If in monopolistic competition in the short run, firms make ________ profits, then in the long run, new firms will enter the market. The ________ each individual firm's product will ________.

In the new long-run equilibrium firms will make ________ profit. A) economic; demand for; decrease; zero economic

B) normal; demand for; increase; zero economic

C) economic; supply of; decrease; an economic

D) economic; supply of; increase; zero economic

Question 2

Refining gasoline for our cars requires a very specialized resource, crude oil. As a result, the

A) demand for gasoline is price elastic.

B) demand for gasoline is price inelastic.

C) supply of gasoline is price elastic.

D) supply of gasoline is price inelastic.

Blue whale skeleton, outside the Long Marine Laboratory at the University of California, Santa Cruz

Blue whale skeleton, outside the Long Marine Laboratory at the University of California, Santa Cruz

Welcome sign for Kenton, Tennessee, an example of competition for "White Squirrel Capital"

Welcome sign for Kenton, Tennessee, an example of competition for "White Squirrel Capital"

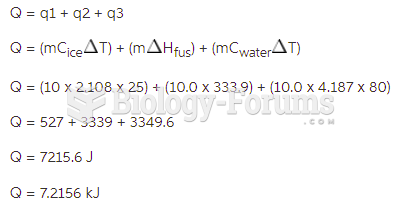

The enthalpy change for converting 10.0 g of ice at -25.0 C to water at 80.0 C is ________ kJ. ...

The enthalpy change for converting 10.0 g of ice at -25.0 C to water at 80.0 C is ________ kJ. ...

Perform the indicated division (long division polynomials)

Perform the indicated division (long division polynomials)

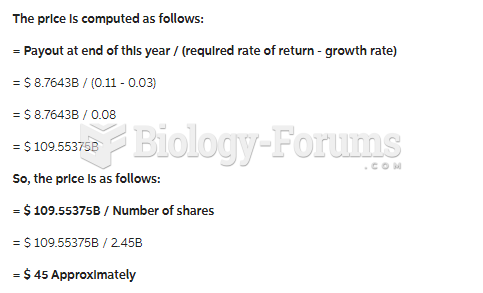

Analysts expect Virtucon to make payouts of $8.7643B at the end of this year. Assume that all ...

Analysts expect Virtucon to make payouts of $8.7643B at the end of this year. Assume that all ...

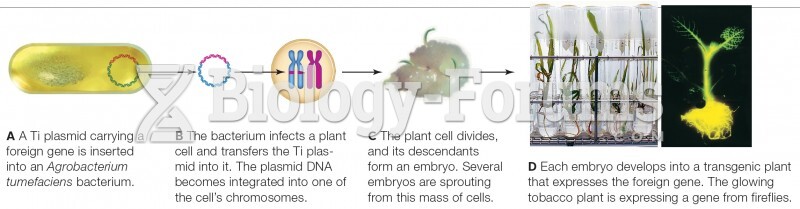

Using the Ti plasmid to make a transgenic plant

Using the Ti plasmid to make a transgenic plant