This topic contains a solution. Click here to go to the answer

|

|

|

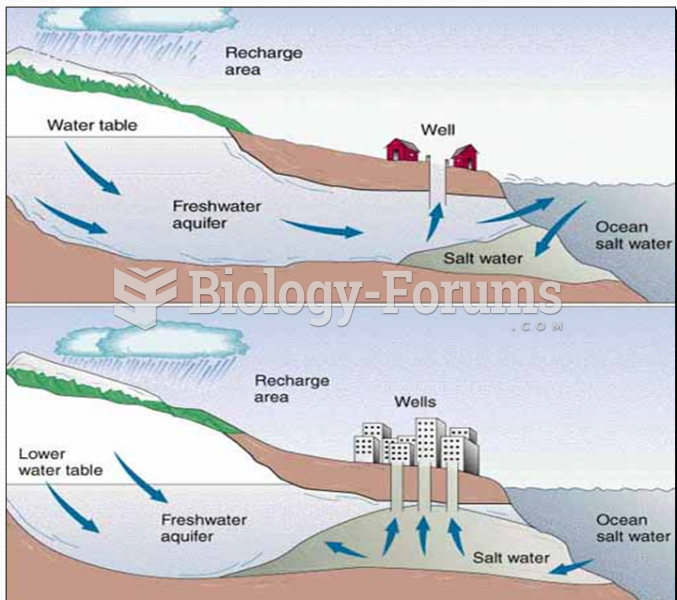

Example of coastal cities Recharge Rates

Example of coastal cities Recharge Rates

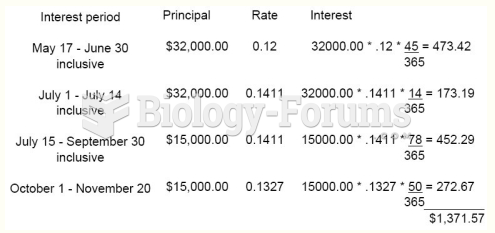

Accounting

Accounting

An organizational specialist is hired as a consultant to a company planning to open a coffee ...

An organizational specialist is hired as a consultant to a company planning to open a coffee ...

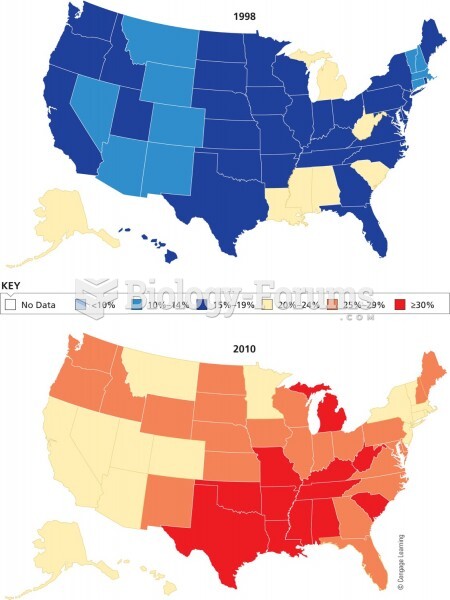

Fraction of obese individuals by state in 1998 and 2008. In 1998, 42 states had obesity rates below

Fraction of obese individuals by state in 1998 and 2008. In 1998, 42 states had obesity rates below

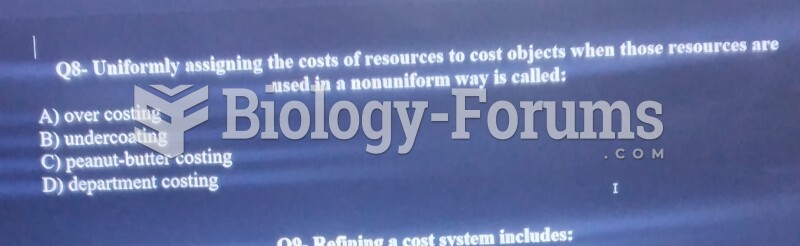

question in cost accounting

question in cost accounting

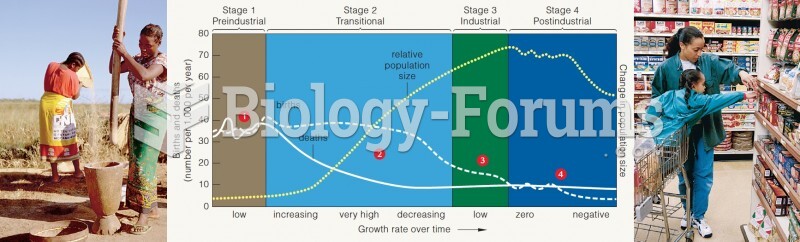

Demographic transition model for changes in population growth rates and sizes, correlated with long-

Demographic transition model for changes in population growth rates and sizes, correlated with long-