Answer to Question 1

a.

No dividend could be paid under this test, because the corporation does not have any earned surplus. A profit during only one quarter does not constitute an earned surplus. Earned surplus is defined as undistributed net profits, income, gains, and losses from the date of incorporation, i.e., retained earnings. This is the most restrictive of the various tests, but it is still followed by many states.

b.

It is not clear from the facts whether a dividend could be paid under this standard, but it probably could not. Surplus consists of the excess of net assets over stated capital. Surplus could consist of a capital surplus; it need not have been earned from the business of the corporation. Thus, this test is slightly more liberal than the earned surplus test. In all likelihood the corporation would be unable to meet this standard and would thus be unable to pay a dividend.

c. It is not clear from the facts whether a dividend could be paid under the net assets test, but as with the surplus test, it probably could not. Net assets consist of total assets minus total debts. The MBCA as amended in 1980 and the Revised Act have adopted this test. It permits dividends to be paid unless 1. if, after paying the dividend, the corporation would not be able to pay its debts as they become due in the usual course of business, or 2. the corporation's total assets after payment of the dividend would be less than the sum of its total liabilities plus the amount that would be needed, if the corporation were to be dissolved at the time of the dividend payment, to satisfy the preferential rights upon dissolution of shareholders whose preferential rights are superior to those receiving the dividend. Not enough information is given here to determine whether the test has been met, but the facts seem to imply that it has not.

Answer to Question 2

A

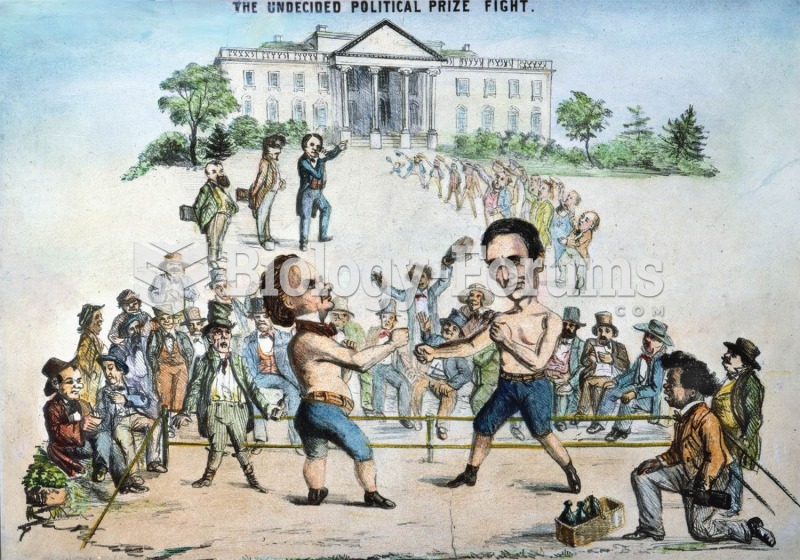

That politics was always a rough business is shown in this cartoon, which shows Lincoln, assisted by

That politics was always a rough business is shown in this cartoon, which shows Lincoln, assisted by

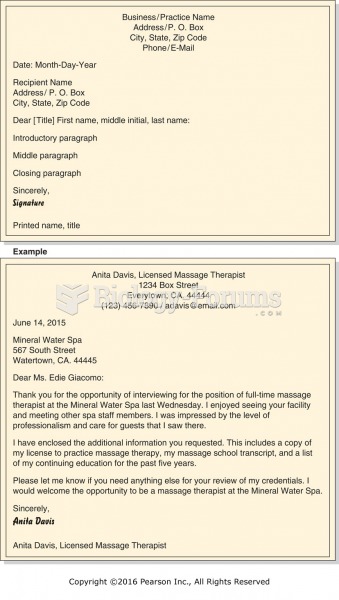

Business Letter Format and Example.

Business Letter Format and Example.

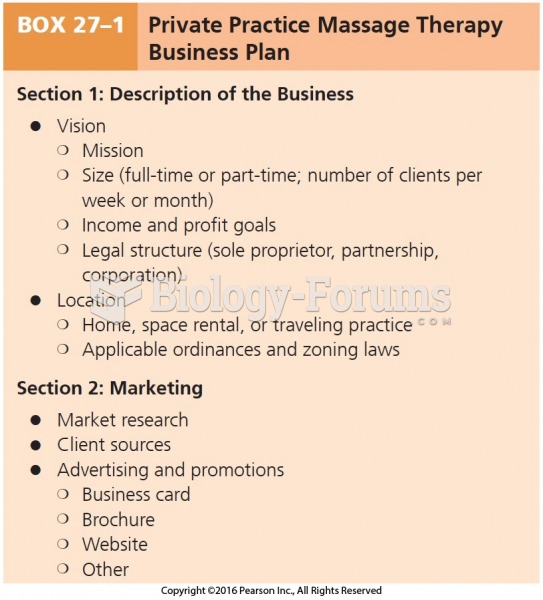

Private Practice Massage Therapy Business Plan

Private Practice Massage Therapy Business Plan

Business Analytics, 2nd Edition

Business Analytics, 2nd Edition

United States Health Care System: Combining Business, Health, and Delivery

United States Health Care System: Combining Business, Health, and Delivery

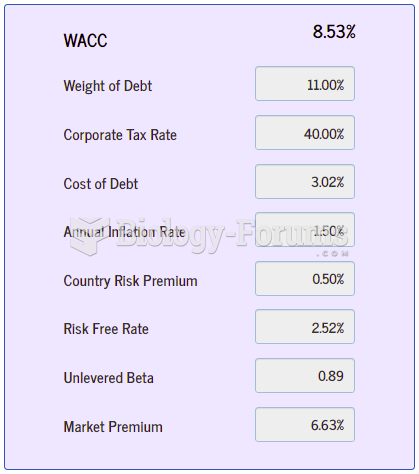

When operating your own business, it is wise to know your cost of capital and that of the ...

When operating your own business, it is wise to know your cost of capital and that of the ...