This topic contains a solution. Click here to go to the answer

|

|

|

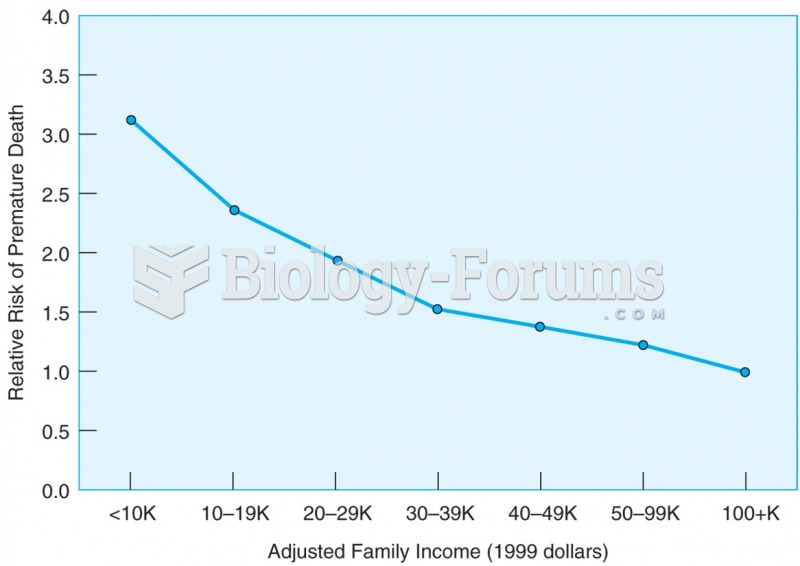

The risk of dying before the age of 65 gets lower as family income gets higher.

The risk of dying before the age of 65 gets lower as family income gets higher.

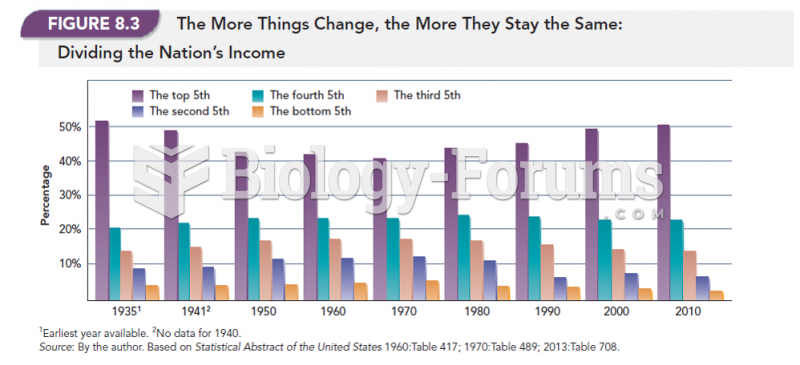

The More Things Change, The More They Say the Same: Dividing the Nation's Income

The More Things Change, The More They Say the Same: Dividing the Nation's Income

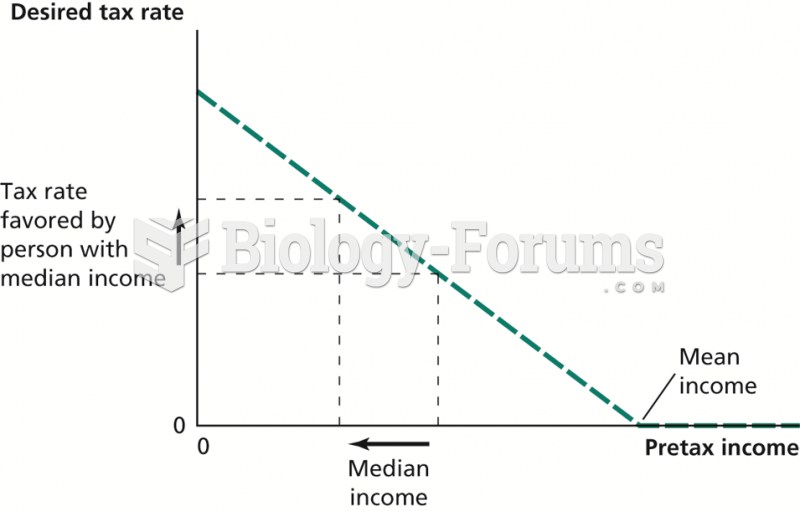

How an Increase in Income Inequality Affects the Desired Tax Rate

How an Increase in Income Inequality Affects the Desired Tax Rate

Income per Capita versus Total Fertility Rate

Income per Capita versus Total Fertility Rate

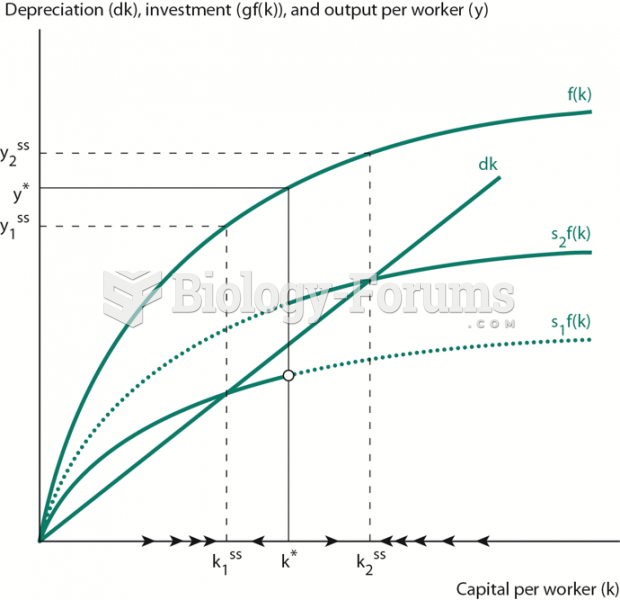

Solow Model with Saving Dependent on Income Level

Solow Model with Saving Dependent on Income Level

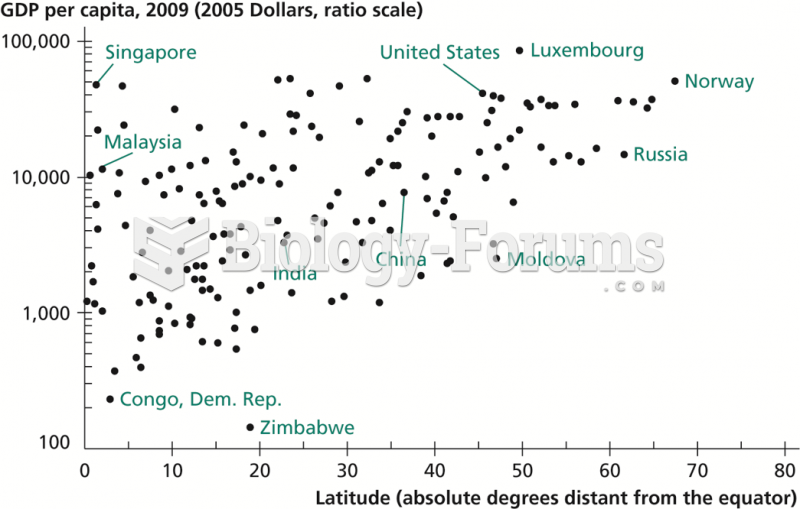

Relationship between Latitude and Income per Capita

Relationship between Latitude and Income per Capita