|

|

|

Large regions of the Boreal forest in Alberta have been divided into a grid due to industrial develo

Large regions of the Boreal forest in Alberta have been divided into a grid due to industrial develo

The "Emu in the sky," a constellation defined by dark clouds rather than the stars.

The "Emu in the sky," a constellation defined by dark clouds rather than the stars.

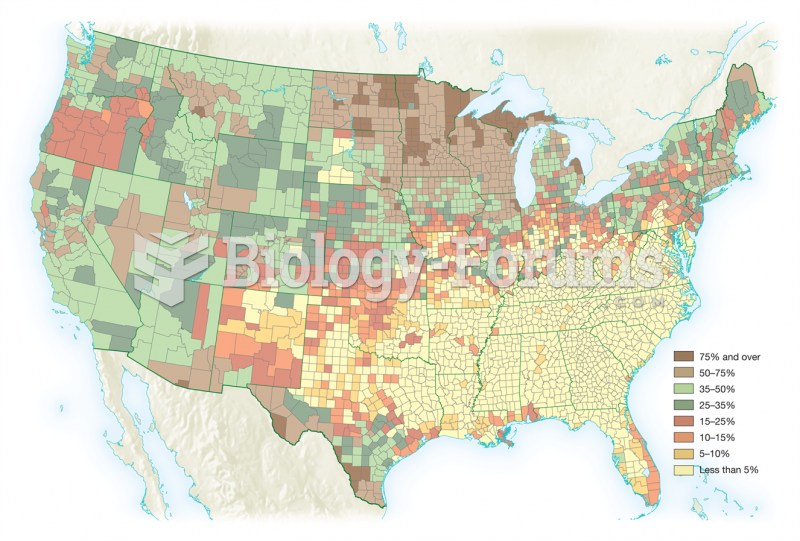

Percentage of Foreign-Born Whites and Native Whites of Foreign or Mixed Parentage in Total Populatio

Percentage of Foreign-Born Whites and Native Whites of Foreign or Mixed Parentage in Total Populatio

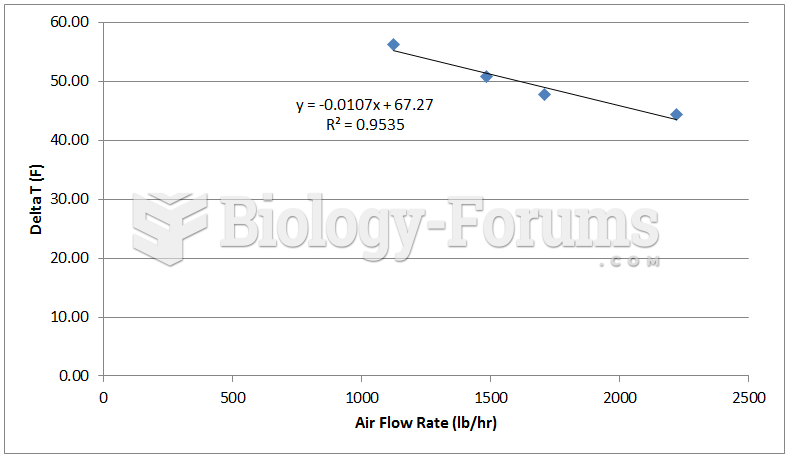

Change in air temperature at various air flow rates for a 4 pass operation

Change in air temperature at various air flow rates for a 4 pass operation

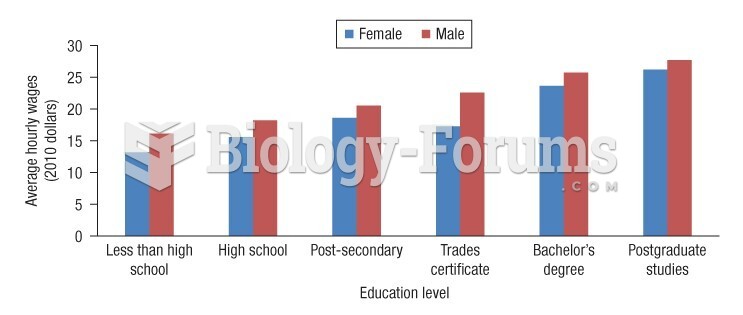

Average real hourly wages (2010 dollars) by education level, full-time workers aged 17 to 34 in 2011

Average real hourly wages (2010 dollars) by education level, full-time workers aged 17 to 34 in 2011

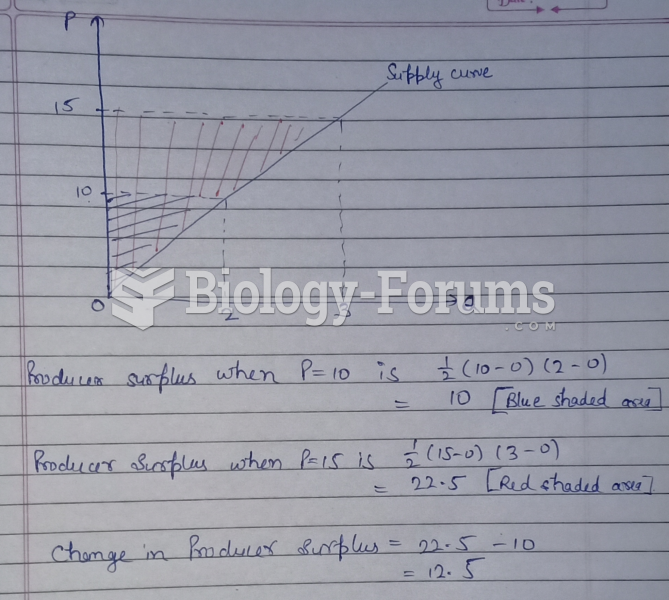

Suppose the market supply curve is p = 5Q. If price increases from 10 to 15, the change in ...

Suppose the market supply curve is p = 5Q. If price increases from 10 to 15, the change in ...