Answer to Question 1

Because of the legal implications involved in denying credit, legal counsel should review your credit denial messages to ensure that they comply with laws related to fair credit practices. The Equal Credit Opportunity Act (ECOA) requires that a credit applicant be notified of the credit decision within 30 calendar days following application. Applicants who are denied credit must be informed of the reasons for the refusal. If the decision was based on information obtained from a consumer reporting agency (as opposed to financial statements or other information provided by the applicant), the credit denial must include the name, address, and telephone number of the agency. It must also remind applicants that the Fair Credit Reporting Act provides them the right to know the nature of the information in their credit file. In addition, credit denials must include a standard statement that the ECOA prohibits creditors from discriminating against credit applicants on the basis of a number of protected characteristics, such as race, color, religion, national origin, sex, marital status, and age.

To avoid litigation, some companies choose to omit the explanation from the credit denial letter and invite the applicant to call or come in to discuss the reasons. Alternately, they might suggest that the audience obtain further information from the credit reporting agency whose name, address, and telephone number are provided.

Answer to Question 2

Resale refers to a discussion of goods or services already bought. Sales promotional material refers to statements made about related merchandise or service. Both of these messages can be effectively used when responding to a request for an adjustment. They remind the customer that they made a good choice in selecting the product or service. Such subtle sales messages may be read by the customer or client, while direct sales messages may not be read.

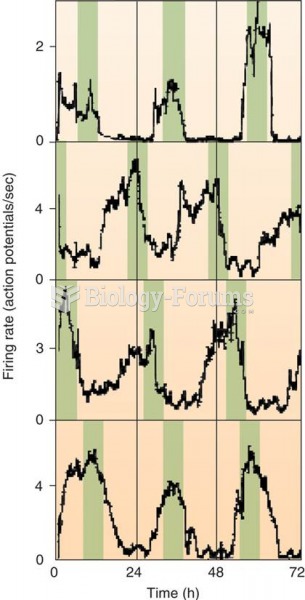

Firing Rate of Individual SCN Neurons in a Tissue Culture Color bars have been added to emphasize th

Firing Rate of Individual SCN Neurons in a Tissue Culture Color bars have been added to emphasize th

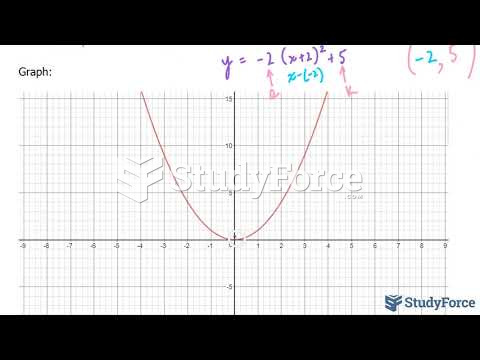

How to sketch a quadratic equation using transformations after completing the square (Question 2)

How to sketch a quadratic equation using transformations after completing the square (Question 2)

Language and Color Perception

Language and Color Perception

Describe the Conceptual Forecasting Framework in your own words.

Describe the Conceptual Forecasting Framework in your own words.

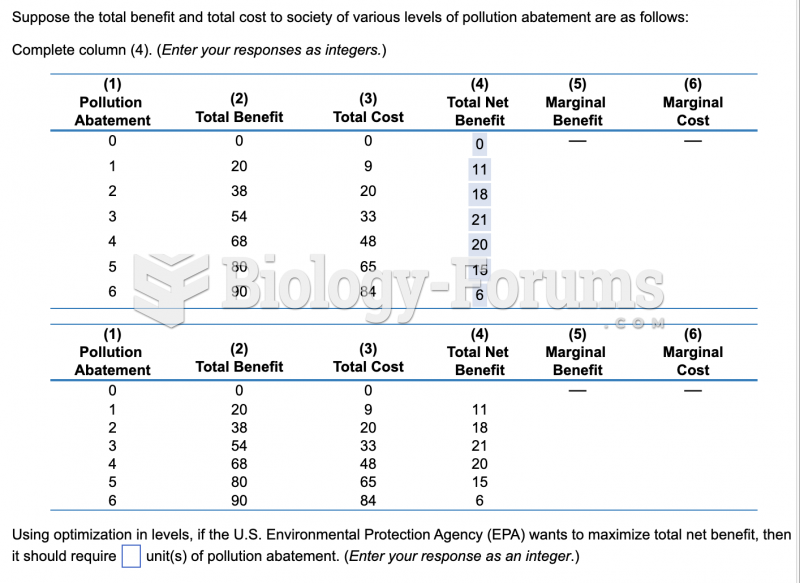

economic question

economic question

Genetic complementation analysis of Drosophila eye color mutants

Genetic complementation analysis of Drosophila eye color mutants