This topic contains a solution. Click here to go to the answer

|

|

|

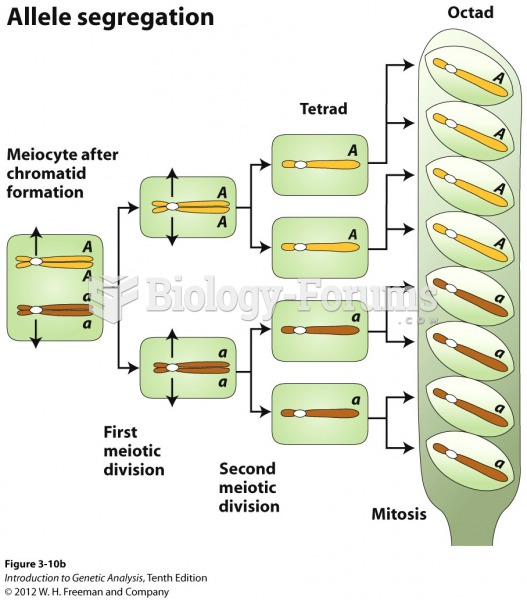

The linear meiosis of Neurospora

The linear meiosis of Neurospora

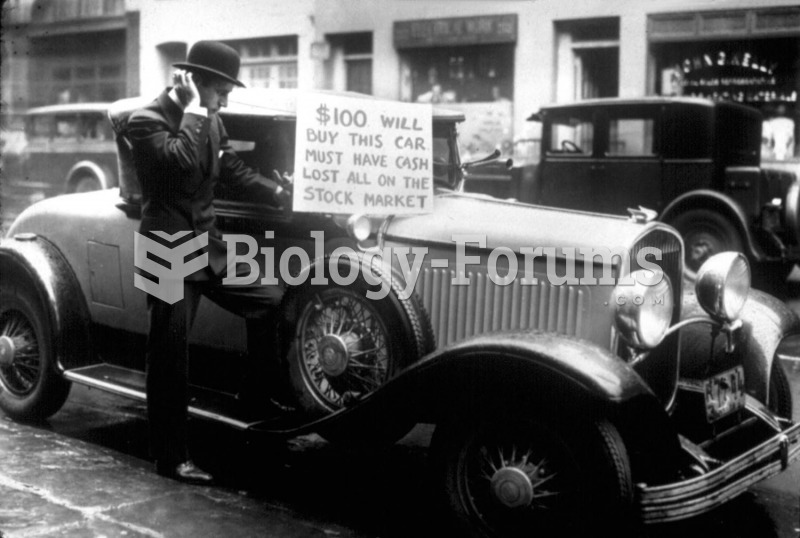

Walter Thompson saw his assets evaporate during the stock market collapse in 1929. Desperate for ...

Walter Thompson saw his assets evaporate during the stock market collapse in 1929. Desperate for ...

How to solve any rational equation by factoring (Part 1)

How to solve any rational equation by factoring (Part 1)

How to sketch a quadratic equation that is in standard form (Question 2)

How to sketch a quadratic equation that is in standard form (Question 2)

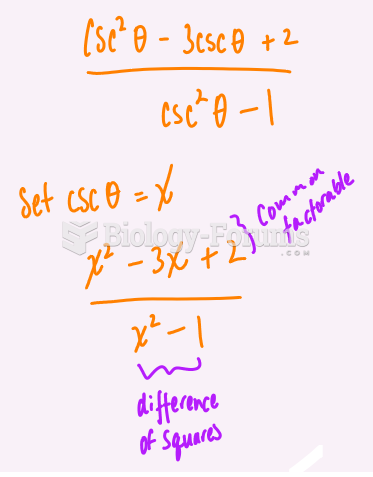

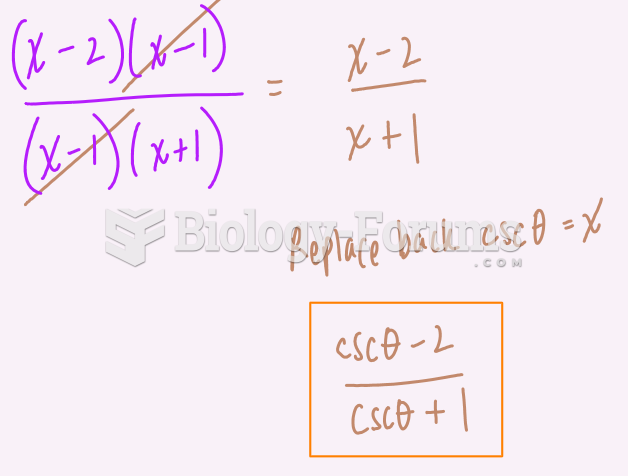

Simplify Trig Equation

Simplify Trig Equation

Simplify Trig Equation

Simplify Trig Equation