Answer to Question 1

1. Because no beginning inventories exist, the cost of the ending inventory must be the same as the cost of goods sold for the period. So, the unit cost of goods sold under variable costing is 7.15.

Variable cost of goods sold = Units sold Unit variable cost of goods sold

= 180,000 7.15

= 1,287,000

Variable nonmanufacturing expenses = 0

Sales Revenues = 2,250,000

Contribution Margin = 2,250,000 () 1,287,000 () 0

= 963,000

2. The profit under variable costing is given as 438,000. We just calculated the contribution margin of Iron City as 963,000. The difference, 525,000 (963,000 438,000) must represent the total fixed costs incurred by Iron City in 2014.

Fixed marketing and administrative costs are given as 295,000. The remainder, 230,000 (525,000 295,000) is therefore the fixed manufacturing costs for 2014.

3. The unit cost of ending inventory, as well as the unit cost of goods produced and sold, is 7.15 under variable costing and 8.30 under absorption costing. The difference, 1.15 (8.30 7.15) is the unit fixed manufacturing cost of goods produced during the period.

In requirement 2, we calculated that the total fixed manufacturing costs are 230,000.

So, Units produced = Total manufacturing costs/Unit fixed manufacturing cost of production

= 230,000/1.15

= 200,000 six-packs.

4. In 2014, Iron City incurred a total of 200,000 7.15 = 1,430,000 in variable manufacturing costs. This includes 880,000 in direct materials costs (given), 400,000 in direct manufacturing labor costs (given), and the rest in variable manufacturing overhead.

So, variable manufacturing overhead = 1,430,000 () 880,000 () 400,000

= 150,000.

5. Under variable costing, the proportion of variable manufacturing overhead corresponding to the units sold, relative to units produced, is expensed as variable cost of goods sold. This equals:

150,000 (180,000 units produced)/(200,000 units sold) = 135,000.

Moreover, the entire amount of fixed manufacturing overhead, totaling 230,000, is expensed.

So, total manufacturing overhead expensed = 135,000 (+) 230,000 = 365,000.

Answer to Question 2

c

iron

iron

Cao Fei, RMB City, in Art in the Twenty-First Century, season 5 episode, "Fantasy".

Cao Fei, RMB City, in Art in the Twenty-First Century, season 5 episode, "Fantasy".

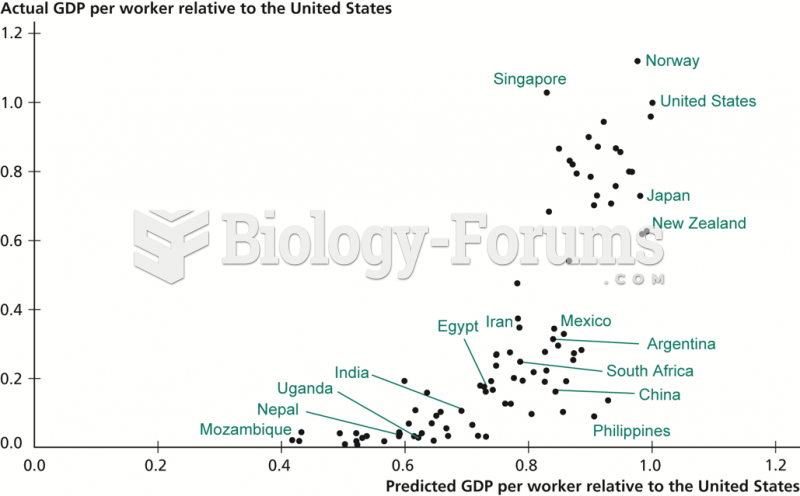

Predicted versus Actual GDP per Worker

Predicted versus Actual GDP per Worker

An organizational specialist is hired as a consultant to a company planning to open a coffee ...

An organizational specialist is hired as a consultant to a company planning to open a coffee ...

Business Math

Business Math

A company that makes cell phones has the following cost structure. They have fixed costs of ...

A company that makes cell phones has the following cost structure. They have fixed costs of ...