|

|

|

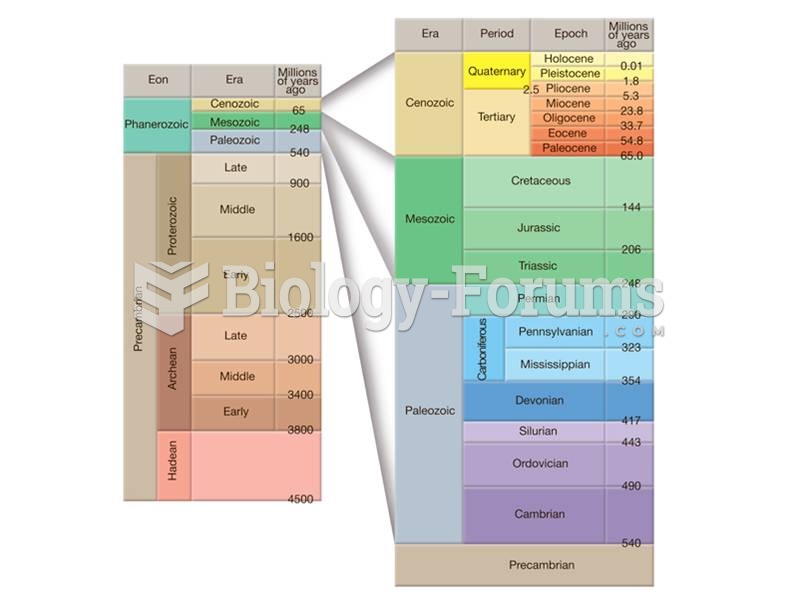

Earth’s history is divided into nested sets of time--eons, eras, periods, and epochs--and is called

Earth’s history is divided into nested sets of time--eons, eras, periods, and epochs--and is called

Greet a First-Time Client With a Firm Handshake.

Greet a First-Time Client With a Firm Handshake.

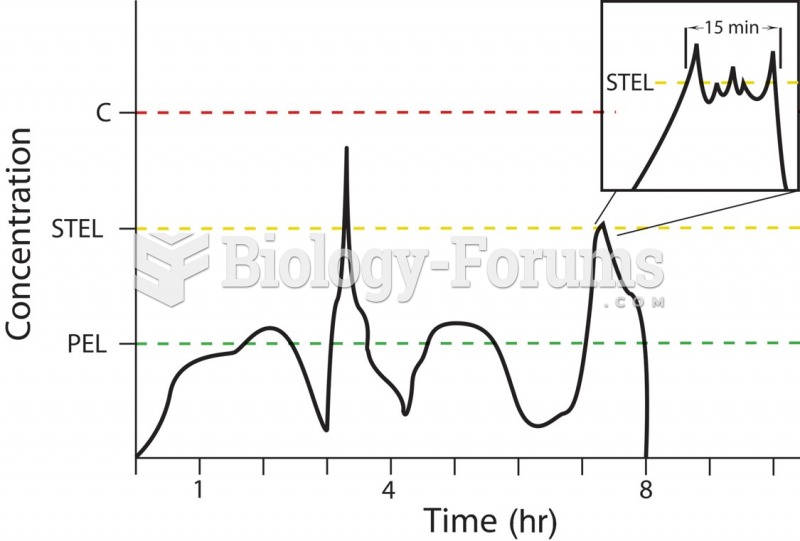

The relationship between the permissible exposure limit (PEL), the short-term exposure limit (STEL), ...

The relationship between the permissible exposure limit (PEL), the short-term exposure limit (STEL), ...

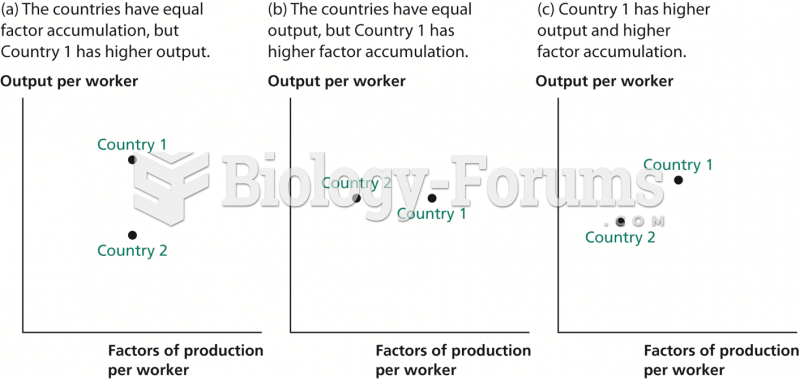

Inferring Productivity from Data on Output and Factor Accumulation

Inferring Productivity from Data on Output and Factor Accumulation

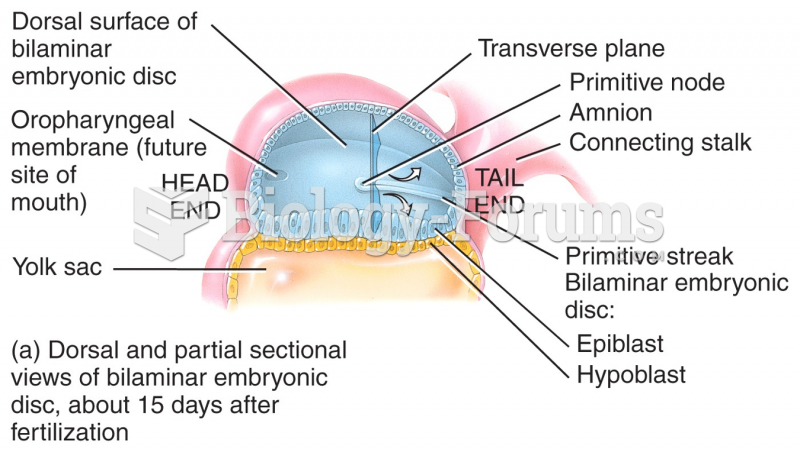

Embryonic Period

Embryonic Period