This topic contains a solution. Click here to go to the answer

|

|

|

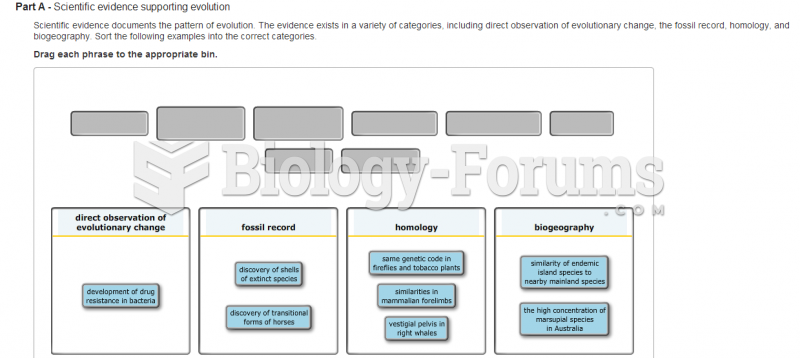

master biology chapter 22-25

master biology chapter 22-25

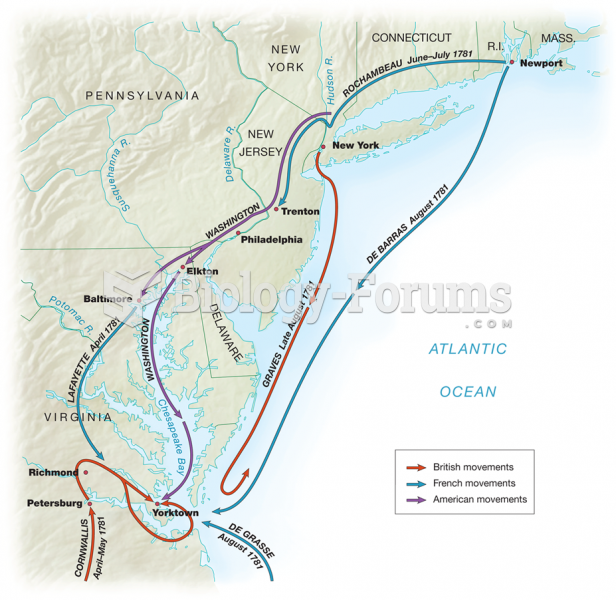

The Yorktown Campaign, April to September 1781

The Yorktown Campaign, April to September 1781

Christian Gladu, The Bungalow Company, The Birch, North Town Woods, Bainbridge

Christian Gladu, The Bungalow Company, The Birch, North Town Woods, Bainbridge

Water (Its Volume Expansion Upon Freezing)

Water (Its Volume Expansion Upon Freezing)

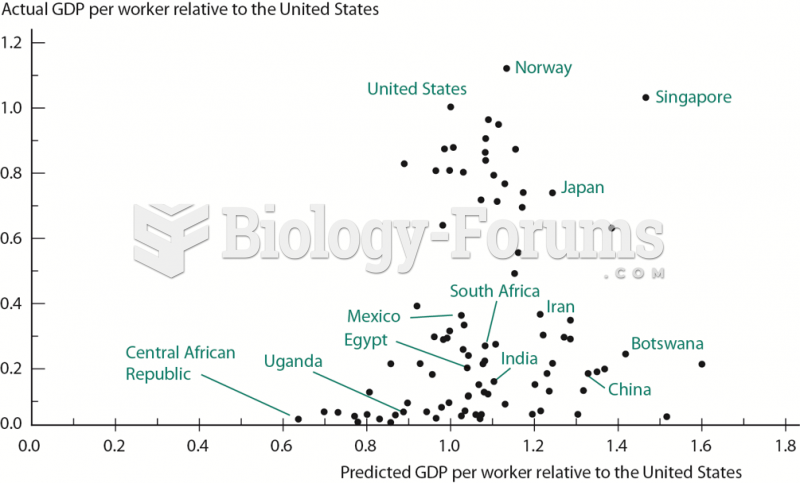

Predicted versus Actual GDP per Worker

Predicted versus Actual GDP per Worker

Paramedic Care: Principles & Practice, Volume 1, 5th Edition

Paramedic Care: Principles & Practice, Volume 1, 5th Edition