Answer to Question 1

Pro forma

Answer to Question 2

Method of proof can be defined as the means by which evidence is developed and presented to establish (or not) the requisite degree of belief or standard of proof, either a preponderance of the evidence or beyond a reasonable doubt. Methods of proof employed by forensic accountants can be direct, indirect, or a combination of the two.

A direct method of proof is a clear-cut or definite means of conclusively establishing a fact at issue such as a false expense or unreported income without inference or presumption. Direct methods of proof typically rely on documentary evidence such as tax returns, books and records, bank statements, invoices, cancelled checks, and contracts and the testimony of witnesses with firsthand knowledge such as bookkeepers, tax return preparers, employees, bankers, or real estate agents.

An indirect method of proof is not straightforward, but is instead built on circumstantial evidence. Circumstantial evidence is based on inference rather than personal knowledge or direct observation. Indirect methods of proof are founded on logic, common sense, critical thinking, and deductive reasoning. Indirect methods are most commonly employed in the absence of reliable books and records.

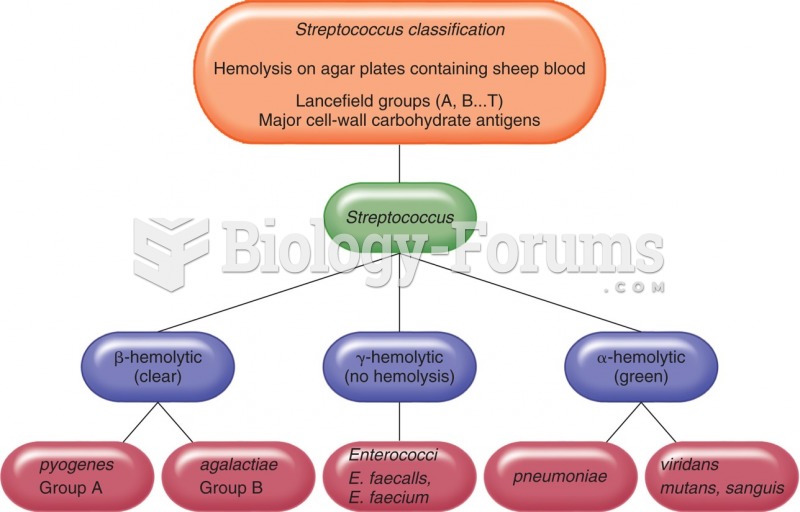

Basic classification of streptococci-based on hemolysis.

Basic classification of streptococci-based on hemolysis.

The science-based DRIs serve as the basis for information

The science-based DRIs serve as the basis for information

Nursing: A Concept-Based Approach to Learning, Volume I

Nursing: A Concept-Based Approach to Learning, Volume I

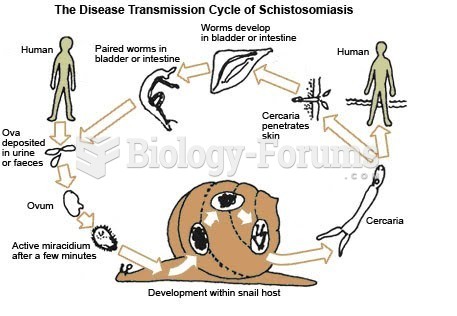

Water-based Diseases

Water-based Diseases

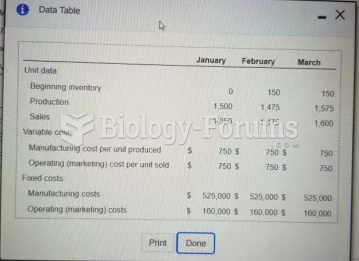

E9-23 Prepare income statements Explain the difference in operating income

E9-23 Prepare income statements Explain the difference in operating income

Financial Management 4th Edition (Cengage)

Financial Management 4th Edition (Cengage)