This topic contains a solution. Click here to go to the answer

|

|

|

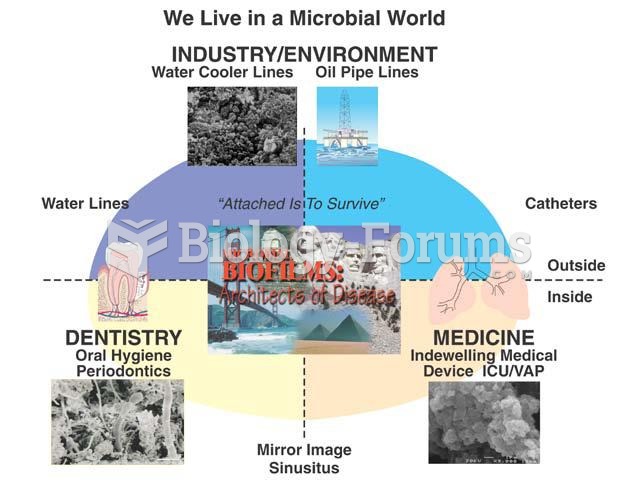

bio industry

bio industry

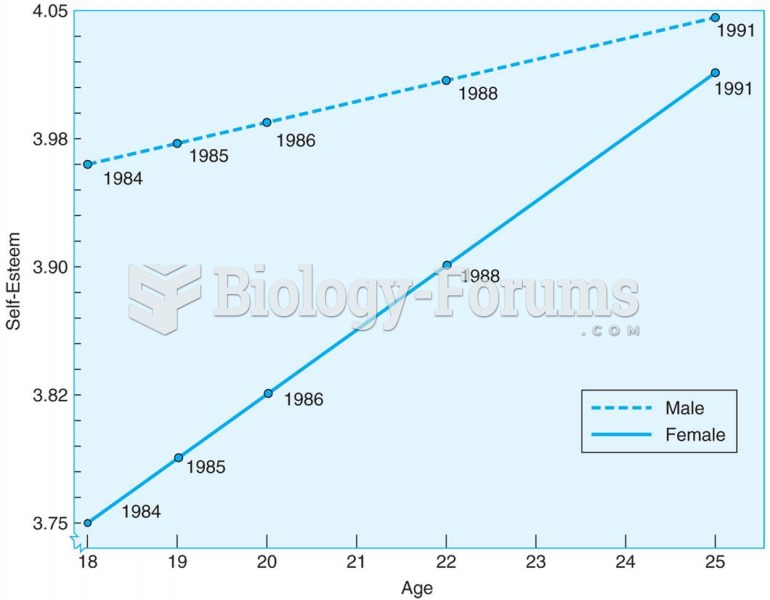

Young adults increase in self-esteem between the ages of 18 and 25, according to this longitudinal s

Young adults increase in self-esteem between the ages of 18 and 25, according to this longitudinal s

