This topic contains a solution. Click here to go to the answer

|

|

|

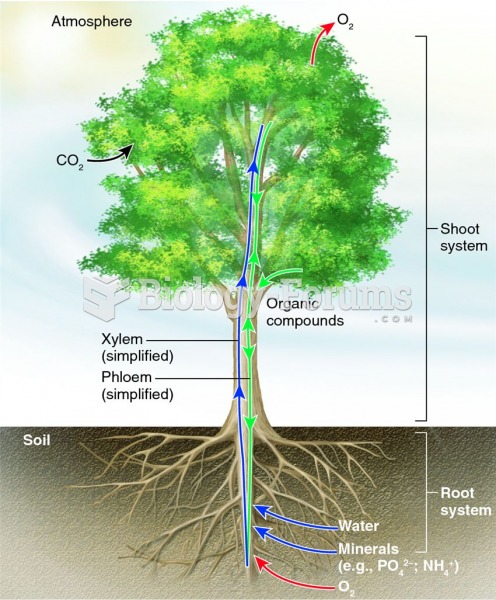

Overview of material uptake and long-distance transport processes in plants

Overview of material uptake and long-distance transport processes in plants

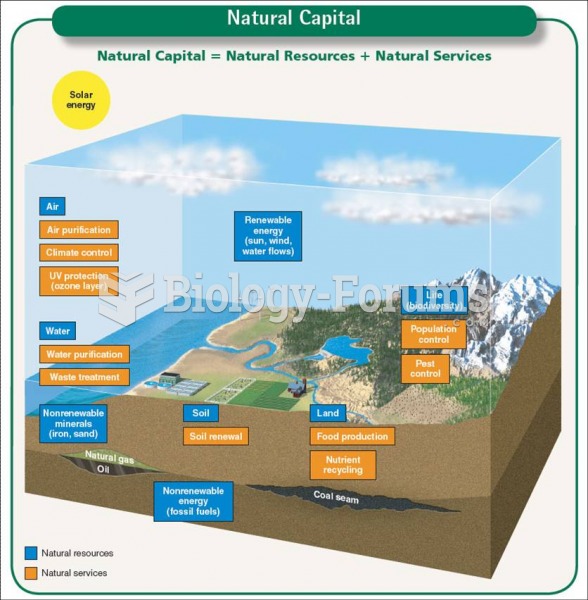

Natural Capital

Natural Capital

Long-tailed Widowbird

Long-tailed Widowbird

Nap master (fixed)

Nap master (fixed)

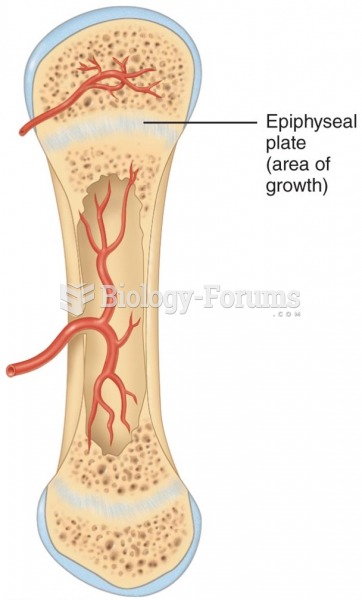

Epiphyseal Plate in Long Bone Adolescent bone growth takes place along the epiphyseal plate

Epiphyseal Plate in Long Bone Adolescent bone growth takes place along the epiphyseal plate

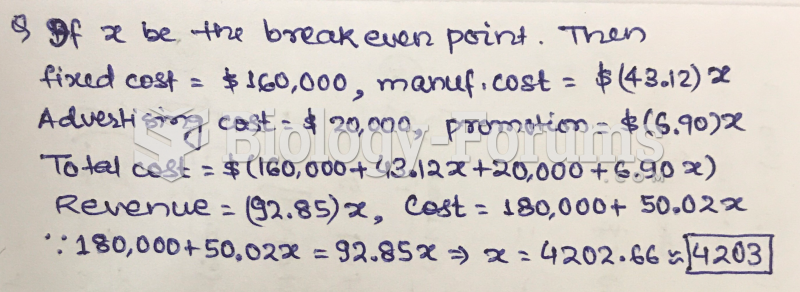

A company that makes cell phones has the following cost structure. They have fixed costs of ...

A company that makes cell phones has the following cost structure. They have fixed costs of ...