Answer to Question 1

b

Answer to Question 2

1. The classification of total costs in 2013 into value-added, nonvalue-added, or in the gray area in between follows:

Value Gray Nonvalue- Total

Added Area added (4) =

(1) (2) (3) (1)+(2)+(3)

Doing calculations and preparing drawings

77 390,000 300,300 300,300

Checking calculations and drawings

3 390,000 11,700 11,700

Correcting errors found in drawings

8 390,000 31,200 31,200

Making changes in response to client

requests 5 390,000 19,500 19,500

Correcting errors to meet government

building code, 7 390,000 27,300 27,300

Total professional labor costs 319,800 11,700 58,500 390,000

Administrative and support costs at 44

(171,600 390,000) of professional

labor costs 140,712 5,148 25,740 171,600

Travel 15,000 15,000

Total 475,512 16,848 84,240 576,600

Doing calculations and responding to client requests for changes are value-added costs because customers perceive these costs as necessary for the service of preparing architectural drawings. Costs incurred on correcting errors in drawings and making changes because they were inconsistent with building codes are nonvalue-added costs. Customers do not perceive these costs as necessary and would be unwilling to pay for them. Calvert should seek to eliminate these costs by making sure that all associates are well-informed regarding building code requirements and by training associates to improve the quality of their drawings. Checking calculations and drawings is in the gray area (some, but not all, checking may be needed). There is room for disagreement on these classifications. For example, checking calculations may be regarded as value added.

2. The consequences of classifying a non-value-added cost as a value-added cost is that managers may hesitate to reduce these costs thinking that if they eliminate these costs it would reduce the value or utility (usefulness) customers experience from using the product or service. But if these costs are really non-value-added costs, mangers should try to reduce these costs because these costs support activities that customers do not value.

For these reasons, managers who are unsure if a cost is value-added or nonvalue-added, often classify costs as nonvalue-added. The nonvalue-added classification focuses organization attention on reducing these costs. The risk with this approach is that an organization may cut some costs that are value-adding, leading to poor customer experiences. Distinguishing value-added from nonvalue-added costs is valuable but also requires the exercise of careful judgment.

3. Reduction in professional labor-hours by

a. Correcting errors in drawings (8 7,500) 600 hours

b. Correcting errors to conform to building code (7 7,500) 525 hours

Total 1,125 hours

Cost savings in professional labor costs (1,125 hours 52) 58,500

Cost savings in variable administrative and support

costs (44 58,500) 25,740

Total cost savings 84,240

Current operating income in 2013 124,650

Add cost savings from eliminating errors 84,240

Operating income in 2013 if errors eliminated 208,890

4. Currently 85 7,500 hours = 6,375 hours are billed to clients generating revenues of 701,250. The remaining 15 of professional labor-hours (15 7,500 = 1,125 hours) is lost in making corrections. Calvert bills clients at the rate of 701,250 6,375 = 110 per professional labor-hour. If the 1,125 professional labor-hours currently not being billed to clients were billed to clients, Calvert's revenues would increase by 1,125 hours 110 = 123,750 from 701,250 to 825,000 (701,250 + 123,750).

Costs remain unchanged

Professional labor costs 390,000

Administrative and support (44 390,000) 171,600

Travel 15,000

Total costs 576,600

Calvert's operating income would be

Revenues 825,000

Total costs 576,600

Operating income 248,400

Operating income would increase by 123,750 (248,400 124,650) or 99.3 (123,750 124,650). Eliminating 15 of nonvalue-added costs results in a doubling of operating income if the resources saved could be used to generate revenues. For this reason, organizations place great emphasis on reducing and eliminating nonvalue-added costs.

