|

|

|

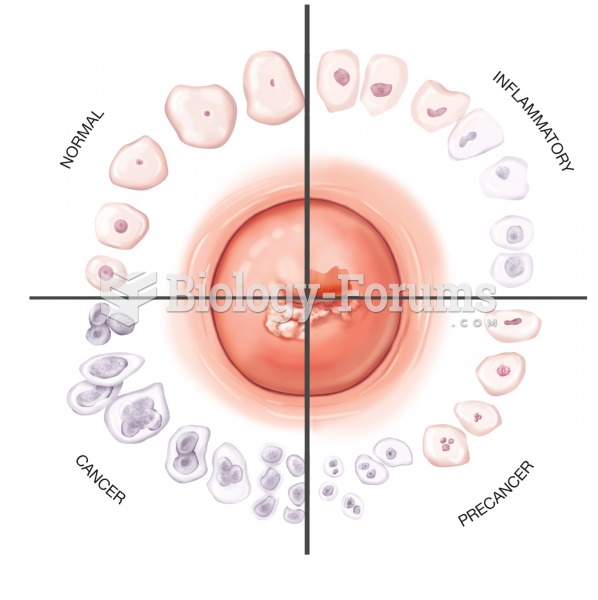

Pap smear. Cells of the cervix (shown in the center) change in appearance as they progress through

Pap smear. Cells of the cervix (shown in the center) change in appearance as they progress through

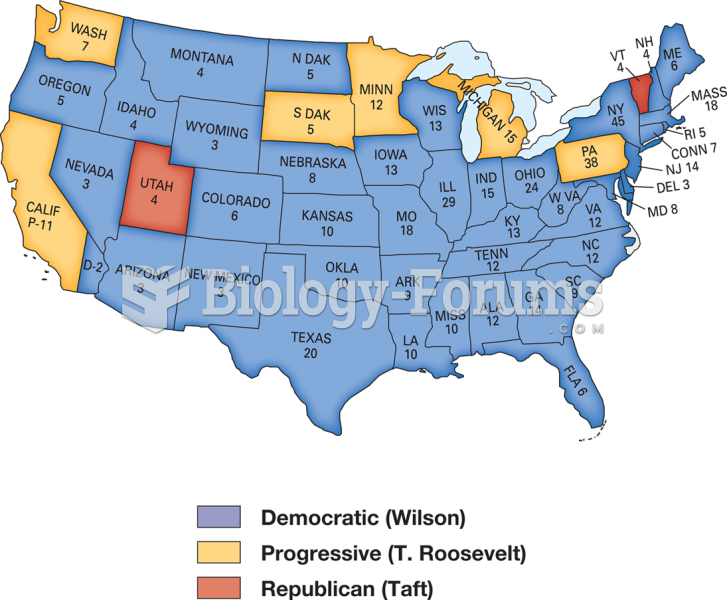

The Election of 1912: Divided Republicans, Democratic Victory

The Election of 1912: Divided Republicans, Democratic Victory

Family interactions change in response to the developing child, and parenting characteristics, such ...

Family interactions change in response to the developing child, and parenting characteristics, such ...

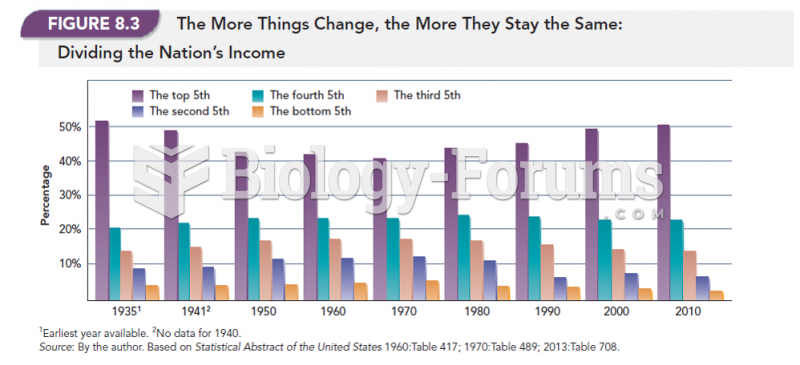

The More Things Change, The More They Say the Same: Dividing the Nation's Income

The More Things Change, The More They Say the Same: Dividing the Nation's Income

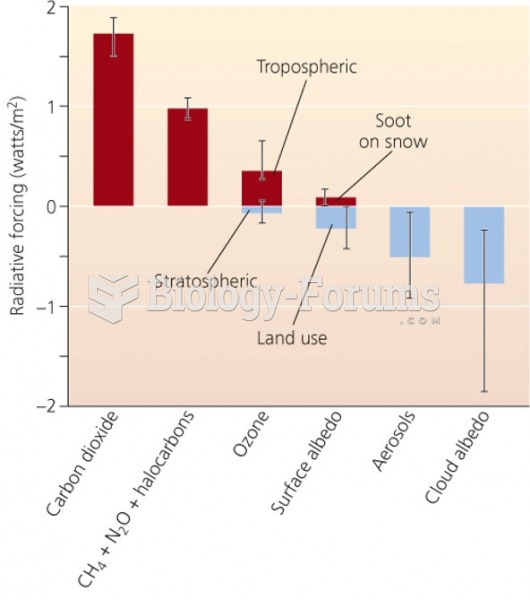

Radiative forcing expresses change in energy input over time

Radiative forcing expresses change in energy input over time

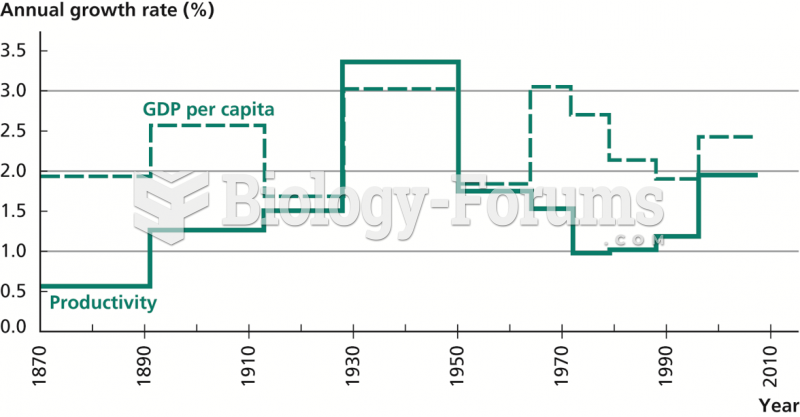

U.S. Output and Productivity Growth, 1870–2007

U.S. Output and Productivity Growth, 1870–2007