Answer to Question 1

T

Answer to Question 2

1.

Direct Manuf. Labor Support Order Processing Design Support Other Total

Wages and salaries 192,000 120,000 144,000 24,000 480,000

Depreciation 15,000 6,000 9,000 30,000 60,000

Rent 36,000 30,000 12,000 42,000 120,000

Other overhead 48,000 72,000 84,000 36,000 240,000

Total 291,000 228,000 249,000 132,000 900,000

Cost Allocation Base Allocation Rate

Direct Manuf. Labor Support 291,000 30,000 DMLHs 9.70/DMLH

Order Processing 228,000 500 orders 456/order

Design Support

Other 249,000

132,000 100 custom designs

30,000 DMLHs 2,490/custom design

4.40/DMLH

2.

Direct materials 4,550

Direct manuf. labor (80 hrs. 20/hr.) 1,600

Direct manuf. labor support (80 dir. manuf. lbr-hrs. 9.70/hr.) 776

Order processing (1 order 456/order) 456

Design support (1 custom design 2,490/custom design)

Other overhead (80 dir. manuf. lbr-hrs. 4.40/hr.) 2,490

352

Total overhead costs 10,224

3. Because only about 20 of the orders that Thurgood receives require custom designs, it is important that the costs generated by custom designs are not allocated to non-custom orders. Activity-based costing allows Thurgood to only assign resources used by orders to the orders. Similarly, order processing costs of 456/order are assigned to each order, regardless of the size of the order. Activity-based costing leads to more accurate costing of orders. This, in turn, leads to more competitive pricing. If Thurgood allocated all overhead costs to orders on the basis of direct manufacturing labor hours, they would tend to overprice larger, non-custom orders and underprice smaller, custom orders. They would likely lose bids on the overpriced orders and win the underpriced orders, but then lose money on the bids they won because the actual costs would be much greater than the estimated costs. The underpriced bids have small direct manufacturing labor hours relative to the resources needed to support custom designs and order processing costs for small orders.

Literacy and Gender Equity

Literacy and Gender Equity

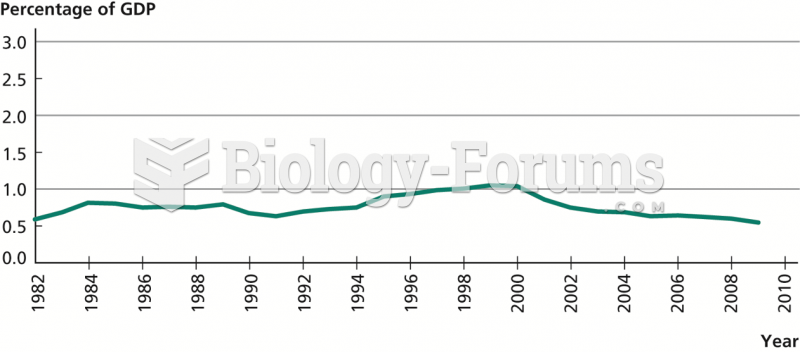

Investment in Computers as a Percentage of GDP, 1982–2009

Investment in Computers as a Percentage of GDP, 1982–2009

Business Intelligence, Analytics, and Data Science: A Managerial Perspective, 4th Edition

Business Intelligence, Analytics, and Data Science: A Managerial Perspective, 4th Edition

business solution

business solution

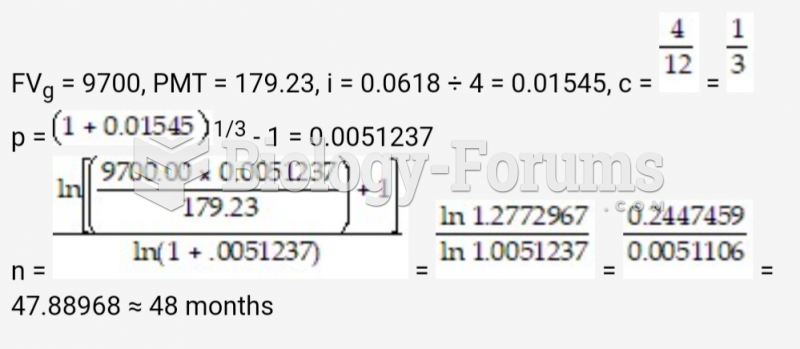

Business Math Question

Business Math Question

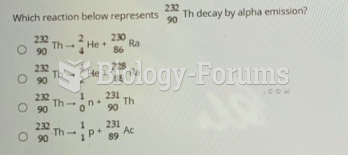

Which reaction below represents Th decay by alpha emission?

Which reaction below represents Th decay by alpha emission?