Some of the fastest growing religions in America are non-Judeo-Christian religions. This photograph

Some of the fastest growing religions in America are non-Judeo-Christian religions. This photograph

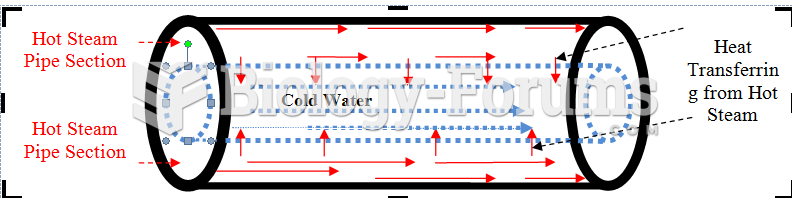

Concentric double-pipe heat exchanger for co-current flow

Concentric double-pipe heat exchanger for co-current flow

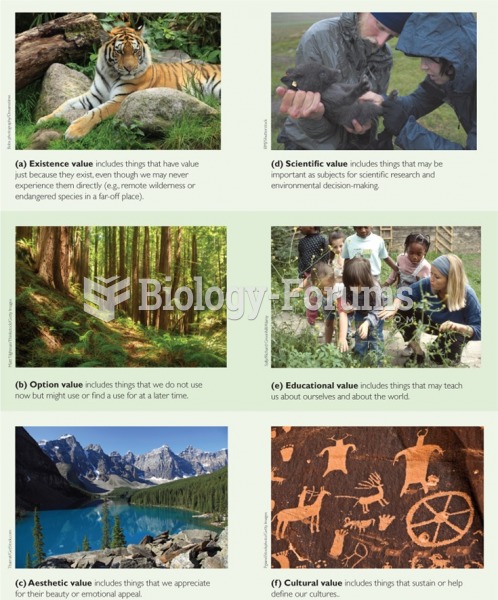

Ecosystem goods and services and monetary values

Ecosystem goods and services and monetary values

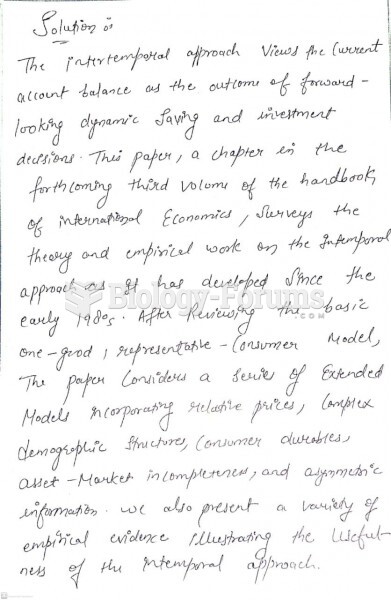

Explain how it can be desirable from an intertemporal perspective for a country run a current ...

Explain how it can be desirable from an intertemporal perspective for a country run a current ...

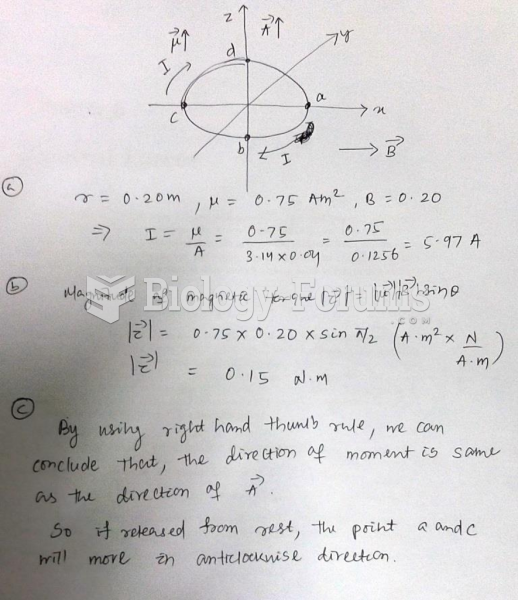

A rigid circular loop has a radius of 0.20 m and is in the xy-plane. A clockwise current I is ...

A rigid circular loop has a radius of 0.20 m and is in the xy-plane. A clockwise current I is ...

The diagonal of the floor of a rectangular office cubicle is 2 ft longer than the ...

The diagonal of the floor of a rectangular office cubicle is 2 ft longer than the ...