Answer to Question 1

1. In the following table, work backward from operating income to calculate the selling price.

Selling price 9.36 (plug)

Less: Variable cost per unit 4.00

Unit contribution margin 5.36

Number of units produced and sold 500,000 units

Contribution margin 2,680,000

Less: Fixed costs 2,500,000

Operating income 180,000

a) Total sales revenue = 9.36 500,000 units = 4,680,000

b) Selling price = 9.36 (from above)

Alternatively,

Operating income 180,000

Add fixed costs 2,500,000

Contribution margin 2,680,000

Add variable costs (4.0 500,000 units) 2,000,000

Sales revenue 4,680,000

c) Rate of return on investment =

d) Markup on full cost

Total cost = (4 500,000 units) + 2,500,000 = 4,500,000

Unit cost =

Markup =

Or

2. New fixed costs =2,500,000 225,000 = 2,275,000

New variable costs = 4.00 0.30 = 3.70

New total costs = (3.70 500,000 units) + 2,275,000 = 4,125,000

New total sales (4 markup) = 4,125,000 1.04 = 4,290,000

New selling price = 4,290,000 500,000 units = 8.58

Alternatively,

New unit cost = 4,125,000 500,000 units = 8.25

New selling price = 8.25 1.04 = 8.58

3. New units sold = 500,000 units 95 = 475,000 units

Budgeted Operating Income

for the Year Ending December 31, 20xx

Revenues (8.58 475,000 units)

4,075,500

Variable costs (3.70 475,000 units)

1,757,500

Contribution margin 2,318,000

Fixed costs 2,275,000

Operating income 43,000

4. The CEO has not considered customers in these pricing decisions. Will customers continue to want the product at these prices? What are competitors doing? The CEO should take a more market-based approach to pricing.

The CEO should also think about the effect of cost cutting on employee participation and morale and whether the cuts are falling disproportionately on any specific value-chain function.

Answer to Question 2

False

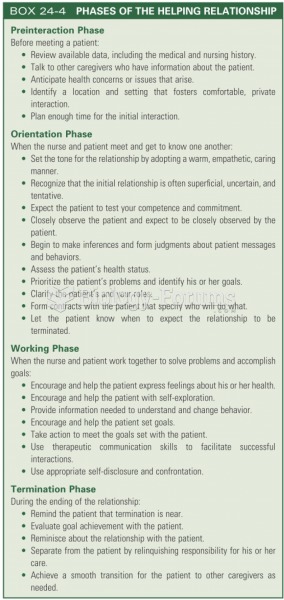

Phases of the working relationship

Phases of the working relationship

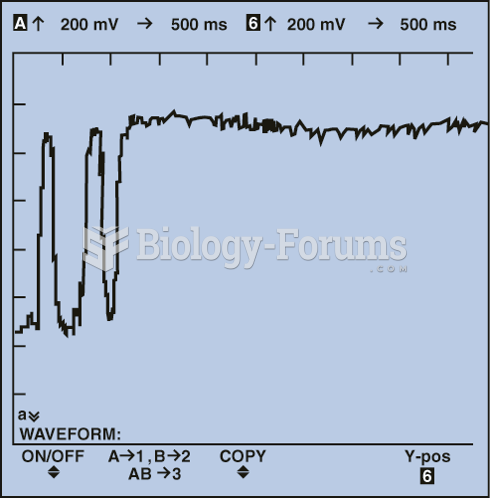

Adding propane to the air inlet of an engine operating in closed loop with a working oxygen sensor ...

Adding propane to the air inlet of an engine operating in closed loop with a working oxygen sensor ...

Red Bull uses strategies that help it target college-aged, young-adult consumers

Red Bull uses strategies that help it target college-aged, young-adult consumers

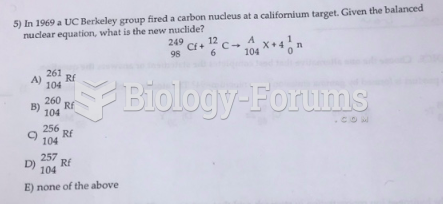

In 1969 a UC Berkeley group fired a carbon nucleus at a californium target. Give

In 1969 a UC Berkeley group fired a carbon nucleus at a californium target. Give

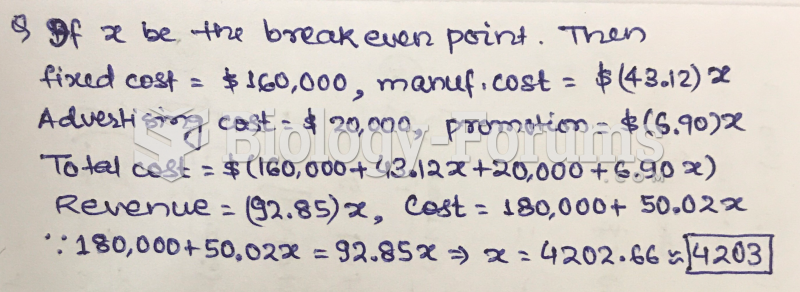

A company that makes cell phones has the following cost structure. They have fixed costs of ...

A company that makes cell phones has the following cost structure. They have fixed costs of ...

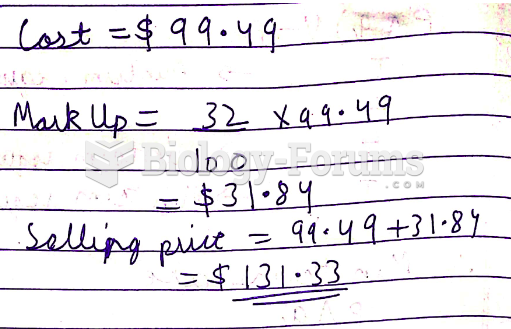

Cost = $99.49; Rate of markup based on cost = 32%. Find the markup and selling price.

Cost = $99.49; Rate of markup based on cost = 32%. Find the markup and selling price.