Answer to Question 1

The internal rate of return (IRR) attempts to answer the question, What rate of return does this project earn? For

computational purposes, the internal rate of return is defined as the discount rate that equates the present value of the

project's free cash flows with the project's initial cash outlay. It is referred to it as the internal rate of return because it

is dependent solely upon the project's cash flows, not on rates of return or the opportunity cost of money.

The modified internal rate of return (MIRR), has gained popularity as an alternative to the IRR method because it

avoids multiple IRRs and allows the decision maker to directly specify the appropriate reinvestment rate. As a result,

the MIRR provides the decision maker with the intuitive appeal of the IRR coupled with a reinvestment rate

assumption that prevents the possibility of multiple rates of return. Is the reinvestment rate assumption really a

problem? The answer is yes. One of the problems of the IRR is that it creates unrealistic expectations for both the

corporation and its shareholders.

There is more than one way to compute the MIRR, and each method can potentially result in a different value for the

MIRR. We used what we consider to be the most common way to compute the MIRR, which is also the one used by

Excel. Specifically, we discounted the project's negative cash flows back to the present using the project's required rate

of return and then compounded all the positive cash flows to the end of the project's life at the required rate of return

before computing the MIRR. Some analysts compute the MIRR by discounting negative cash flows back to the present

using the project's required rate of return and then computing the MIRR. Neither method is necessarily better than the

other.

Answer to Question 2

D

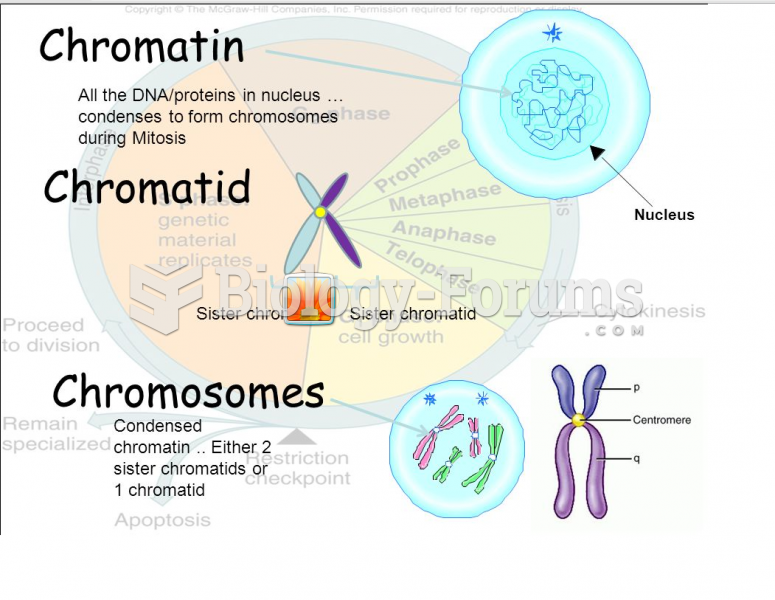

Difference between chromosomes, chromatids, and chromatins

Difference between chromosomes, chromatids, and chromatins

A typical open-end wrench. Note the size difference on each end and that the head is angled 15 ...

A typical open-end wrench. Note the size difference on each end and that the head is angled 15 ...

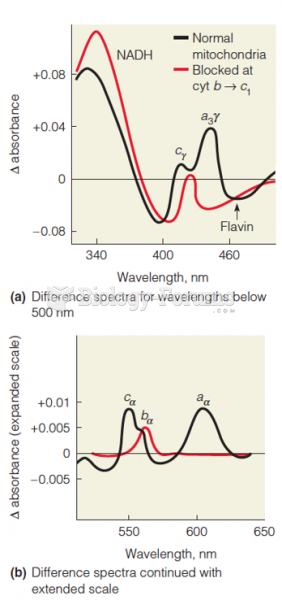

Difference spectra of mitochondria

Difference spectra of mitochondria

What's the Difference Between England, Great Britain, and United Kingdom?

What's the Difference Between England, Great Britain, and United Kingdom?

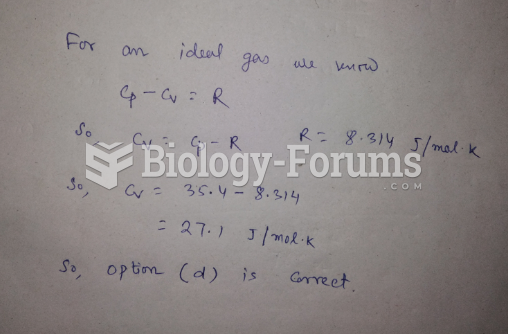

If CP for an ideal gas is 35.4 J/molK, which of the following is CV for this gas?

If CP for an ideal gas is 35.4 J/molK, which of the following is CV for this gas?

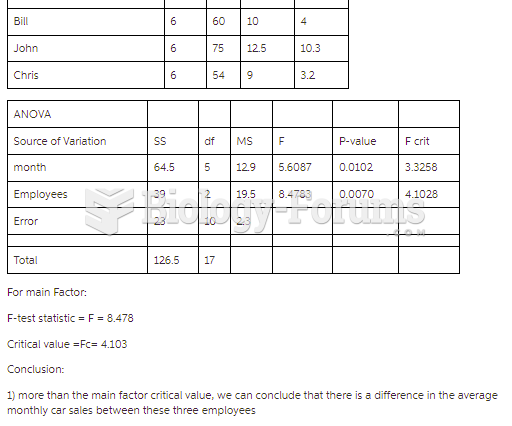

Sheridan Motors is a car dealership that would like to investigate if there is a difference in ...

Sheridan Motors is a car dealership that would like to investigate if there is a difference in ...