The appropriate measure for risk according to the capital asset pricing model is

A) the standard deviation of a firm's stock returns.

B) the standard deviation of a firm's cash flows.

C) alpha.

D) beta.

Question 2

Given a discount rate of 0, which of the following has the greatest present value? ONE, a series of 10 equal annual end-of-the cash flows of 100 each, TWO, just like ONE except the first 5 cash flows are only 50 but the last 5 cash flows are 150

, or THREE, just like ONE except the 10 100 cash flows are at the beginning of the period.

A) ONE

B) TWO

C) THREE

D) The choices all have equal present values.

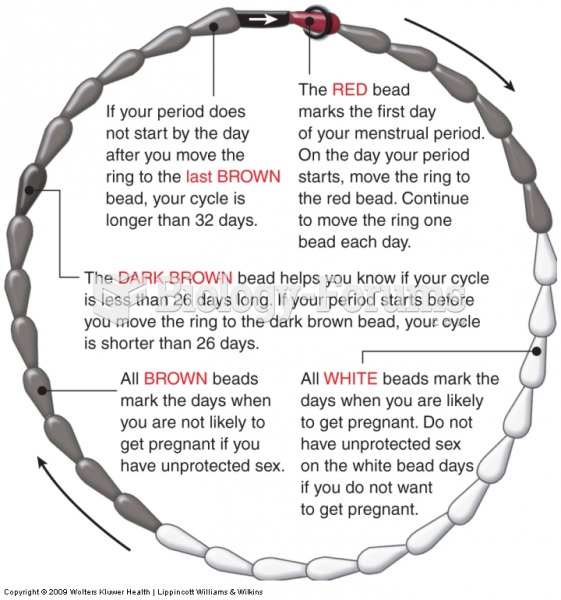

CycleBeads help women use the Standard Days Method.

CycleBeads help women use the Standard Days Method.

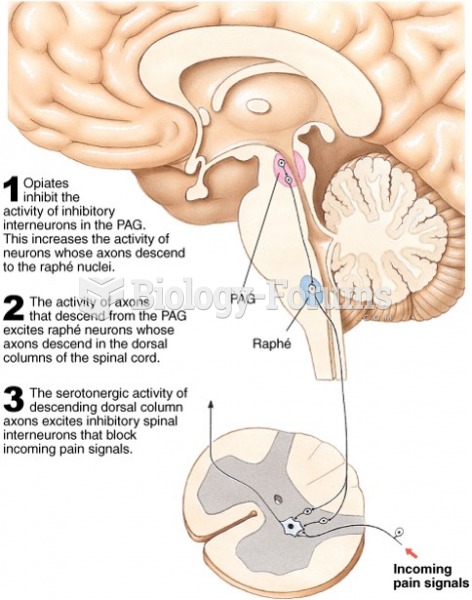

Basbaum and Fields’s (1978) model of the descending analgesia circuit.

Basbaum and Fields’s (1978) model of the descending analgesia circuit.

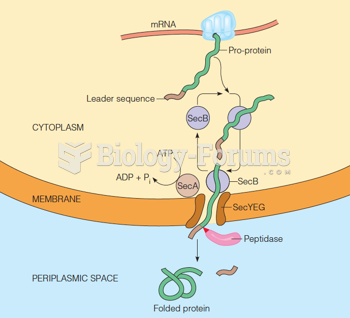

A current model for protein secretion by prokaryotes

A current model for protein secretion by prokaryotes

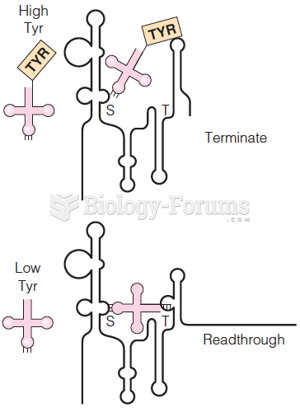

Model for induction of B. subtilis tyrS gene by uncharged tRNATyr

Model for induction of B. subtilis tyrS gene by uncharged tRNATyr

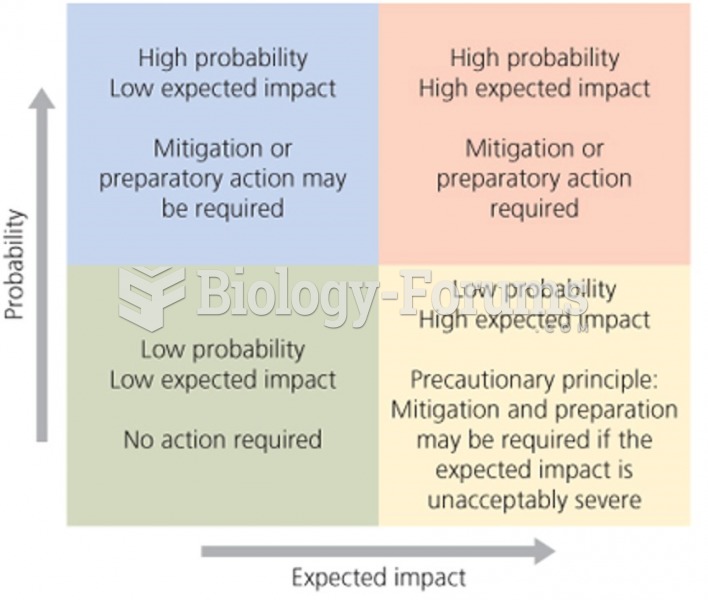

Risk assessment analyzes

Risk assessment analyzes

The ABC model of flower development

The ABC model of flower development