In a perfectly competitive industry, in the long-run equilibrium

A) the typical firm is producing at the output where its long-run average total cost is not minimized.

B) the typical firm is earning an accounting profit greater than its implicit costs.

C) the typical firm is maximizing its revenue.

D) the typical firm earns zero profit.

Question 2

Suppose that real GDP for 2015 was 10,000 billion and real GDP for 2016 was 11,000 billion. What is the rate of growth of real GDP between 2015 and 2016?

A) 1 B) 2 C) 5 D) 10

A 19-foot-long blue whale skull in the collections of the Smithsonian Museum of Natural History

A 19-foot-long blue whale skull in the collections of the Smithsonian Museum of Natural History

Feng Mengbo, Long March: Restart.

Feng Mengbo, Long March: Restart.

The air flowing into the engine can be directed through long or short runners for best performance ...

The air flowing into the engine can be directed through long or short runners for best performance ...

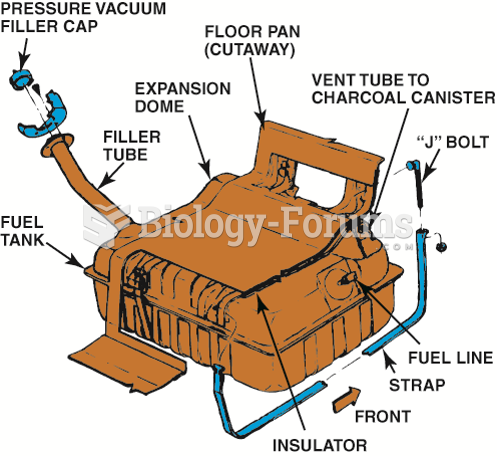

A typical fuel tank installation.

A typical fuel tank installation.

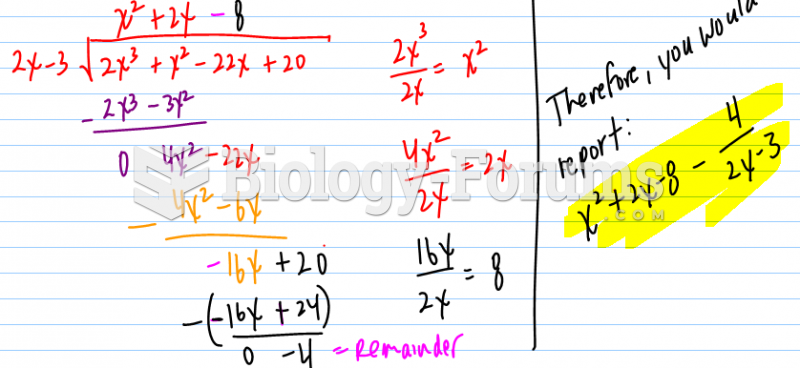

Long division for polynomials

Long division for polynomials

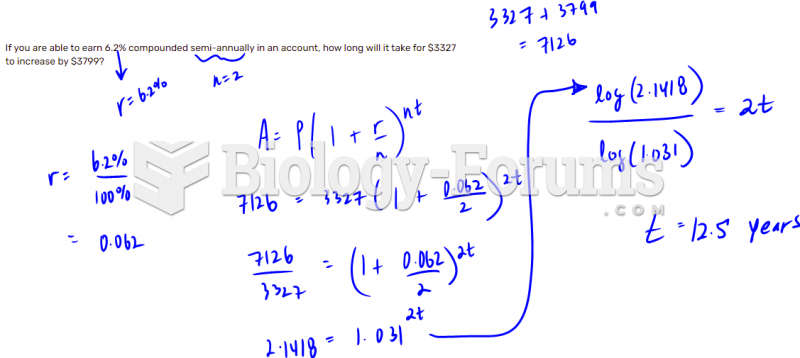

If you are able to earn 6.2% compounded semi-annually in an account, how long will it take for ...

If you are able to earn 6.2% compounded semi-annually in an account, how long will it take for ...