|

|

|

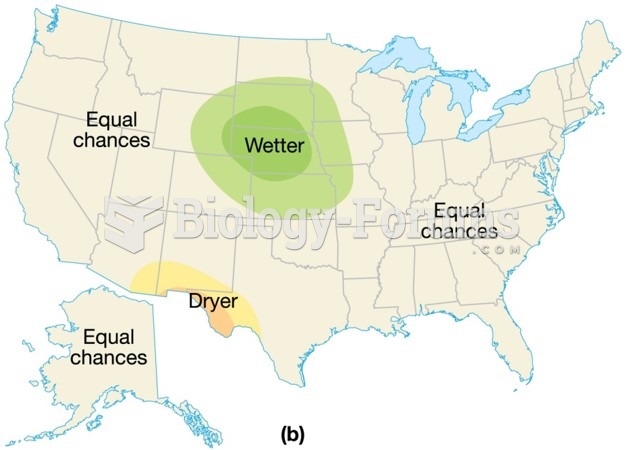

Long-range forecasts

Long-range forecasts

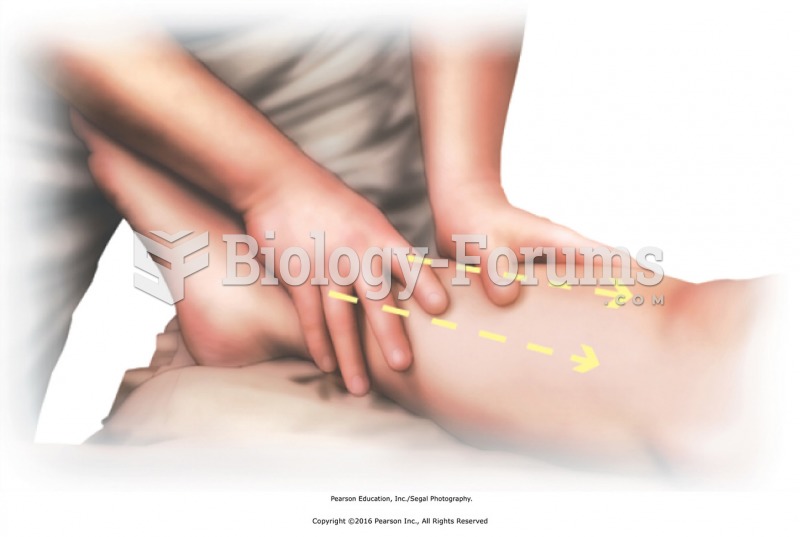

Clear the lower leg with long strokes. Start proximal to the ankle, and stroke to the knee and ...

Clear the lower leg with long strokes. Start proximal to the ankle, and stroke to the knee and ...

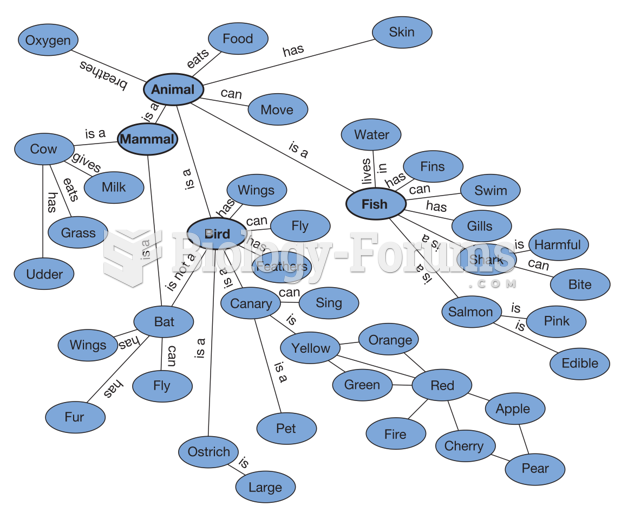

Part of a Semantic Network in Long-Term Memory

Part of a Semantic Network in Long-Term Memory

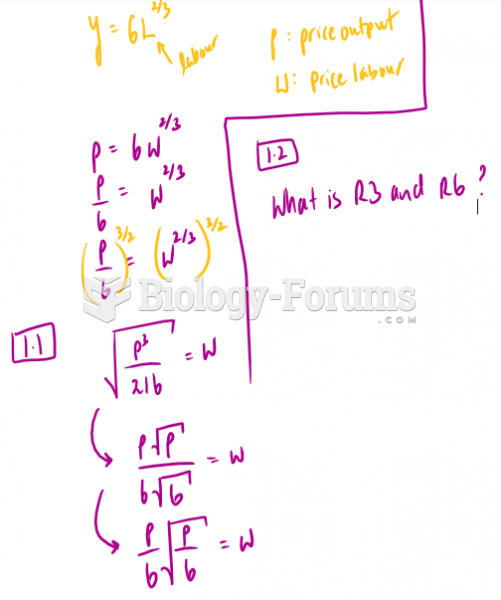

Find the factor demand for labour and the amount of output it will produce. Show all ...

Find the factor demand for labour and the amount of output it will produce. Show all ...

Summer squash exhibiting various fruit-shape phenotypes, including disc, long, and sphere

Summer squash exhibiting various fruit-shape phenotypes, including disc, long, and sphere

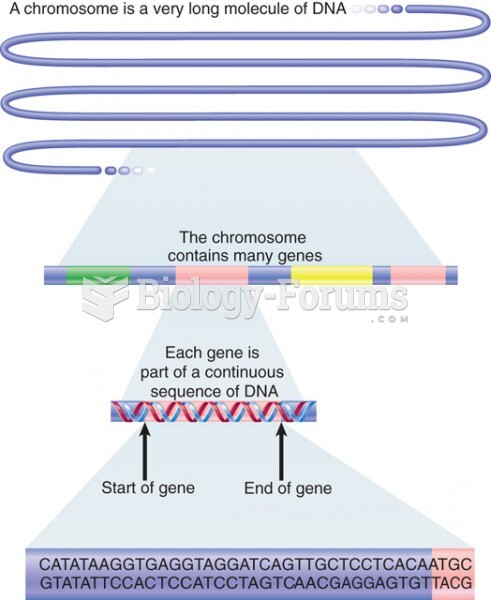

Each chromosome consists of a single, long molecule of DNA within which are the sequences of individ

Each chromosome consists of a single, long molecule of DNA within which are the sequences of individ