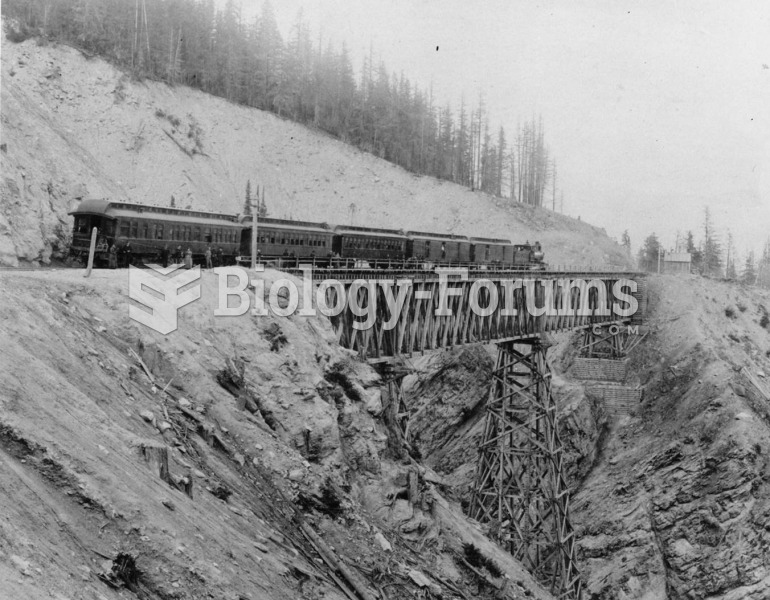

A passenger train crosses Stony Creek Bridge in the Rocky Mountains in 1878. Railroads were importan

A passenger train crosses Stony Creek Bridge in the Rocky Mountains in 1878. Railroads were importan

Midway Island, an inhospitable atoll acquired in 1867, was valuable as a military base located midwa

Midway Island, an inhospitable atoll acquired in 1867, was valuable as a military base located midwa

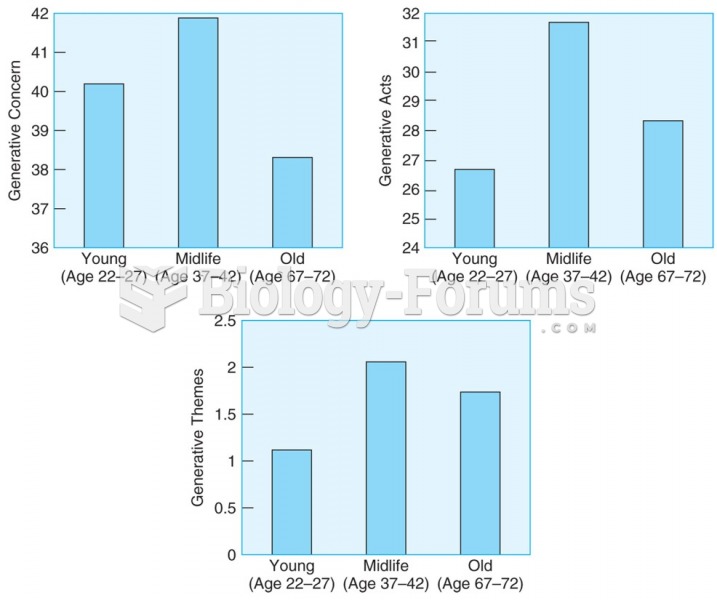

Adults in the middle-aged group (37–42 years) score higher on measures of generativity than either ...

Adults in the middle-aged group (37–42 years) score higher on measures of generativity than either ...

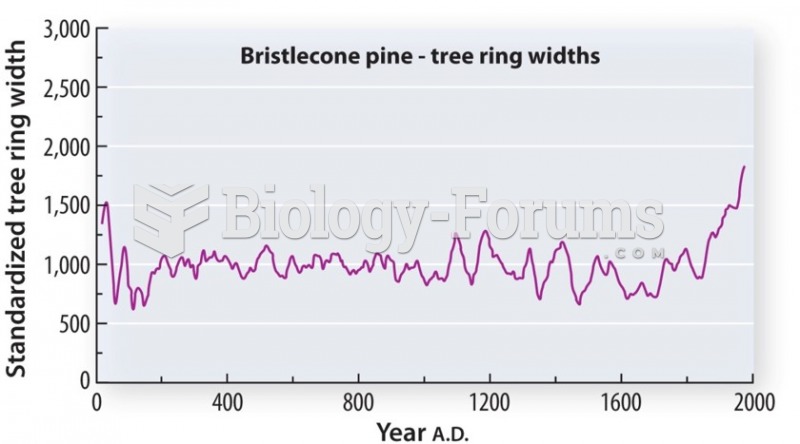

An overlapping record extends back thousands of years of tree ring width

An overlapping record extends back thousands of years of tree ring width

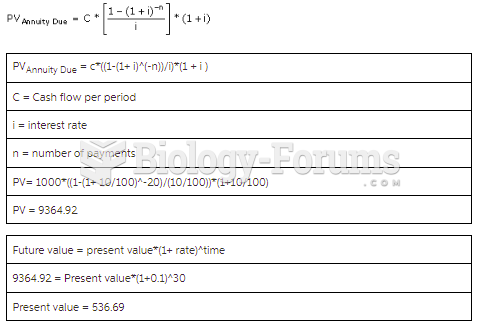

Charlie Stone wants to retire in 30 years, and he wants to have an annuity of $1000 a year for ...

Charlie Stone wants to retire in 30 years, and he wants to have an annuity of $1000 a year for ...