This topic contains a solution. Click here to go to the answer

|

|

|

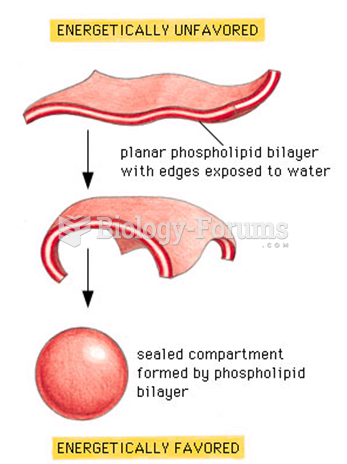

Self-sealing property

Self-sealing property

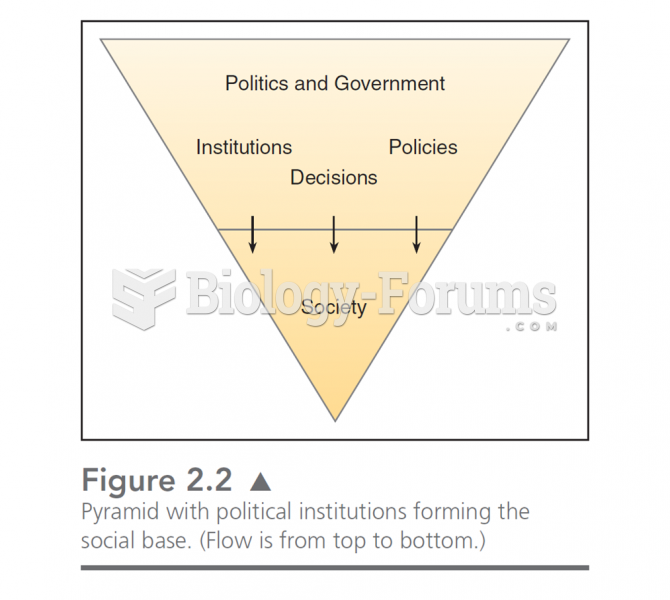

This chart illustrates the “drip down” model of government. In this, politics is formed by the soc

This chart illustrates the “drip down” model of government. In this, politics is formed by the soc

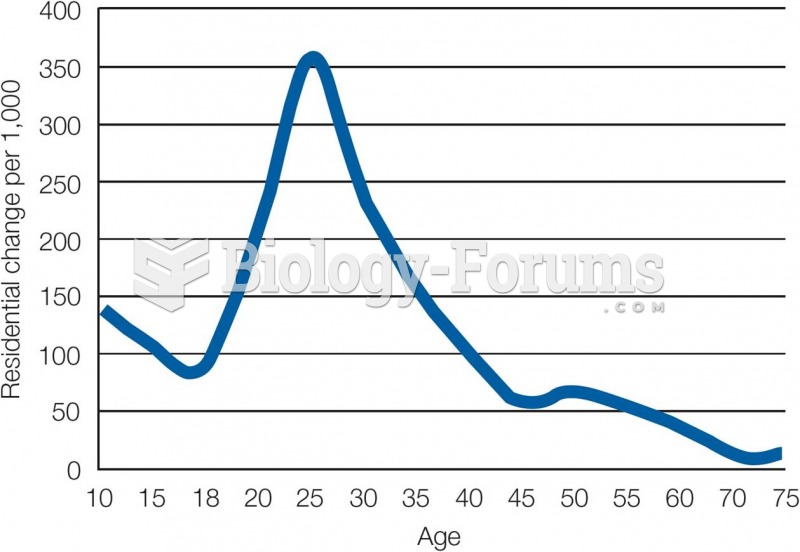

Rate of Residential Change, Past Year, in the United States

Rate of Residential Change, Past Year, in the United States

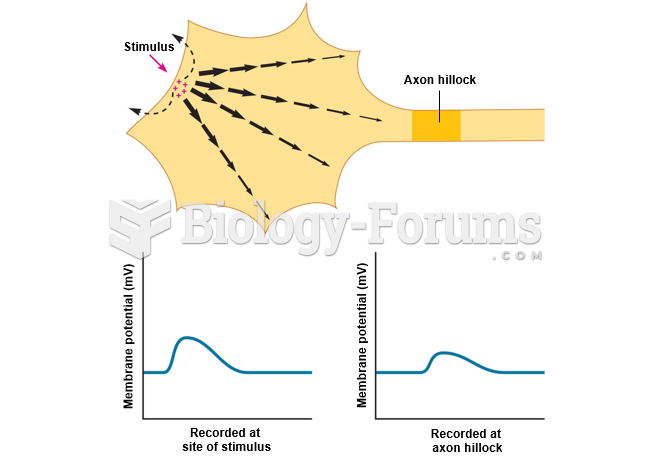

Decremental property of graded potentials.

Decremental property of graded potentials.

Prestige can sometimes be converted into property. Shown here is “Snooki” Polizzi, a reality ...

Prestige can sometimes be converted into property. Shown here is “Snooki” Polizzi, a reality ...

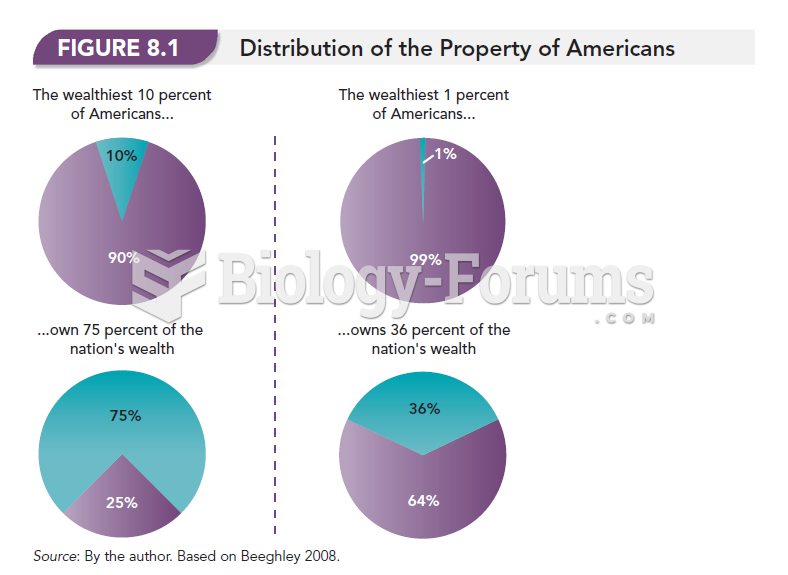

Distribution of the Property of Americans

Distribution of the Property of Americans