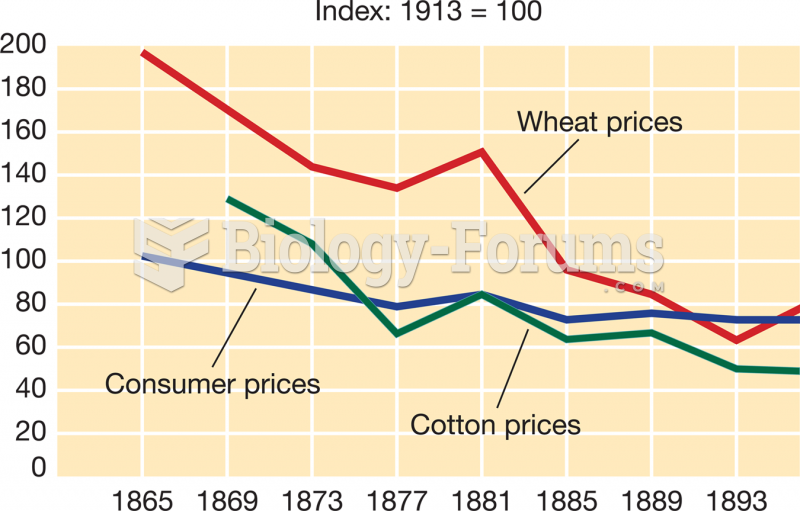

Wheat and Cotton Prices and Consumer Price Indexes, 1865–1896

Wheat and Cotton Prices and Consumer Price Indexes, 1865–1896

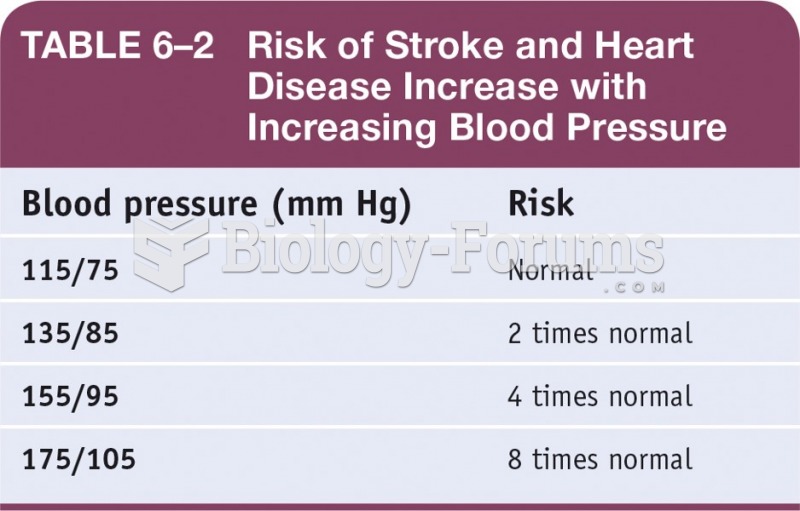

Risk of Stroke and Heart Disease Increase with Increasing Blood Pressure

Risk of Stroke and Heart Disease Increase with Increasing Blood Pressure

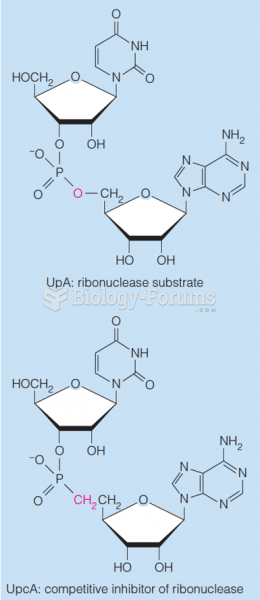

A substrate and its competitive inhibitor

A substrate and its competitive inhibitor

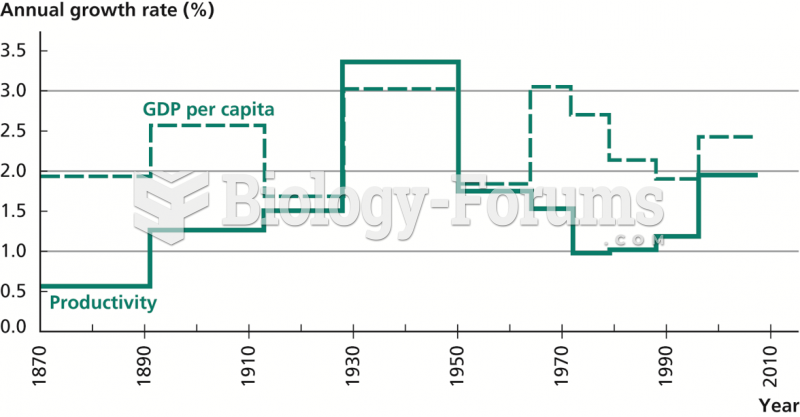

U.S. Output and Productivity Growth, 1870–2007

U.S. Output and Productivity Growth, 1870–2007