Insurer's Defenses. Kirk Johnson applied for life insurance with New York Life Insur-ance Co on October 7, 1986. In answer to a question about smoking habits, Johnson stated that he had not smoked in the past twelve months and that he had never smoked cigarettes. In fact, Johnson had smoked for thirteen years, and during the month prior to the insurance appli-cation, he was smoking approximately ten cigarettes per day. Johnson died on July 17, 1988, for reasons unrelated to smoking. Johnson's father, Lawrence Johnson, who was the benefi-ciary of the policy, filed a claim for the insurance proceeds. While investigating the claim, New York Life discovered Kirk Johnson's misrepresentation and denied the claim. The company canceled the policy and sent Lawrence Johnson a check for the premiums that had been paid. Lawrence Johnson refused to accept the check, and New York Life brought an action for a declaratory judgment (a court determination of a plaintiff's rights). What should the court decide? Discuss fully.

Question 2

A company that has more than 25,000 worth of business with the federal government and does not notify employees that as a condition of employment, the employer must be notified of any drug-related convictions that occur, and the employer must notify the federal government would be in violation of:

a. the Drug Prohibition Act

b. the Drug Control in the Workplace Act c. the Drug-Free Workplace Act

d. the Zero Tolerance Act

e. the Drug Prevention in the Workplace Act

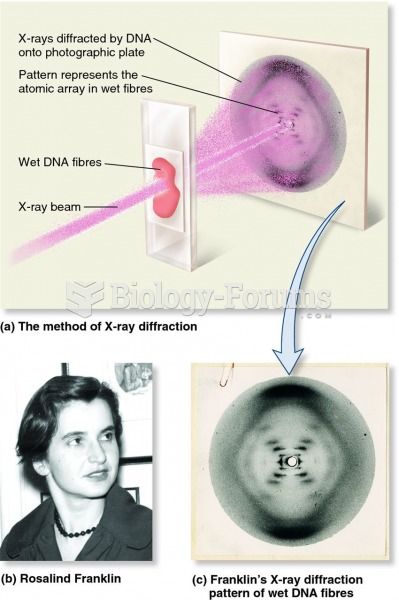

Rosalind Franklin and X-ray diffraction applied to DNA wet fibres

Rosalind Franklin and X-ray diffraction applied to DNA wet fibres

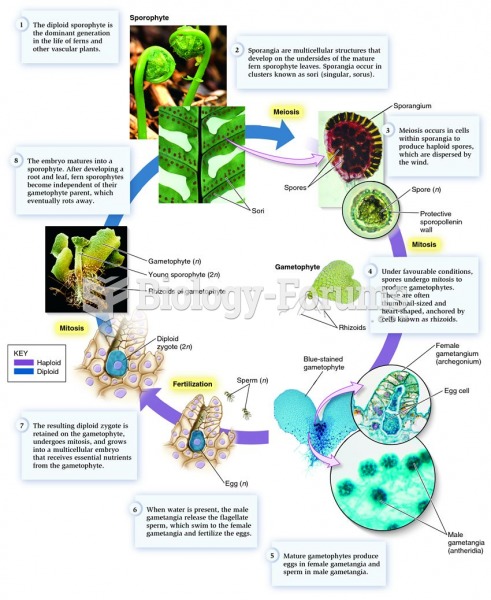

The life cycle of a typical fern.

The life cycle of a typical fern.

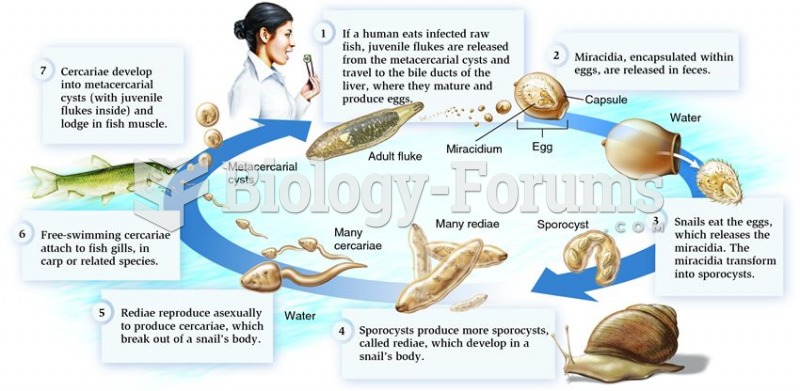

The complete life cycle of a trematode.

