(Entries to prepare government-wide financial statements - revenue and expense accruals)

For the following situations, make adjusting entries necessary to prepare government-wide financial statements.

Where appropriate, take account of the amounts reported in the fund-level financial statements.

a. To prepare its government-wide financial statements for the year ended December 31,2012, the city reported a 900,000 long-term liability for estimated judgments and claims. At December 31, 2013, the city estimated that the long-term liability would be 935,000 . (Hint: Carry forward the starting liability and adjust for the increase.)

b. A city instituted a new sales tax starting January 1, 2012 . It collected 600,000 of sales taxes during 2012 . When the city prepared its fund-level statements, it accrued an additional 200,000 for sales taxes remitted by larger businesses in January, 2013, for taxes collected in the fourth quarter of 2012 . However, smaller businesses are not required to remit fourth quarter collections until April, 2013 . No accrual was made for those taxes, which were estimated to be 28,000 .

c. See facts in situation b. For the calendar year 2013, the city reported sales taxes of 800,000 in its fund-level financial statements. This amount includes all taxes collected in 2013 (applicable to 2013 and 2012), as well as the accrual for larger merchant remittances in January, 2014 . The accrual does not include estimated remittances of 35,000 from smaller merchants in April, 2014 .

Question 2

A(n) ___________________ ___________ happens when an attribute is dependent on a portion of the primary key not on the entire key.

Fill in the blank(s) with correct word

snout is just over 100 microns wide

snout is just over 100 microns wide

How to convert verbal statements into algebraic equations (Part 2)

How to convert verbal statements into algebraic equations (Part 2)

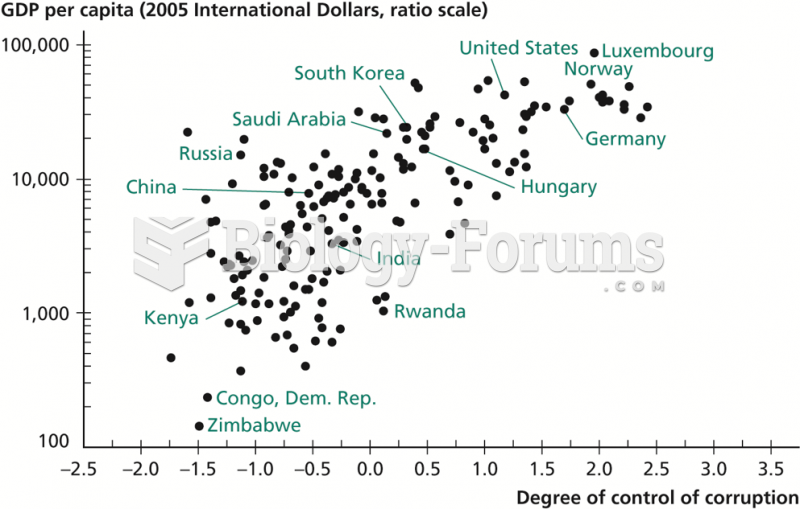

Government Corruption versus GDP per Capita, 2009

Government Corruption versus GDP per Capita, 2009

A wide variety of pathogens may live on or in the human body

A wide variety of pathogens may live on or in the human body

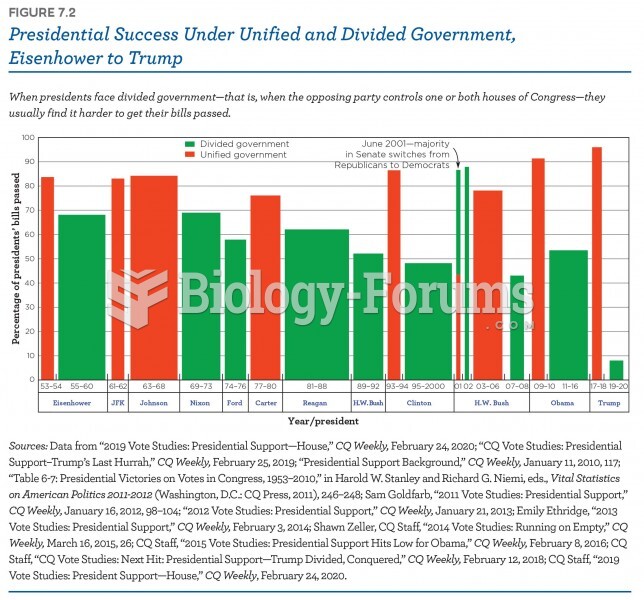

Presidential success under unified and divided government, from Eisenhower to trump

Presidential success under unified and divided government, from Eisenhower to trump

Financial Management 4th Edition (Cengage)

Financial Management 4th Edition (Cengage)