In the long run, in the model of monopolistic competition, for a typical firm, price is

a. above average cost but equal to marginal cost.

b. above marginal cost but equal to average cost.

c. above marginal cost.

d. equal to marginal cost and equal to or greater than average cost.

Question 2

In the monopolistic competition model

a. firms are price takers

b. barriers to entry maintain some monopoly rents in the long run.

c. one dominant firm acts as the monopolist that is followed by the fringe of competitors.

d. none of these.

Model Organism Neurospora

Model Organism Neurospora

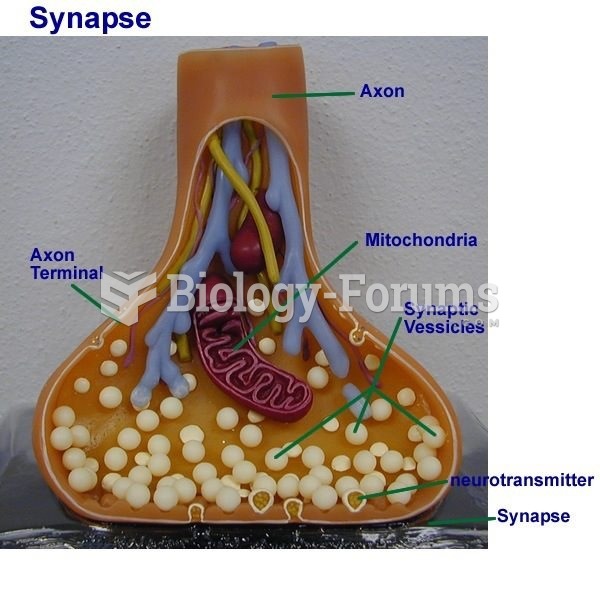

Axon terminal model

Axon terminal model

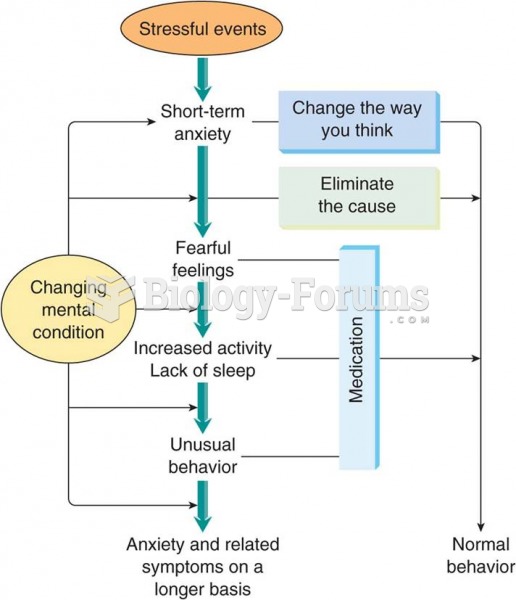

A model of anxiety in which stressful events or a changing mental condition can produce unfavorable

A model of anxiety in which stressful events or a changing mental condition can produce unfavorable

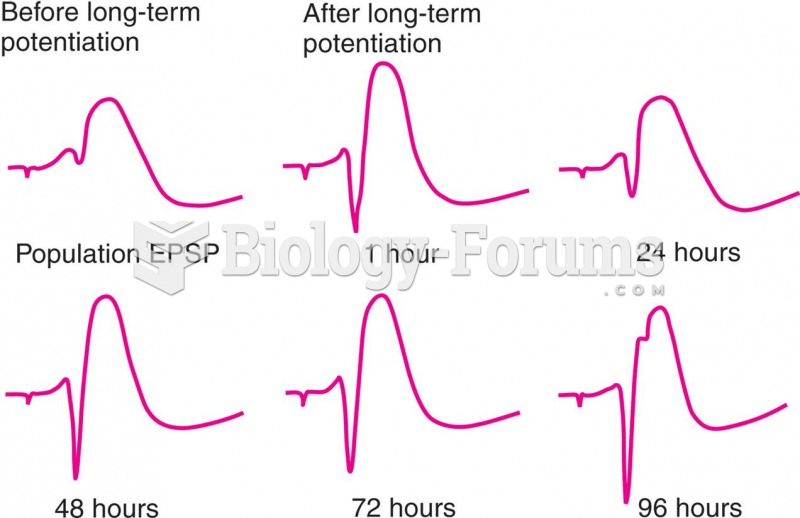

Long-Term Potentiation

Long-Term Potentiation

Alan Price - Poor People

Alan Price - Poor People

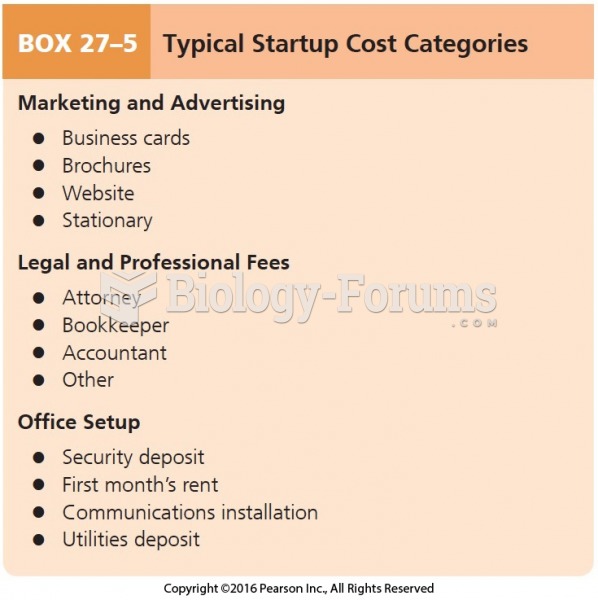

Typical Startup Cost Categories Cont.

Typical Startup Cost Categories Cont.