The complete life cycle of a trematode.

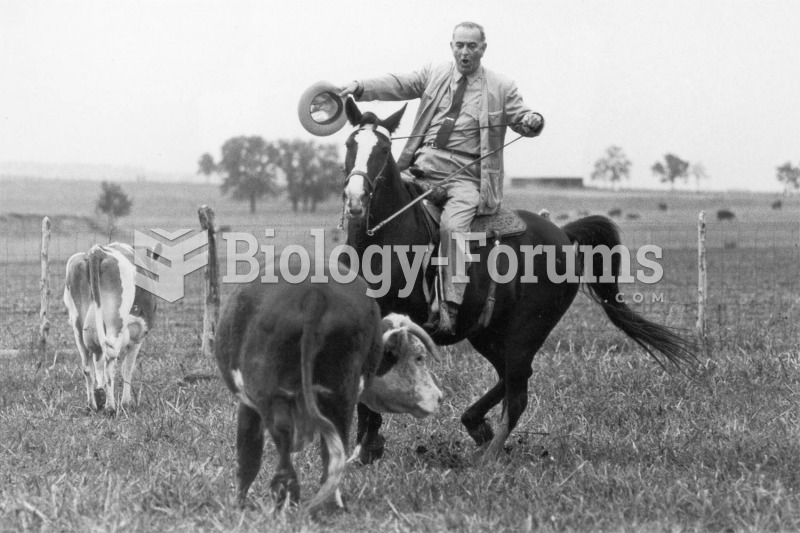

LBJ cultivated the masculine image of a Texas cowboy. Biographers have suggested that Johnson was ...

LBJ cultivated the masculine image of a Texas cowboy. Biographers have suggested that Johnson was ...

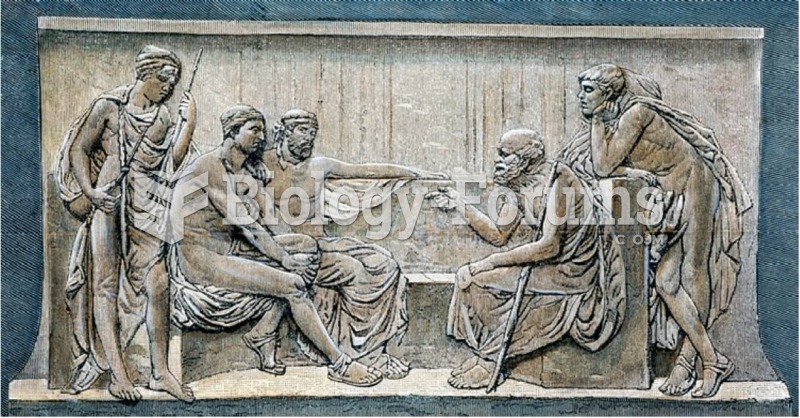

Socrates thrived on the intellectual life of the agora (the marketplace), where he could be sure to ...

Socrates thrived on the intellectual life of the agora (the marketplace), where he could be sure to ...

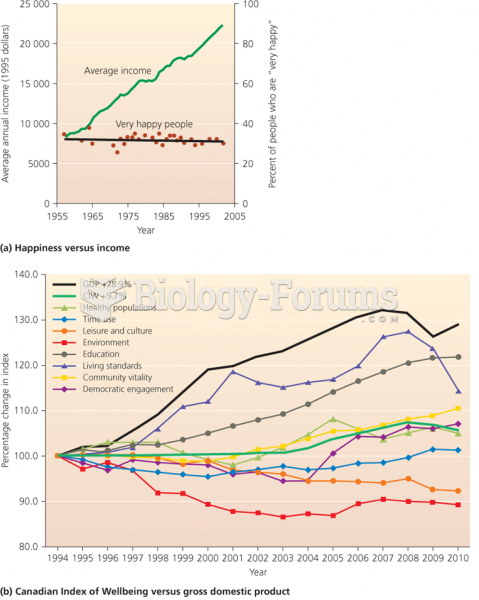

Growth and quality of life

Growth and quality of life