Answer to Question 1

Insurer's defenses

The court found that there was no misrepresentation. Even if there was misrepresentation, stated the court, it was not material. Plaintiff New England Mutual mistakenly likens the de-scription of a beneficiary to a warranty and argues that a mischaracterization of a beneficiary is grounds for rescission, similar to the misrepresentation of a pre-existing health condition. The court viewed the matter otherwise, reasoning that the relationship between the insured person and his or her beneficiary is considered to be a description and not a warranty. The instant case involves a description of a non-traditional, non-familiar relationship, not a warranty, which, even if misrepresented, would not invalidate the policy. The court did not stop there. It went on to say that the insurance company should have to pay attorneys' fees as well. The court noted that while attorneys' fees are rarely awarded in actions involving breach of contract, two exceptions exist which are applicable here. First, attorneys' fees can be awarded to insureds forced to defend against an insurer's action to escape coverage. Second, attorneys' fees may be awarded where there has been an unreasonable, bad faith denial of coverage. The court found that New England Mutual's actions evidenced a gross disregard for its policy obligation. Said the court, Upon learning that Duke had contracted AIDS and that there would, most likely be a claim asserted under the life insurance policy within a short period of time, plaintiff searched through its files in an effort to determine a way to escape its obligation. Such an investigation to find a bogus basis for disclaiming because the insured was a male homosexual (at higher risk for contracting AIDS than the general public) constitutes discrimination, both on the basis of disability and marital status.

Answer to Question 2

e

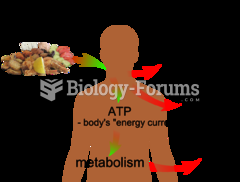

Basic overview of energy and human life.

Basic overview of energy and human life.

The Ku Klux Klan forces John Campbell, a black man, to beg for his life in Moore County, North Carol

The Ku Klux Klan forces John Campbell, a black man, to beg for his life in Moore County, North Carol

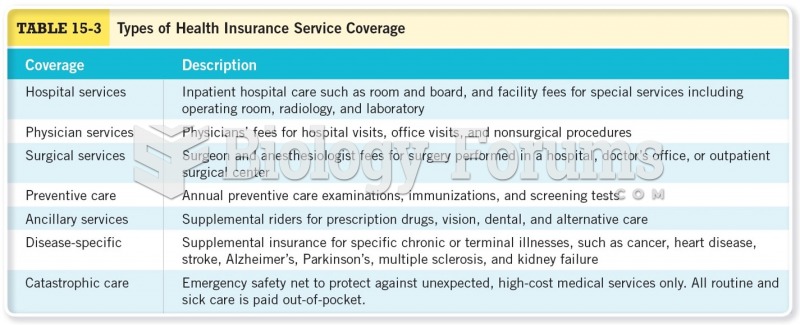

Types of Health Insurance Service Coverage

Types of Health Insurance Service Coverage

Still Life, House of The Stags (Cervi)

Still Life, House of The Stags (Cervi)

Life cycle of Pisum sativum

Life cycle of Pisum sativum

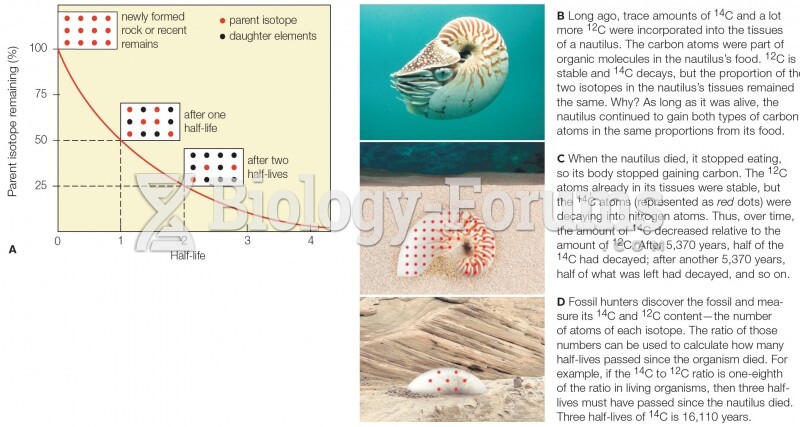

Half-life explained

Half-life explained