Answer to Question 1

Interpretation of insurance contract terms

The trial court construed Frances's death as an injury (rather than a loss from an injury) un-der the Nationwide insurance policy. The court noted that for payment, the policy required that an injury (1) arises solely from accident and (2) is not contributed to by sickness, disease, or bodily or mental infirmity. Because Allison conceded that the death was in part caused by a bodily infirmity (arteriosclerosis), the court held that the death was not covered by the policy and granted summary judgment in favor of Nationwide. The appellate court reasoned that because the injury was accidental, was not contributed to by disease or sickness, and occurred while the insured was riding as a passenger on an ocean liner, it constituted an injury under the policy. Frances's death was thus a loss resulting from injury, because the death occurred within 180 days of the injury, as required by the policy, and was a result of the injury (Frances would not have died but for the surgery). Consequently, the appellate court held that under the clear language of the policy the death benefit should have been paid.

Answer to Question 2

e

Alfred Hershey and Martha Chase

Alfred Hershey and Martha Chase

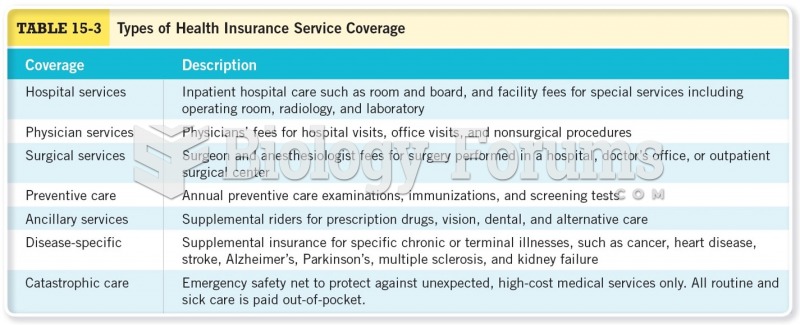

Types of Health Insurance Service Coverage

Types of Health Insurance Service Coverage

How to combine like-terms in expressions containing multi-brackets

How to combine like-terms in expressions containing multi-brackets

Children's Thinking (4e) By Martha W. Alibali

Children's Thinking (4e) By Martha W. Alibali

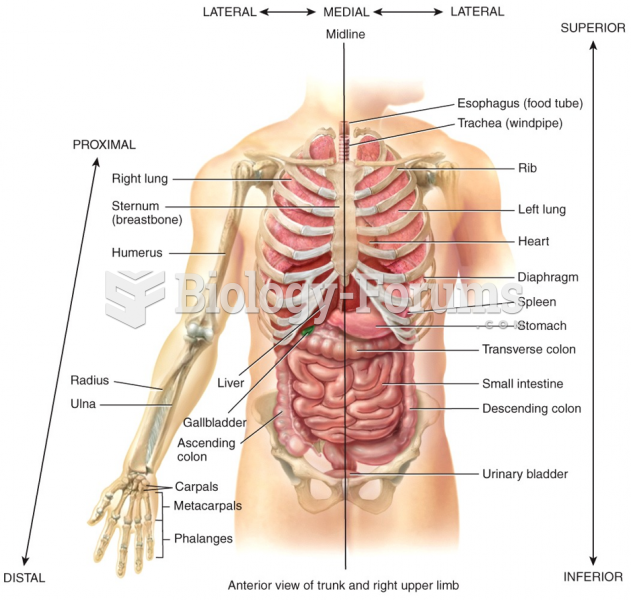

Directional Terms

Directional Terms

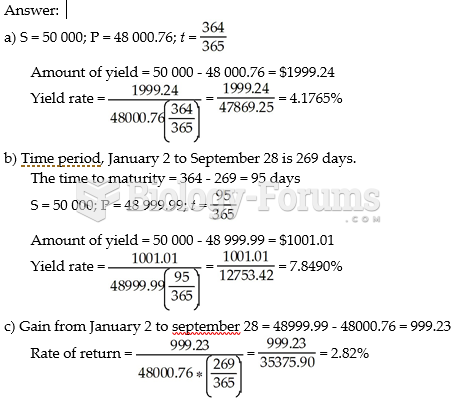

A government of Ontario 364-day T-bills with a face value of $50 000 were purchased on January ...

A government of Ontario 364-day T-bills with a face value of $50 000 were purchased on January ...