This topic contains a solution. Click here to go to the answer

|

|

|

How to solve first-degree equations (Part 1)

How to solve first-degree equations (Part 1)

How to convert verbal statements into algebraic equations (Part 2)

How to convert verbal statements into algebraic equations (Part 2)

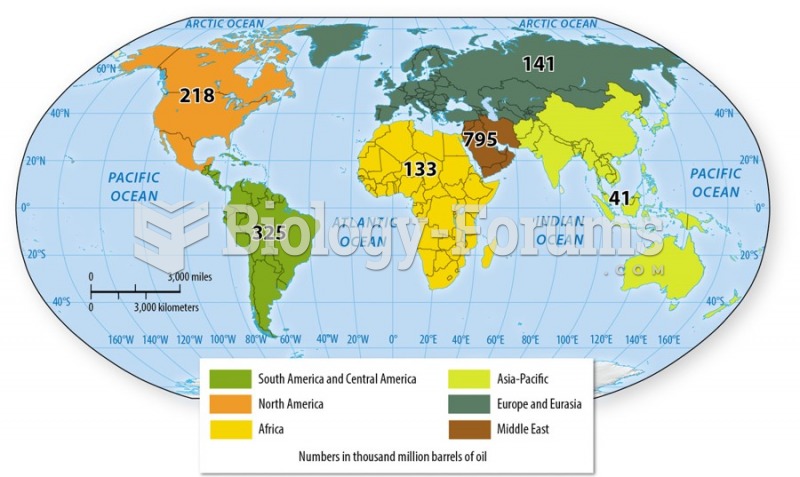

Growth in the demand for oil from the developing world

Growth in the demand for oil from the developing world

A variety of sugar substitutes is available to the consumer

A variety of sugar substitutes is available to the consumer

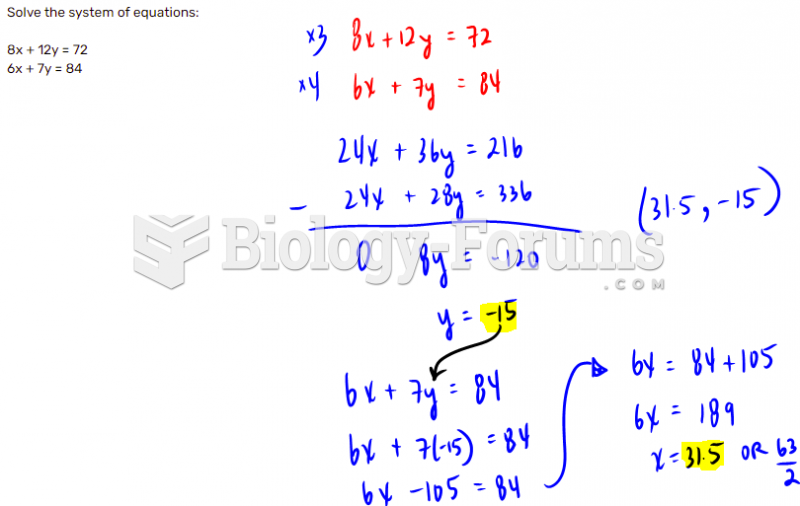

Solve the system of equations:

Solve the system of equations:

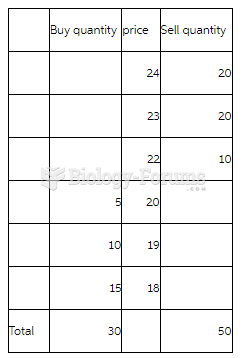

Markets and Institutions Market Story Problem

Markets and Institutions Market Story Problem