This topic contains a solution. Click here to go to the answer

|

|

|

USF Biologist Taegan McMahon conducts experiments on chlorothalonil at a research facility in East H

USF Biologist Taegan McMahon conducts experiments on chlorothalonil at a research facility in East H

This 80-year old man in a village in Hubei, China, has slowed down, but he has not retired. He is ...

This 80-year old man in a village in Hubei, China, has slowed down, but he has not retired. He is ...

Polio eradication campaign in Georgia in the 1950s. In the 1950s, 20,000 cases of polio occurred ...

Polio eradication campaign in Georgia in the 1950s. In the 1950s, 20,000 cases of polio occurred ...

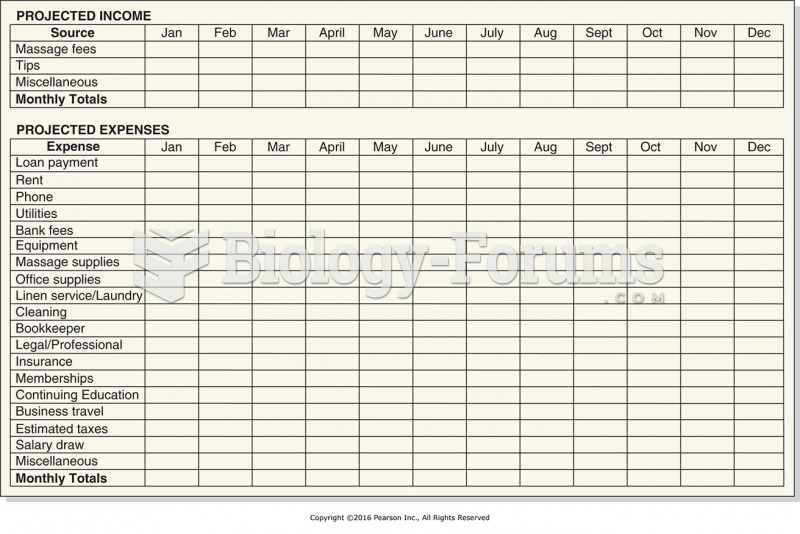

Sample budget spreadsheet form for first year of business.

Sample budget spreadsheet form for first year of business.

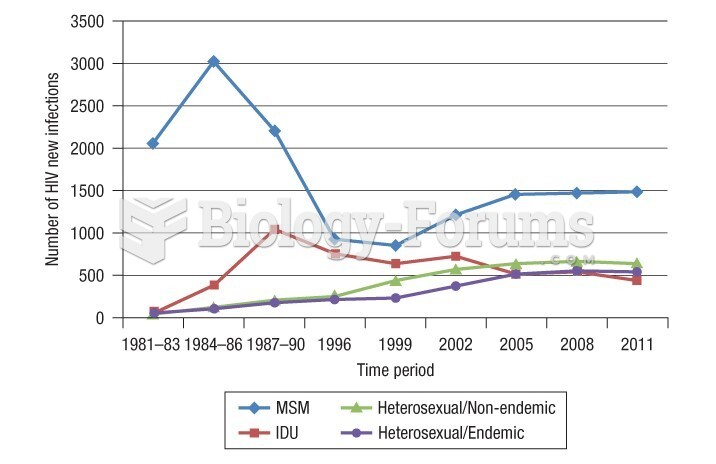

Estimated number of new HIV infections per year over time period in Canada

Estimated number of new HIV infections per year over time period in Canada

Walking into new year kids drawing

Walking into new year kids drawing